You click buy on a crypto setup that looks clean on the chart. The order fills, but not where you expected. Your stop is now closer than planned, your risk is larger than planned, and the trade starts in a hole before price even moves.

That gap between the price you saw and the price you got is often a liquidity problem. If you want to understand what does liquidity mean in crypto, think less about textbook definitions and more about execution quality, slippage, and whether you can get in and out without damaging your own P&L.

Introduction

A funded trader can be right on direction and still lose money on execution.

You hit buy on a breakout, the order fills higher than expected, and your stop now sits closer than planned. Nothing changed on the chart. Your risk changed in the market. That is a liquidity problem, and in prop trading it is not academic. It affects entry quality, position size, and whether a normal loss stays inside your drawdown rules.

Liquidity is the market’s ability to absorb your order without forcing a meaningful price move. In practice, the question is simple: can you get in and out near the price you planned, with size that fits your account, on the venue you trade?

Crypto adds another layer of risk because liquidity is split across exchanges, pairs, and time windows. A setup that looks tradable on one screen can behave very differently once your order meets a thin book, a wide spread, or a fast-moving perp market. Newer traders often treat that as bad luck. It is usually a market quality issue that should have been checked before the order was sent.

Practical rule: If you can’t explain where your fill will likely happen before you send the order, you don’t understand the trade’s actual risk yet.

For prop traders, liquidity is part of risk control. Poor liquidity widens the gap between planned risk and realized risk. That gap shows up as slippage, partial fills, worse exits, and avoidable drawdown pressure. A good setup in a thin market can still be a bad trade.

What Is Crypto Liquidity and Why It Matters

Crypto liquidity is the market’s capacity to take your order at or near the quoted price, without a sharp move against you. For a prop trader, that definition is practical, not theoretical. If liquidity is poor, the trade you planned and the trade you carry are two different things.

The easiest way to judge liquidity is to look at execution, not just price.

A market is liquid when orders can be filled with limited friction. In practice, that usually shows up in three places:

- Bid-ask spread. The difference between the best available buy and sell price.

- Order book depth. The amount of resting size available close to the current market.

- Slippage. The gap between the price you expected and the price you receive.

Those three signals determine whether your edge survives contact with the market. Tight spreads lower your entry cost. Real depth gives you room to trade size. Low slippage keeps your actual loss close to the one you modeled before entry. If you need a quick refresher on spread cost, this guide to how spreads work in trading covers the part many newer traders underestimate.

Liquidity matters because P&L is built on fills. A setup can be correct on direction and still underperform if you enter late, scale poorly, or get forced out through a thin book. That problem gets worse on funded accounts where daily loss limits and trailing drawdown rules leave little room for execution mistakes.

Here is where traders usually feel it first:

- Entry quality. A bad fill means the trade starts with avoidable cost.

- Stop distance. If entry slips, your stop may be tighter than planned or your dollar risk may be larger than planned.

- Exit control. Thin markets make it harder to reduce risk fast when the trade is wrong.

- Position sizing. Size that looks safe on paper can become oversized once slippage is included.

A chart does not show all of that. The order book does.

Liquidity also affects strategy selection. Breakout trading, momentum entries, and short-term scalps need reliable execution to work as tested. In a thin market, the same strategy can lose its expectancy because the spread widens, the book pulls, and market orders sweep through nearby levels too easily.

Crypto adds another complication. Liquidity is fragmented across exchanges, trading pairs, and products. BTC perp liquidity on a major centralized venue behaves very differently from a small altcoin pair or a thin pool on a decentralized venue. Two markets can show a similar chart and offer very different execution risk.

| Market style | How liquidity works | What traders usually like | Common problem |

|---|---|---|---|

| CEX order book | Buyers and sellers post bids and offers | Faster fills and visible depth on major pairs | Liquidity can vary sharply by exchange and time of day |

| DeFi pool | Traders swap against a liquidity pool | Access to newer or niche assets | Price impact can rise fast when pool depth is limited |

For prop traders, liquidity is part of pre-trade risk control. It decides whether a position can be entered, managed, and exited inside the firm’s rules, not just whether the idea looks good on the chart.

