You’re staring at a chart, price is jumping around, and every candle feels important until the next one wipes out the story. That’s where volume weighted average price, or VWAP, earns its place. It helps you stop reacting to every move and start judging price against where most trading happened.

For active traders, VWAP isn’t just another line. It’s a practical reference for fair value, intraday bias, and risk control. If you trade stocks, indices, forex, crypto, or CFDs, understanding how VWAP works can clean up your decision-making fast.

Introduction

Most newer traders read price but ignore participation. That’s a problem. A move on light activity and a move on heavy activity don’t mean the same thing, even if the chart shape looks identical.

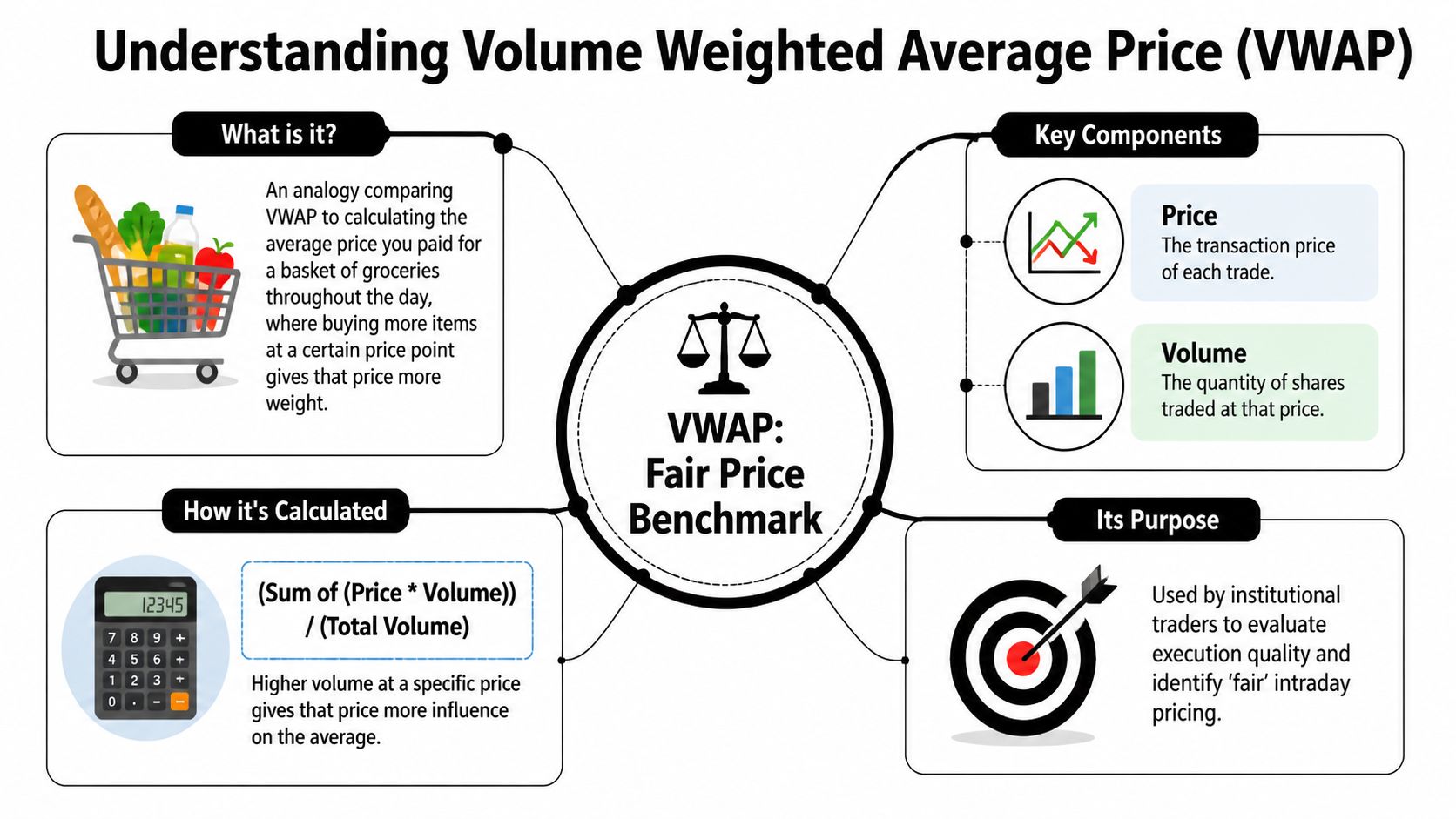

Volume weighted average price fixes that by combining price with volume. In simple terms, it asks: at what price did the market do most of its business during this session? That makes it useful for spotting fair value, checking whether buyers or sellers have control, and deciding whether a move is extended or still healthy.

Consider buying apples throughout the day. If you buy a few at one price and a lot more at another, your real average cost isn’t a plain average of the two prices. The bigger purchase matters more. VWAP works the same way. It gives more weight to prices where more trading happened.

Practical rule: If you only look at price, you’re missing context. VWAP adds that context.

Trading still involves risk of loss, and no indicator guarantees anything. But if you want a cleaner way to judge intraday structure, VWAP is one of the best tools to learn.

What Is the Volume Weighted Average Price

A trader looking at the same market on TradingView, cTrader, and DXtrade can see three charts that look almost identical, yet the VWAP line may sit in slightly different places. The reason is simple. VWAP depends on volume, and volume data is not always identical across platforms, especially in CFDs and prop firm simulation environments.

That nuance matters because volume weighted average price is not just another line on a chart. It is the average price traded during the session, with heavier trading activity given more influence than lighter activity. In market structure terms, VWAP asks a practical question: where did most business get done today?

Institutional desks have long used VWAP as an execution benchmark, and the standard definition is summarized in Wikipedia’s overview of VWAP. Retail traders can use the same tool for a different job. It helps frame whether current price is trading near the session’s accepted value or stretching away from it.

