You see a swap charge on your platform, a wider spread after a central bank meeting, or a change in overnight holding cost, and it feels like back-office noise. It isn't. Interest rate benchmarks are part of the pricing plumbing behind margin trading, and they can subtly change your P&L even when your chart analysis is solid.

If you trade forex, indices, or CFDs on a prop or retail account, you need to know what these benchmarks are, why they changed, and how they feed into funding costs, carry, and execution risk. This is the practical version.

What Exactly Is an Interest Rate Benchmark

An interest rate benchmark is the reference rate financial firms use as a base for pricing money. The cleanest way to think about it is this: it's the wholesale price of money for the banking and financial system.

Retail traders usually don't borrow directly at that wholesale rate. Brokers, banks, liquidity providers, and other firms do. Then they add their own spread, fee structure, and risk buffer on top. By the time it reaches your account, it often shows up as a swap, overnight financing charge, or a change in the pricing of products using borrowed funds.

Why traders should care

If you hold positions intraday only, benchmarks still matter because they affect liquidity conditions and rate expectations. If you hold overnight, they matter even more because they can directly alter your cost base.

A few practical examples:

- Forex positions: The overnight adjustment often reflects the rate differential between the two currencies, plus the broker's or venue's markup.

- Index CFDs: The cost of carry usually includes a financing component linked to benchmark rates.

- Margin trading conditions: If funding gets more expensive upstream, firms may tighten conditions, adjust charges, or change margin treatment.

Practical rule: If your strategy depends on holding trades for days, benchmark rates matter almost as much as your entry signal.

Where the hidden impact comes from

Most traders look at the front-end number on the platform and stop there. The core issue sits underneath. Changes in benchmark design and benchmark transitions can alter funding conditions for institutions first, then flow downstream to traders.

Research on benchmark transitions found that smaller financial institutions experienced “reduced equity returns, higher interest spreads, and loss of market share” according to the Virginia Tech benchmark reference rate paper. That matters because when smaller institutions face higher funding pressure, the end user often feels it through pricing, spreads, or less favorable credit terms.

Benchmarks are not just macro trivia

A lot of traders treat rates like something only economists watch. That's a mistake. When the Fed changes its stance, or when markets rapidly reprice future policy, funding costs don't stay in the macro section of a news terminal. They move into your trading statement.

If you want a quick example of how benchmark shifts become market-moving events, Fed boosts interest rate by 0.75% is a useful read because it shows how policy moves feed into broader financial conditions that traders actually trade through.

The Great Transition From LIBOR to SOFR

For years, traders heard about LIBOR without needing to understand it. That changed when the system behind it broke trust.

LIBOR was a benchmark built from bank submissions about borrowing costs. The core problem was obvious in hindsight. A benchmark that influences huge parts of the financial system is vulnerable if it relies too heavily on estimates instead of deep, observable transactions.

Why the old model had to go

After manipulation scandals, regulators and central banks pushed markets toward risk-free rates, often called RFRs. The big shift was methodological.

Old benchmark logic leaned more on panel submissions and judgment. New benchmark logic leans more on actual transactions.

That's the key lesson for a trader. The benchmark world moved from “what participants say the rate is” toward “what the market traded.”

A benchmark is only as useful as the market reality underneath it.

Why SOFR became central for USD markets

For US dollar markets, SOFR became the flagship replacement benchmark. You don't need to master all the institutional details to grasp the practical takeaway. If you trade USD-linked products, the benchmark framework underneath them is now built around a more transaction-grounded reference point.

That shift matters because benchmark credibility affects:

- Derivative pricing

- Funding calculations

- Curve construction

- Risk models

- How firms hedge rate exposure

When the benchmark is more reliable, pricing tends to rest on firmer ground. That doesn't remove volatility. It reduces one layer of structural uncertainty.

Central banks still set the tone

Even with better benchmark design, the benchmark environment still lives under central bank policy. In the early 1980s, the Federal Reserve under Paul Volcker pushed its key rate to around 20% to fight inflation, a move described in Bankrate's history of the federal funds rate. It triggered a recession, but it also showed how aggressively central banks can reset the cost of money that sits beneath global benchmarks.

For traders, the lesson is simple. Benchmark reform improved integrity, but it didn't remove policy risk. If a central bank sharply changes direction, the benchmark-linked costs and expectations across markets can still move fast.