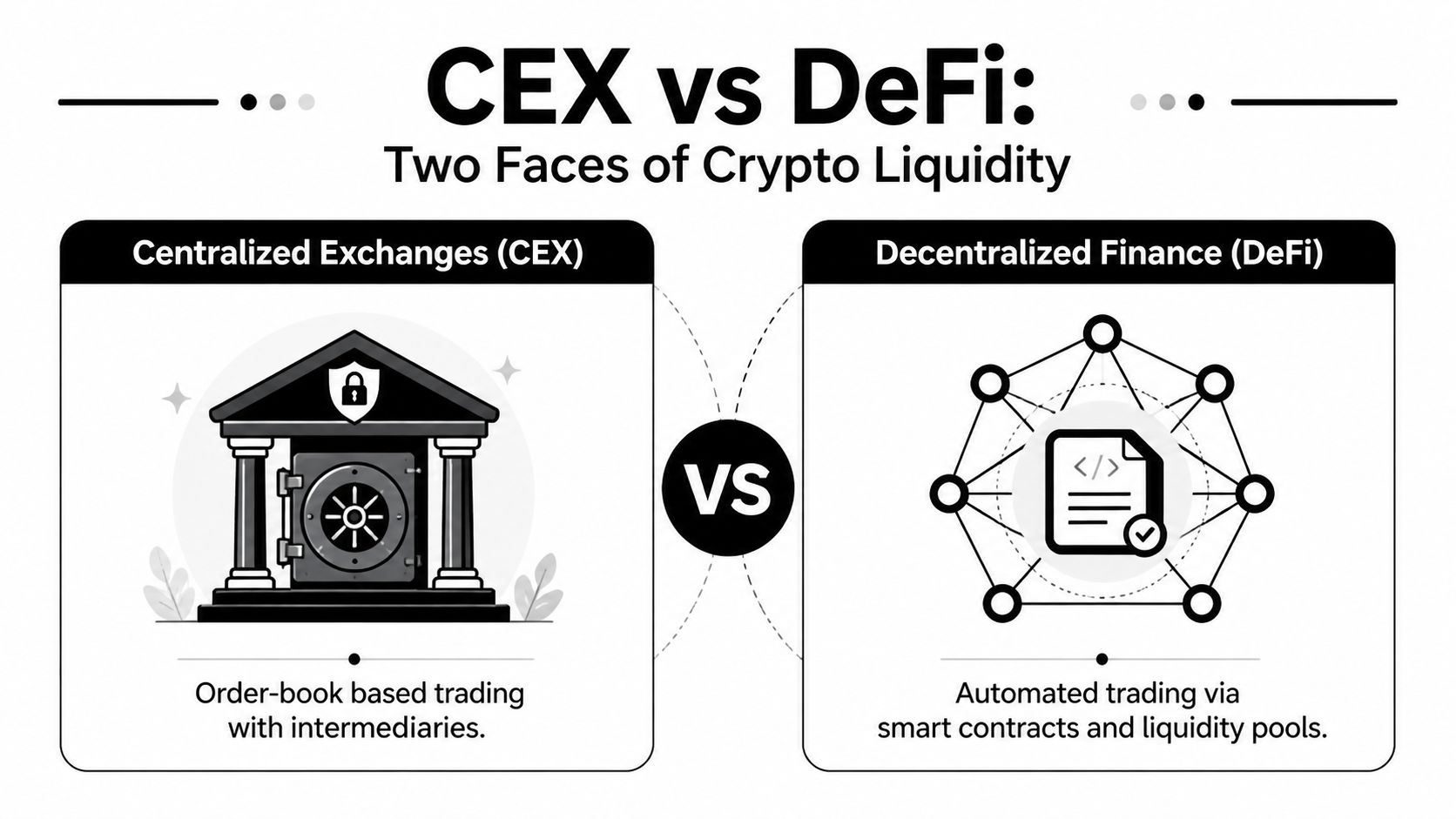

The Two Faces of Crypto Liquidity CEX vs DeFi

A prop trader can be right on direction and still lose money on venue choice. Buy a liquid BTC perp on a strong centralized book, and the fill is usually close to the screen price. Try to push similar size through a thin DeFi pool, and the entry itself can take a meaningful bite out of the trade before the market even moves.

How CEX liquidity works

Centralized exchanges run on order books. Buyers post bids, sellers post offers, and matching happens at visible price levels. For an active trader, that visibility matters because execution risk is easier to judge before the order is sent. You can see whether size is stacked near the market or whether the book thins out a few ticks away.