The basic idea

A plain average gives every price equal importance. VWAP does not.

If price trades briefly at one level but a large amount of volume goes through at another, VWAP shifts toward the level where more orders were filled. That makes it a more useful intraday reference point than a standard average built only from price. If you already use trend tools, it helps to compare VWAP with a traditional moving average indicator. A moving average smooths price over time. VWAP adds participation.

A grocery receipt is a good comparison. If you buy one item at a high price and ten items at a lower price, your real average cost is shaped more by the larger purchase. VWAP works the same way.

How the formula works

The formula is straightforward:

VWAP = cumulative total of (price × volume) / cumulative total volume

You do not need to calculate it by hand before the open, but you should understand what each part means:

- Price: the trade price, or on many charting platforms a bar-based typical price

- Volume: the amount traded at that price

- Cumulative total: the running sum from the session open

VWAP usually resets at the start of each trading day and updates throughout the session. That reset is why traders mainly use standard VWAP as an intraday tool rather than a swing-trading indicator.

One caution for funded traders. On centralized markets, such as many futures products, volume is closer to the true traded volume. On many CFD platforms, the platform may show tick volume or broker-specific feed data instead. In a prop firm challenge on cTrader or DXtrade, VWAP can still be useful, but you should treat it as a platform-specific reference, not a universal market truth.

Why traders care

VWAP helps answer three practical questions during the day:

- Where is fair value for this session? VWAP gives a running reference for the price area where activity has concentrated.

- Is price trading with acceptance or extension? A market holding near VWAP often behaves differently from one that is accelerating far above or below it.

- Am I chasing? If you enter too far from VWAP without a clear reason, your risk usually gets worse because your stop often has to be wider.

That last point is where many newer traders slip up. They see momentum, enter late, and only afterward notice they bought far above the session’s average traded price. VWAP helps catch that mistake before the order is placed.

VWAP is best used as a decision aid. It improves context, helps frame entries, and can keep risk tighter. It does not predict the next move, and in simulated prop environments it is only as reliable as the volume feed behind it.