What works and what doesn't

What works:

- Watching benchmark reform as market structure, not trivia

- Assuming funding costs can change even if your strategy rules don't

- Treating rate-sensitive products differently from pure intraday setups

What doesn't:

- Ignoring swap and carry because the chart “looks good”

- Assuming all overnight fees are arbitrary broker choices

- Using long holding periods without understanding the financing side

A Trader's Guide to Major Global Benchmarks

You don't need to memorize every benchmark in the world. You do need to know which benchmark sits behind the currency or product you trade most often.

Here's the short version. If you trade major FX pairs and CFDs, four benchmarks come up repeatedly in trader education and institutional pricing discussions: SOFR for USD, SONIA for GBP, €STR for EUR, and TONAR for JPY.

Major Global Interest Rate Benchmarks at a Glance

| Benchmark | Currency | What It Measures | Administered By |

|---|---|---|---|

| SOFR | USD | A key overnight reference used in US dollar markets | Federal Reserve Bank of New York |

| SONIA | GBP | A key overnight reference used in sterling markets | Bank of England |

| €STR | EUR | Euro area banks' wholesale unsecured overnight borrowing costs | European Central Bank |

| TONAR | JPY | A key overnight reference used in yen markets | Bank of Japan |

What matters most for traders

The trader's question isn't “Which benchmark is academically interesting?” It's “Which one affects the products I hold and the currency I'm exposed to?”

Use this quick mapping:

- EURUSD: You're dealing with the interaction of euro and dollar rate expectations.

- GBPUSD: Sterling and dollar benchmark expectations both matter.

- USDJPY: This pair is highly sensitive to differences in rate regimes and central bank paths.

- European index or euro-linked CFDs: The euro benchmark environment matters for financing and pricing.

Why €STR deserves special attention

The euro short-term rate, €STR, is a good example of what modern benchmark construction looks like. The ECB says €STR is calculated as the trimmed, volume-weighted mean of actual daily transactions, and from 2023 to 2025 it moved from -0.5% to 3.5%, influencing pricing across over €300 trillion in derivatives according to the ECB explainer on benchmark rates and €STR.

That sounds institutional, but the practical read-through is straightforward. A benchmark can sit in the background while still anchoring a huge amount of pricing across swaps, futures, and related products. Traders don't need direct exposure to that full institutional ecosystem to feel the downstream effects.

Desk view: If you trade a major currency, assume its benchmark environment affects both your direct cost of holding and the behavior of larger participants around you.

How to use this as a trader

Keep it simple:

- Identify your base exposure. If you mostly trade USD crosses, start with the USD benchmark environment.

- Check the second currency. A pair is a spread between two policy paths, not just one.

- Match benchmark awareness to holding period. The longer you hold, the more benchmark effects matter.

- Watch benchmark-sensitive events. Central bank meetings, inflation releases, and policy guidance often shift expectations before the published benchmark level itself changes.

You don't need to become a rates specialist. You need enough benchmark literacy to stop treating financing costs as random noise.