That structure usually fits short-term trading better, especially on major pairs. Limit orders, partial exits, tighter stop management, and repeated intraday entries are easier to control when the book is deep and updates cleanly. The trade-off is that liquidity still varies by exchange, by contract, and by time of day. A pair can look tradable on one venue and sloppy on another.

How DeFi liquidity works

DeFi usually routes trades through automated market makers and liquidity pools instead of a traditional order book. You are not hitting a visible stack of bids or offers. You are swapping against pool inventory, and price adjusts as your order moves through that pool.

That creates a different risk profile. Execution can deteriorate quickly once order size becomes large relative to pool depth. Fees, slippage settings, pool composition, and smart contract risk all matter alongside price direction. For traders looking at newer listings or niche pairs, DeFi can provide access that major centralized venues do not. A practical example is Pancakeswap Klink Token trading, where access matters, but sizing discipline matters more.

Desk habit: Treat trade access, fill quality, and exit capacity as separate checks before putting on risk.

CEX order books vs DeFi AMMs A Trader's Comparison

| Feature | Centralized Exchanges (CEX) | Decentralized Exchanges (DEX/AMM) |

|---|---|---|

| Trading mechanism | Order book with bids and offers | Liquidity pool with automated pricing |

| Price visibility | Usually clearer near the current market | Often harder to judge before execution |

| Execution feel | Better suited to fast active trading on major pairs | More sensitive to pool depth and swap size |

| Asset coverage | Strong on major coins and widely listed pairs | Strong on long-tail tokens and early listings |

| Main trader risk | Venue fragmentation, hidden weakness outside top pairs | Slippage, pool imbalance, smart contract risk |

| Best use case | Short-term strategies needing cleaner fills | Accessing assets outside major exchange listings |

Which one works better

For most funded traders, CEX liquidity is easier to manage because the path from entry to exit is more predictable on major instruments. That predictability matters when daily loss limits and trailing drawdown rules leave little room for execution mistakes.

DeFi has a place, but it demands tighter controls. Smaller size, wider assumptions for slippage, and stricter venue selection are standard risk adjustments. The same token can trade cleanly on one venue and poorly on another, so the key question is not where the chart looks attractive. The key question is where the order can be executed, defended, and closed without turning friction into avoidable drawdown.

Key Metrics for Measuring Liquidity

A market can look active on the chart and still trade badly at your size. For funded traders, that distinction matters because liquidity is not a theory problem. It shows up in entry cost, stop execution, and whether a manageable loss stays inside the firm’s rules.

Bid-ask spread

Spread is the first number to check because it is the cost of crossing the market right now. If the gap between bid and ask is wide, the trade starts with friction before price even moves.

Crypto.com explains in its guide to liquidity in crypto markets that tighter spreads usually reflect better liquidity and lower transaction cost, while wider spreads tend to signal weaker market quality.

In practice:

- Narrow spreads reduce immediate cost.

- Wide spreads force the trade to work harder just to break even.

- Unstable spreads often warn that liquidity is thinning even if the chart still looks orderly.

For short-term traders, spread discipline is basic risk control. A setup that looks attractive on price alone can be poor once the spread is included.

Order book depth

Depth answers a different question. It shows how much size is available near the current market, not just the best displayed bid and ask.

That matters because two markets can show the same spread and still behave very differently once real size hits the book. One absorbs the order cleanly. The other moves several levels and turns a normal entry into a chase.

This is one reason execution benchmarks matter. Traders who track fill quality against session averages often use tools like what VWAP is and how traders use it to judge whether entries are slipping away from fair execution during active periods.

Slippage

Slippage is the metric that hits P&L directly. It is the gap between the price planned and the price filled.

The usual causes are operational, not mysterious:

- Thin liquidity near the touch

- Fast tape where resting orders disappear

- Order size that is too large for current depth

- Weak venue selection for the pair

Many newer funded traders encounter a significant challenge. They calculate risk from the chart, then enter with a market order into a thin book and discover their real exposure is larger than planned. If the account has a strict daily loss cap, a few bad fills can do more damage than a wrong directional call.

Trading volume

Volume helps confirm whether participation is broad enough to support consistent trading. It is useful, but it should not be treated as a standalone liquidity signal.