How to Interpret VWAP for Intraday Trading

Most traders use VWAP poorly at first. They see price touch the line and expect an automatic reversal. That’s not how it works. VWAP is better used as context first, signal second.

Above VWAP and below VWAP

Start with the simplest read.

When price spends time above VWAP, the market is trading above its volume-adjusted fair value for the session. That often supports a bullish intraday bias. When price stays below VWAP, it suggests weaker auction conditions and seller control.

That doesn’t mean you buy every break above VWAP or short every break below it. You still need to judge the quality of the move:

- Strong hold above VWAP: pullbacks may attract buyers

- Repeated failure at VWAP from below: short setups can make more sense

- Choppy back-and-forth around VWAP: there may be no clean edge at all

If you already use moving averages, it helps to compare the two. A moving average smooths price. VWAP tracks where trading activity has concentrated. This is why many traders use both. If you want a refresher on how moving averages differ in practice, this guide to the moving average indicator is a useful comparison point.

VWAP as a center of gravity

VWAP often acts like a center of gravity for intraday price.

In a balanced session, price may rotate above and below it. In a directional session, price may trend away from it for a while, then use it as a pullback area. In a messy session, it may be flat and not worth much.

Watch the reaction, not just the touch.

A few useful questions:

- Is price rejecting VWAP quickly, or drifting through it?

- Is VWAP sloping, or nearly flat?

- Did the move into VWAP come with momentum, or did it slow down first?

Those details matter more than the line itself.

A clean reaction at VWAP usually tells you more than a random cross through it.

Mean reversion and extension

VWAP is also useful for identifying extension. If price runs hard away from VWAP, some traders look for a move back toward it. This works best when the market is not in a strong trend.

A simple way to think about it:

| Market condition | Common VWAP use |

|---|---|

| Trend day | Look for pullbacks toward VWAP in the trend direction |

| Range day | Look for moves back toward VWAP after extension |

| Choppy open | Wait and let VWAP develop before trusting it |

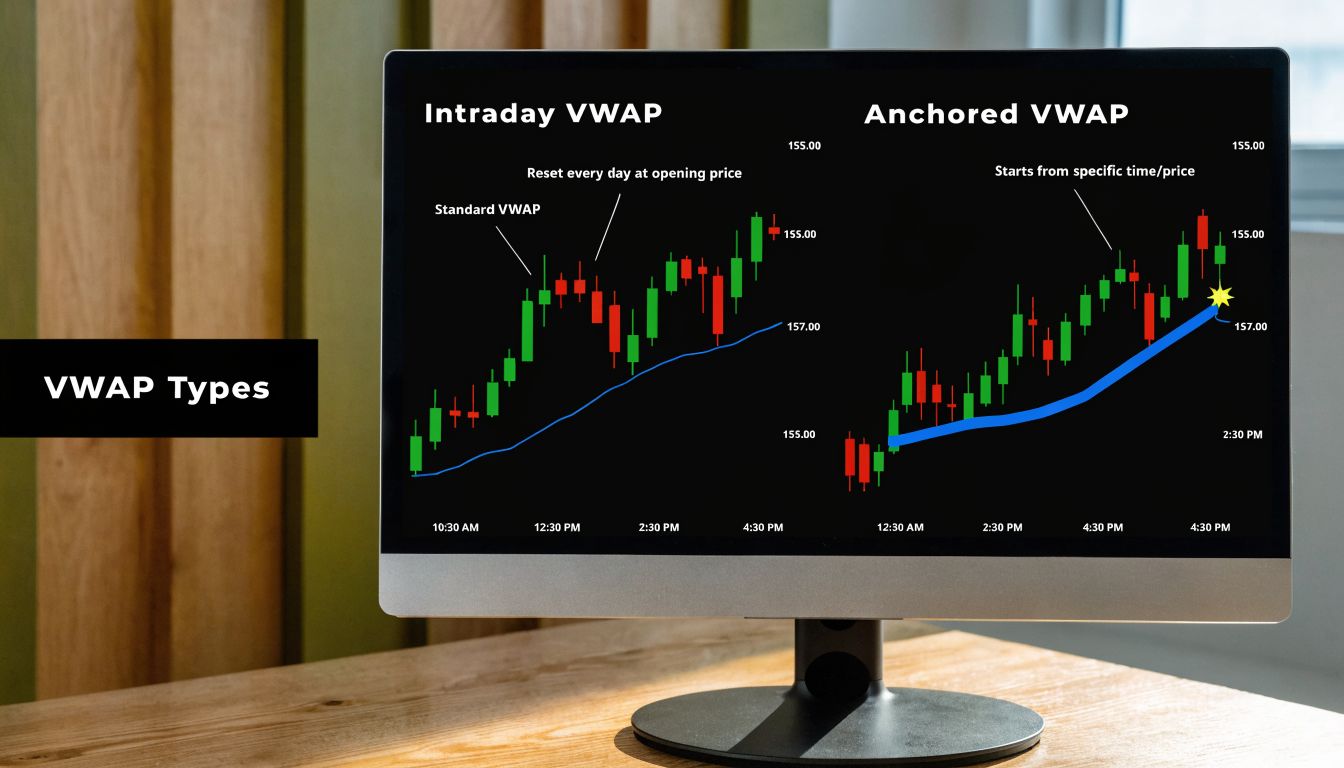

Intraday VWAP and anchored VWAP

There are two related tools traders often mix up.

Intraday VWAP resets each session and is best for session-based decisions.

Anchored VWAP starts from a specific point on the chart, such as a breakout, major low, or news event.

The practical difference is simple:

- Use intraday VWAP when you want today’s fair-value reference

- Use anchored VWAP when you want fair value measured from a meaningful event

Both are useful. They just answer different questions.

Intraday VWAP vs Anchored VWAP

One line starts fresh every day. The other starts where you choose. That’s the core difference.

When intraday VWAP makes more sense

A trader opens the chart after the cash session begins. They want to know whether buyers are controlling today’s trade, where fair value sits right now, and whether a pullback is healthy or dangerous.

That’s an intraday VWAP job.

Use it when you care about:

- today’s opening auction

- session bias

- intraday pullbacks

- mean reversion inside the day

Because it resets daily, it stays focused on the current session. That makes it clean and practical for day traders.

When anchored VWAP is the better tool

Another trader doesn’t care where today started. They care where price has traded relative to a major event. Maybe a breakout launched yesterday. Maybe a key swing low formed earlier in the week. Maybe a news spike changed structure.

That’s where anchored VWAP helps.

You choose the starting point. The line then measures volume-weighted fair value from that event forward.

Three workable setups

Here are three setups that show how the two versions differ in practice.

Session pullback with intraday VWAP

Price opens strong, pushes above VWAP, then pulls back calmly. The trader waits for the pullback to test VWAP without heavy selling pressure.

- Entry idea: after price rejects VWAP and the next candle confirms higher

- Stop logic: below the pullback low, not directly on the line

- Exit idea: previous intraday high or scale out into strength

This works best when VWAP is rising and price has already shown trend behavior.

Breakdown retest with intraday VWAP

Price spends the early session below VWAP and fails every attempt to reclaim it. A bounce reaches the line again, but buyers can’t hold above it.

- Entry idea: short after rejection from VWAP

- Stop logic: above the rejection high

- Exit idea: prior session low or a fresh impulse leg lower

The key is failure, not just contact.

Event-driven trade with anchored VWAP

A strong breakout candle clears resistance. Instead of using session VWAP, the trader anchors VWAP from the breakout bar to see whether price is holding above post-breakout fair value.

- Entry idea: buy a retest that stays above anchored VWAP

- Stop logic: below the retest structure

- Exit idea: trail as long as price respects the anchored line

If the setup is tied to an event, anchored VWAP usually gives cleaner context than the daily reset line.

Practical VWAP Trading Strategies

VWAP is most useful when you turn it into repeatable rules. Not rigid predictions. Rules. You want clear conditions for entry, invalidation, and management.