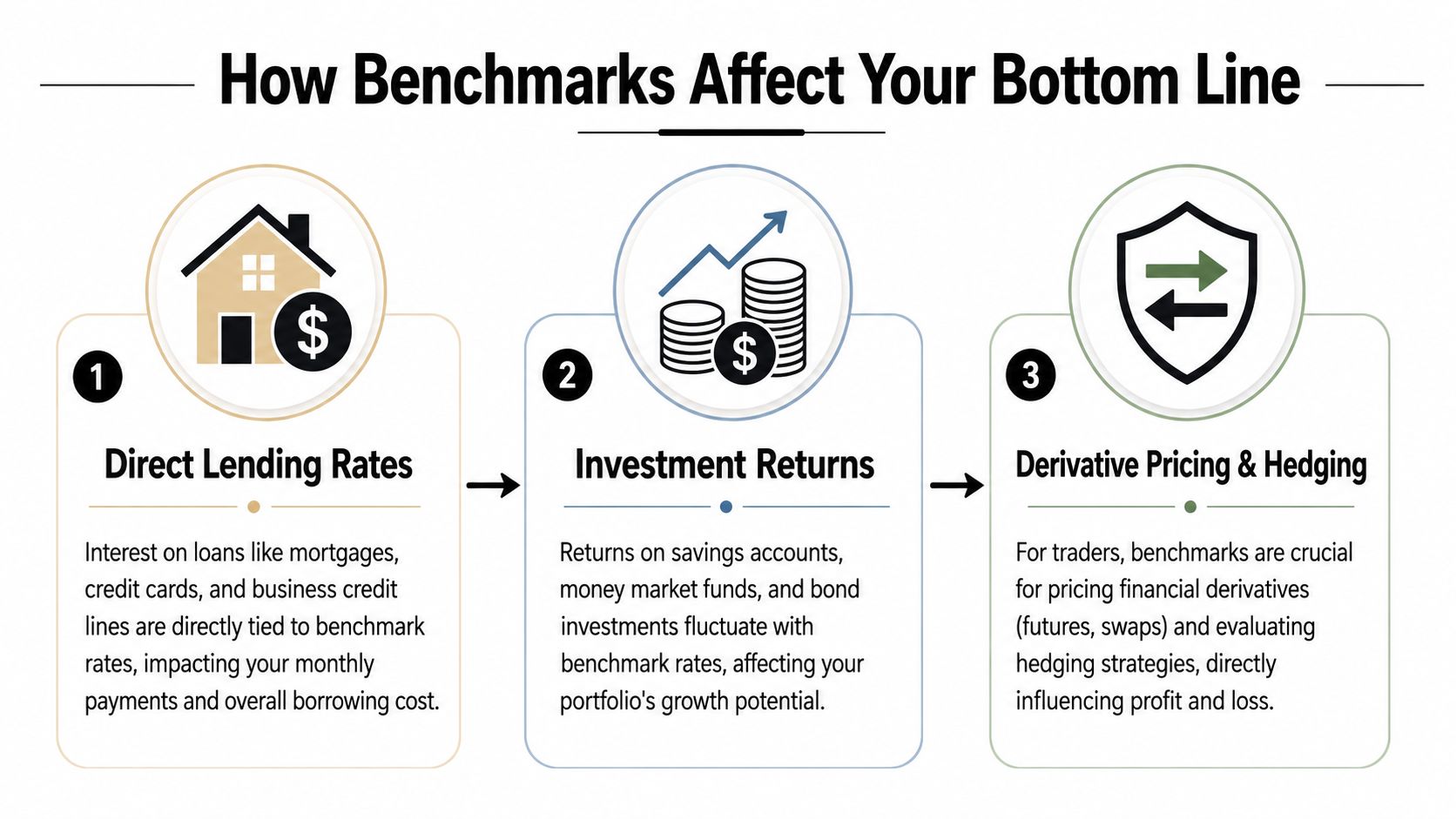

How Benchmarks Hit Your Bottom Line

Interest rate benchmarks stop being theory here and start showing up as money in or money out.

Three channels matter most for a trader: overnight funding, cost of carry in derivative pricing, and the cost of debt built into the ecosystem around your account.

Overnight swaps and financing

If you hold a CFD or forex position overnight, your platform usually applies a financing adjustment. The exact method varies by provider, but the general logic is often close to:

- Relevant benchmark rate

- Plus or minus the currency differential or product financing component

- Plus the provider's spread or markup

A simple mental model is:

Overnight cost ≈ benchmark-based funding rate + provider adjustment

That won't match every contract specification line by line, but it's close enough to make better trading decisions. If benchmark expectations rise, overnight holding costs often become less forgiving for strategies that sit in positions too long.

Cost of carry in CFD pricing

Benchmarks also feed into the pricing logic of derivatives and cash-settled products. On an index CFD, for example, the level you see isn't only about the chart pattern or the cash market. Financing assumptions often sit underneath the structure.

That's why some traders struggle with decent directional calls but still underperform in practice. They focus on setup quality and ignore the carry layer.

If you run a business or want a better feel for how funding assumptions change planning decisions, tools used to compare business cash flow software can sharpen your thinking. Different context, same discipline. Costs that look small in isolation can materially change outcomes when they recur.

Leverage is never free

Many newer traders think borrowing power is a platform feature. It isn't. It has an economic cost somewhere in the chain.

Firms providing access to products involving borrowed capital still operate inside a broader funding environment. When benchmark-linked costs rise, firms may respond by changing overnight charges, tightening risk conditions, or adjusting how certain products are offered.

For traders, the practical checklist looks like this:

- Check the contract specs: Look for swap, financing, and triple-swap details before holding trades.

- Test strategy sensitivity: A swing strategy can look strong in backtests and weaken badly once realistic financing is applied.

- Watch margin usage: If your sizing is loose, financing drag and volatility can work together.

- Know the math: A margin primer like this forex margin calculation guide helps connect exposure, use of borrowed funds, and account pressure.

Don't judge a strategy only by win rate. Judge it by net outcome after financing, spread, and execution.

What usually works better

Traders handle benchmark-linked costs better when they:

- Separate intraday and swing models

- Track overnight charges in the journal

- Avoid holding low-conviction trades “just in case”

- Review whether positive carry is a feature or just a side effect

What usually works worse:

- Holding every trade overnight by default

- Ignoring swap because it seems small

- Backtesting without a realistic financing assumption

- Treating borrowed capital as costless

Trading Strategies and Risks in a Volatile Rate Environment

A volatile rate environment doesn't just increase costs. It changes which strategies make sense.