A pair can print strong daily volume and still trade poorly at certain hours or on a weaker venue. What matters is where that volume sits, how regularly it trades, and whether it supports your size without forcing price to move.

For prop-style risk management, volume is best used as a filter. It helps narrow the list of tradable markets, then spread and depth decide whether execution is acceptable.

For DeFi traders, pool quality matters too

On decentralized venues, liquidity is shaped by pool reserves, swap size, and pricing mechanics rather than a central order book. Traders who are still learning that side of execution should first understand decentralized finance basics, because the same order can behave very differently in a pool than on a major exchange.

A practical pre-trade check is simple:

- Review the live spread or quoted swap output.

- Check how much size sits close to the current price, or how sensitive the pool is to your order.

- Compare the same pair across venues.

- Cut size if the exit looks less certain than the entry.

That process protects capital. It also protects evaluation accounts, where execution mistakes count against you just as much as bad reads.

How Liquidity Impacts Trading Execution and Risk

Most traders learn about liquidity after it hurts them. They don’t notice it in strong conditions. They notice it when a fill is bad, a stop slips, or an exit takes far more price movement than expected.

Low liquidity turns execution into risk

Liquidity affects risk in two ways. First, it raises direct cost through spread and slippage. Second, it increases instability because thin markets react harder to small order flow.

Chiliz’s article on understanding crypto liquidity notes that assets with lower trading volumes show sharper price swings from small trades or news events, while high liquidity dampens volatility by keeping enough buyers and sellers active at competitive prices.

For active traders, that means a low-liquidity market can break your plan even if your market view is right. You may catch direction and still underperform because execution quality is poor.

Where traders usually get caught

The common failure points are operational:

- Market orders in thin books. The order sweeps levels and fills worse than expected.

- Stops placed in unstable markets. The exit triggers into weak liquidity and slips.

- Oversized positions. The trader sizes for chart risk, not execution risk.

- Ignoring spread changes. The setup looks valid, but cost expansion ruins the trade.

If you need a refresher on the mechanics behind quoted prices, this guide on the difference between bid and ask helps explain why execution cost starts before slippage even appears.

Practical controls that help

Use these controls when liquidity is uncertain:

- Prefer limit orders when possible. A limit order won’t guarantee a fill, but it helps control price. This works best when you care more about execution quality than immediate entry.

- Reduce size in thinner markets. Smaller size lowers your own price impact. This matters most in altcoins and niche pairs.

- Test exits before scaling in. Traders often focus on entry liquidity and ignore exit liquidity. If you can’t get out cleanly, the setup is weaker than it looks.

- Avoid chasing fast moves. Thin markets often look most attractive after they’ve already expanded. That’s when slippage risk is highest.

- Check venue conditions in real time. Don’t assume yesterday’s execution quality still exists today.

A trade isn’t low risk because the stop is small on the chart. It’s low risk only if the market can actually fill you near that stop.

Practical Strategies to Manage Liquidity Risk

A funded trader can be right on direction and still fail the trade on execution. The setup works on the chart, but the venue cannot handle the order cleanly, the fill comes in late, and the extra slippage pushes the loss past what the model allowed. That is a liquidity problem, not an analysis problem.

The practical fix is to treat liquidity checks as part of pre-trade risk control. If a market cannot take your size at an acceptable cost, it does not fit the trade, no matter how clean the setup looks.

Use the right order type

Order type is a risk decision.

Market orders buy immediacy, but they also hand price control to the book or pool in front of you. In thick markets, that cost may be small. In thin markets, especially around news, liquidations, or fast breakouts, that cost can turn a planned scalp into a poor trade before the position has room to work.

Limit orders make more sense when:

- Fill price matters more than instant entry

- Depth near the top of book is uneven

- You are building size over time

- Missing the trade is cheaper than getting filled badly

That last point matters for prop traders. A missed trade does not hit the drawdown. A bad fill does.

Choose the venue before choosing the trade

The same coin can trade well on one venue and poorly on another. Spreads, visible depth, refill speed, and slippage can differ enough to change whether the trade is viable.

Do the venue check first:

- Compare spreads across the exchanges or pools you can access.

- Check how much size sits near the current price.

- Watch how the book or pool reacts when trades hit.