VWAP rejection trade

This is one of the simplest setups.

Price approaches VWAP after trading on one side of it for a while. Instead of crossing and holding, it rejects sharply. That rejection tells you the market still sees VWAP as a decision level.

A practical checklist:

- Find one-sided context. Price has spent meaningful time above or below VWAP.

- Wait for the retest. Don’t chase the first impulse.

- Read the reaction. Rejection candles, failed closes through VWAP, or clear loss of momentum matter.

- Define the invalidation. Place the stop where the rejection idea is clearly wrong.

- Manage toward structure. Prior highs, lows, or range edges usually make more sense than arbitrary targets.

This setup is best when the market is already showing directional intent.

VWAP pullback in trend

This is different from a pure rejection. Here, you’re trading with the session trend after a healthy retracement.

Common signs:

- VWAP slopes up and price forms higher lows

- Price pulls back toward VWAP instead of collapsing through it

- Buyers step in before or at the line

For short setups, reverse the logic.

If you want to combine VWAP with price structure, this guide to intraday trading chart patterns pairs well with pullback entries because chart patterns often give the confirmation VWAP alone cannot.

VWAP mean reversion

This setup works better in balanced or range-bound conditions than in strong trend days.

You’re looking for price that has moved too far from VWAP and may snap back toward fair value. The mistake traders make is trying to fade every extension. Some extensions are the start of a trend, not the end of one.

A safer approach:

- Look for a stretched move away from VWAP

- Wait for momentum to stall

- Enter only after price shows failure to continue

- Treat VWAP as the reversion target, not a guarantee

VWAP bands and extremes

Some platforms add standard deviation bands around VWAP. These bands can help you spot stretched conditions, but they are not automatic reversal zones.

Use them as an extra layer:

| Situation | Better read |

|---|---|

| Price tags upper band in trend | Could be strength, not a short |

| Price tags upper band in range | Reversion may be more likely |

| Price tags lower band after panic move | Watch for stabilization first |

Simple VWAP logic for automation

If you trade through cBots, EAs, or alert scripts, keep the logic basic before you add filters.

Pseudo-code example:

- If price closes above VWAP after being below it

- And the next candle does not break back below immediately

- Then trigger a long alert

- Invalidate if price closes back under VWAP

That kind of rule is easy to test. It’s also easy to improve with filters like session time, structure, or volatility. The point isn’t to automate complexity. The point is to automate consistency.

VWAP for Funded Traders Pitfalls and Risk Rules

You take a clean VWAP bounce on a prop account. The setup looks disciplined on cTrader or DXtrade. Price reacts for a moment, then tags your stop and keeps going. The frustrating part is that your read of price action may not have been the actual problem. The VWAP line itself may have been built on volume data that does not match the broader market well enough to trust on its own.

That gap matters more in funded trading than many retail traders realize.

VWAP is only as good as the volume feeding it. In a centralized futures market, that relationship is clearer. In CFDs, some crypto products, and simulated environments, the platform may rely on tick volume, broker-side flow, or synthetic pricing. The line can still look neat and precise, but neat is not the same as reliable.

For a self-funded trader, a slightly off reference point is annoying. For a funded trader, it can push an otherwise reasonable trade into a daily loss limit or max drawdown violation.

Where funded traders get trapped

The trap is simple. Traders assume VWAP on the screen reflects the same participation that institutional desks are watching. Sometimes it does not.

That mismatch shows up most often in thinner instruments, off-peak sessions, and products where volume is fragmented across venues. A VWAP pullback that looks attractive on a demo or challenge account may be less meaningful if the underlying volume picture is incomplete. This is one reason traders who perform well on chart replays or personal accounts can struggle to repeat the same execution inside a prop evaluation.

Platforms like cTrader and DXtrade are useful tools, but the indicator output still depends on the data stream behind the platform. If you trade funded accounts, treat platform VWAP as a reference that needs confirmation, not as proof of fair value.