The obvious example is the carry trade. In simple terms, traders seek exposure that benefits from borrowing in a lower-rate currency and holding a higher-rate one. In calm periods, that can support a position over time. In unstable periods, the same trade can unwind violently if policy expectations shift or risk appetite breaks.

Where the opportunity sits

Benchmark differentials can shape currency behavior in ways technical traders can use. If one central bank is moving toward tighter policy while another is staying easier, that relative path can affect trend quality, momentum, and overnight carry.

This shows up in practice through:

- Swing bias in major FX pairs

- Repricing after central bank statements

- Shifts in forward-looking expectations before actual rate changes

- Changes in overnight hold attractiveness

A rates-aware trader doesn't need to predict every meeting perfectly. It's often enough to know when your setup is fighting the benchmark story.

Where the risk gets worse

Post-pandemic conditions brought heightened interest rate volatility, and that volatility boosted FX trading volumes in 2025, while also increasing risks such as slippage and unpredictable funding costs, as noted by the Kansas City Fed's review of post-pandemic interest rate dynamics.

That matters because volatility in rate expectations can break assumptions traders rely on:

- A spread that looked stable can widen.

- A funding estimate can become unreliable.

- Correlations between instruments can weaken.

- A carry trade can stop acting like a carry trade and start acting like a risk-off liquidation.

Risk management that actually helps

In this environment, broad “be careful” advice isn't enough. Do specific things.

- Reduce size before central bank events: If your edge depends on clean fills, don't hold full size into a rates catalyst.

- Separate carry from conviction: Don't keep a weak trade open just because the overnight rate differential looks favorable.

- Use hedge logic carefully: A hedge can reduce one risk while adding another. Traders who use multi-position structures should understand how hedging works in forex before trying to neutralize event risk.

- Recheck holding assumptions weekly: Funding conditions can change faster than many strategy docs do.

Rate volatility creates opportunity for prepared traders and avoidable damage for casual ones.

Where to Monitor Interest Rate Data

Most traders don't need an institutional data stack. They need a reliable routine.

The practical monitoring stack

Start with the official benchmark administrators. They are the primary source for benchmark definitions, methodology, and daily publication details. For the rates discussed earlier, that means the Federal Reserve system for US dollar benchmark data, the Bank of England for sterling, the ECB for euro benchmarks, and the Bank of Japan for yen references.

Then layer on tools you will use during the trading week:

- Economic calendars: Central bank meetings and inflation releases matter more to most traders than raw benchmark tables.

- Charting platforms: Use them to compare FX pairs, index moves, and rate-sensitive reactions.

- Platform contract specs: Your actual swap and financing treatment lives there, not in macro commentary.

- Futures conventions: If you follow rate-sensitive contracts, references like CME month codes help decode contract notation quickly.

What to check each week

A simple benchmark routine works better than information overload:

- Policy calendar: Know when the Fed, ECB, BoE, or BoJ is due.

- Market reaction: Watch how your instruments trade around those events.

- Holding cost review: Recheck financing on products you plan to hold.

- Journal note: Record whether benchmark conditions helped or hurt the trade.

You're not trying to become a macro economist. You're trying to stop getting blindsided by costs and volatility that were visible in advance.

Frequently Asked Questions

Do interest rate benchmarks matter if I only trade intraday

Yes, but less directly. You may avoid overnight financing, yet benchmark expectations still affect volatility, spreads, and how currencies react to news. Intraday traders often feel benchmarks through event risk and execution quality rather than swap charges.

Why does one platform's overnight charge look different from another

Because the benchmark is only the base layer. Each provider can apply different markups, contract terms, and product-specific financing rules. That's why two traders can look at the same market and still face different effective holding costs.

Are interest rate benchmarks only relevant for forex traders

No. They also matter in index CFDs, some commodity products, and any instrument that uses borrowed capital with a financing component. If a product has a cost of carry, benchmark rates are usually part of the story somewhere in the background.

Can a good strategy fail because of financing costs

Absolutely. A strategy with modest edge and long average holding time can weaken fast once swaps, spread, and slippage are applied realistically. This is why educational backtests and live results often diverge when traders ignore the benchmark-linked cost layer.

If you want to trade with clearer rules around risk, scaling, and platform choice, explore MyFundedCapital. You can compare funding programs, review account types, and start a challenge that fits your style. Trading involves risk of loss, and this article is educational only, not financial advice.