- Skip venues where liquidity disappears as soon as volatility rises.

As noted earlier, broader participation usually translates into better execution. For a trader working under strict loss limits, venue quality is part of risk selection, not a technical detail.

Match your size to actual market capacity

A common mistake is sizing only from stop distance and account risk. That ignores the cost of getting in and out.

Size should reflect what the market can absorb without forcing you into avoidable slippage. In practice, that means full size in majors may be acceptable, partial size in mid-tier pairs may be smarter, and some thin altcoins should be left alone entirely. If your exit would move the market against you, the position is too large for the venue.

Many evaluation accounts suffer damage in such scenarios. The chart shows a controlled 0.5% risk. The executed loss ends much larger because the market could not fill the stop anywhere close to plan.

Trade at times when liquidity is actually there

Liquidity shifts through the day. A pair that trades smoothly during active hours can become expensive and erratic during off-peak sessions, around listings, or during sudden macro headlines.

Before entry, check:

- Whether spreads are stable or expanding

- Whether depth is stacked close to price or far away

- Whether recent aggressive orders caused outsized moves

- Whether the market refills quickly after prints

If those conditions are deteriorating, the best adjustment is often simple. Reduce size or stand down.

Build a liquidity rule into your playbook

Good traders do not rely on judgment alone when markets speed up. They set rules in advance. For example: no market orders above a certain size in secondary pairs, no first entries during spread expansion, no trading venues that repeatedly slip stops beyond a defined tolerance.

Those rules protect P&L, but they also protect consistency. A prop trader needs repeatable execution, because inconsistent fills make it harder to judge whether the strategy has an edge or the venue is distorting results.

A simple liquidity checklist

Before placing a crypto trade, ask:

- Can this market take my size without a large price concession

- Is the spread still acceptable after recent volatility

- Does my order type match current conditions

- Would this trade still make sense if the exit slips

- Is this venue reliable enough for a funded account rule set

If the answer is unclear, pass. In prop trading, protecting execution quality is part of protecting the account.

Conclusion Your Edge in a Liquid Market

Understanding what does liquidity mean in crypto changes how you trade. You stop looking only at chart patterns and start judging whether the market can support your idea with acceptable execution.

That shift matters. Liquid markets make risk easier to define, entries easier to control, and exits more reliable. Thin markets do the opposite. They hide costs, distort sizing, and create losses that don’t show up in the setup itself.

Algorithmic traders should treat liquidity as a strategy input, not an afterthought. DeFi users should treat pool quality as part of trade validation, not a technical detail. In both cases, execution risk is real.

Trading involves risk of loss. This article is educational only and not financial advice.

Frequently Asked Questions About Crypto Liquidity

| Question | Answer |

|---|---|

| What does liquidity mean in crypto in one sentence? | It is the market's ability to absorb your order at or near the quoted price without forcing you into a worse fill. |

| Why can the same coin feel liquid on one exchange and illiquid on another? | Order flow, market maker activity, and depth are venue-specific. A coin can trade actively on one exchange and still have wide spreads or thin size on another. For a prop trader, that difference shows up in slippage, missed exits, and avoidable drawdown. |

| Is high volume enough to prove a coin is liquid? | No. Reported volume does not tell you how much size is sitting near the best bid and ask. Check spread, top-of-book depth, order book resilience after a sweep, and the slippage your actual ticket size would create. |

| Does liquidity matter for algo traders and copy traders? | Yes. Small execution costs can wipe out a strategy that looks fine in backtests. If your model relies on tight entries, quick exits, or frequent rebalancing, liquidity is part of the edge and part of the risk model. |

| Why does liquidity matter more in a funded account? | Funded traders operate under hard loss limits. A poor fill is not just a trading cost. It can push an otherwise valid setup closer to the daily drawdown line, especially in fast markets or lower-depth alt pairs. |

| What is the fastest practical way to check liquidity before entering? | Look at the spread, visible depth near the inside market, recent trade size, and how price reacted to the last few impulsive moves. If the book looks thin or the spread expands every time momentum picks up, reduce size or skip the trade. |

If you want to apply disciplined execution in a prop environment, explore the funding programs at MyFundedCapital. You can compare account types, review the risk parameters, and start a challenge built for traders who take execution, drawdown control, and consistency seriously.