Why this problem is sharper in simulated prop environments

A funded account has less room for technical sloppiness.

Most firms set hard limits such as a daily loss cap and an overall drawdown cap. That changes how you should use any indicator built from volume. If your VWAP is even slightly out of sync with the market you think you are trading, three things happen fast. Your entry is late or early. Your stop is placed in the wrong spot. Your position size, based on that faulty location, now carries more risk than planned.

It works like using a ruler with the wrong markings. The measurement error may look small, but every decision built on it gets worse.

A safer way to use VWAP on prop platforms

Start with market structure, then ask whether VWAP supports the idea.

That order matters. If price is reclaiming a key intraday level, holding above a prior swing, and showing responsive buying, VWAP can strengthen the case. If the only reason for the trade is “price touched VWAP,” you are leaning on the most fragile part of the setup.

A practical framework:

- Favor liquid instruments and active sessions, where the volume input is usually more representative

- Compare VWAP with obvious structure such as prior highs, lows, opens, and session ranges

- Watch how price behaves at VWAP. Acceptance, rejection, or failure matters more than the touch itself

- Be more cautious with crypto CFDs, thin indices, and quiet session trading

- Define the invalidation point before entry, based on price structure first and VWAP second

If you want examples of how traders turn that logic into rules, this guide to a VWAP trading strategy is a useful companion.

Risk rules that keep VWAP from becoming an excuse

Funded traders often misuse VWAP in one of two ways. They either treat it like a magic support and resistance line, or they keep taking every cross because the indicator makes the trade feel objective.

A better rule is stricter. VWAP can help you filter trades, time entries, or judge whether price is extended. It should not override your risk limits, your session plan, or obvious market context.

Use checks like these before any VWAP-based trade:

- Is this market active enough for volume-based tools to carry weight?

- Does price structure support the same direction as VWAP?

- If VWAP is misleading here, where does the trade clearly fail?

- Will the full loss on this trade still leave room under the day’s limit?

- Am I using VWAP for context, or to justify a trade I already want to take?

That last question matters because challenge accounts are often lost through forced trades, not through a lack of indicators.

Trading involves risk of loss. In a funded evaluation, good VWAP use is less about finding more trades and more about avoiding weak ones.

VWAP Frequently Asked Questions

Is volume weighted average price better than a moving average

Not better. Different.

A moving average tracks price over a chosen lookback period. Volume weighted average price tracks price with volume built in and usually resets each session. If you want intraday fair value, VWAP often gives cleaner context. If you want broader trend analysis across multiple sessions, moving averages are usually more practical.

Can you use VWAP for swing trading

Classic session VWAP is mainly an intraday tool because it resets. For swing trading, many traders use anchored VWAP instead. By anchoring the calculation to a key low, high, breakout, or news event, you can study whether price is holding above or below volume-weighted value from that point forward.

Is VWAP a leading or lagging indicator

It’s generally lagging because it’s calculated from completed trading activity. It doesn’t forecast the future. It summarizes where trading has occurred so far.

That said, traders still use it proactively. Not because it predicts direction, but because other market participants watch it and react around it.

Why does price sometimes ignore VWAP

Because VWAP is a reference, not a law.

Strong trends can stay far above or below VWAP for long stretches. News-driven markets can slice through it. Low-quality volume data can also make the line less meaningful. If price seems to ignore VWAP repeatedly, the problem may be market conditions, instrument quality, or your expectation of what VWAP is supposed to do.

Conclusion

Volume weighted average price helps you judge intraday price with more context than price alone. It gives you a fair-value reference, helps frame bullish or bearish control, and can improve trade selection when you combine it with structure and risk rules.

Used well, VWAP can make your trading cleaner and more disciplined. Used blindly, especially in thin or simulated markets, it can create false confidence. Keep expectations realistic, respect your risk, and remember that trading involves risk of loss. This article is educational only and not financial advice.

If you’re ready to apply disciplined intraday trading in a prop environment, explore MyFundedCapital to compare funding programs, review account types, and choose a challenge that fits your trading style.