Most advice on how to get venture capital funding is backwards. It starts with pitch decks, networking, and founder theater, when the first question is much simpler. Should you even be chasing VC at all?

If you're a trader, quant, or builder in market infrastructure, the answer depends on the business model, not your ambition. VC is one lane. Prop funding, bootstrapping, angels, revenue financing, and customer-funded growth are other lanes. Pick the wrong one and you'll waste months talking to people who were never going to fund you.

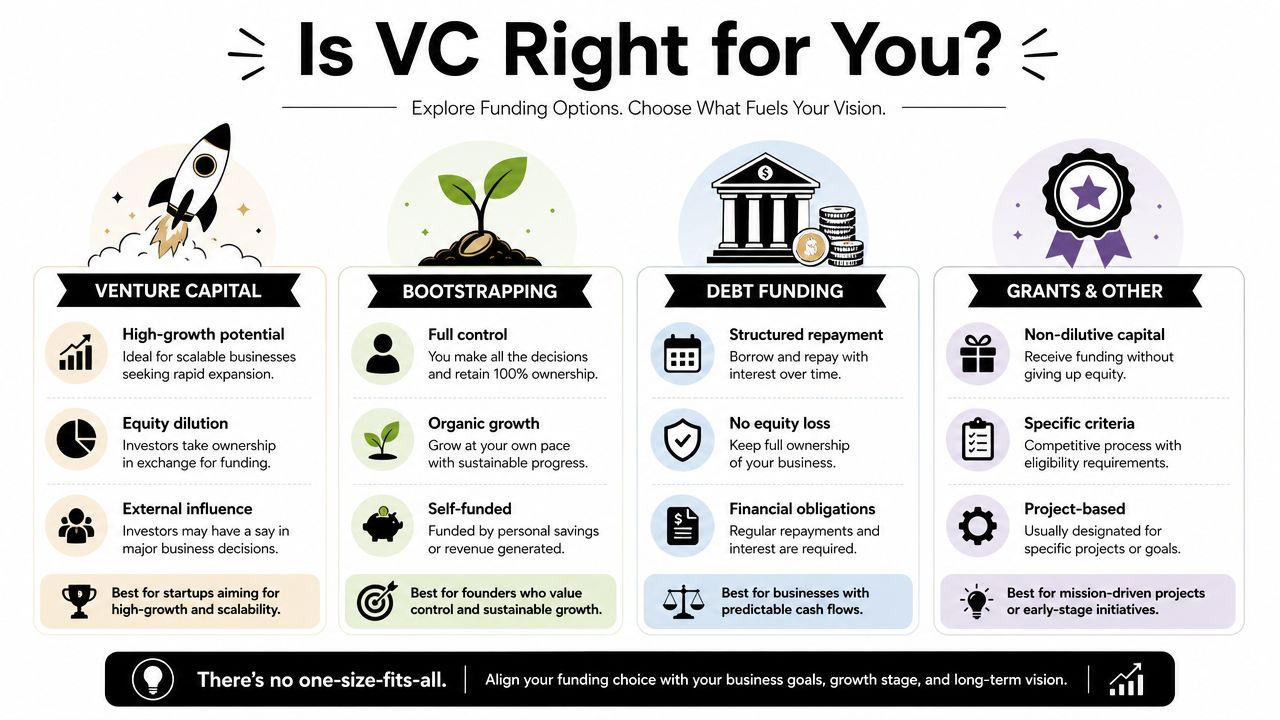

Is Venture Capital Really the Right Fuel for Your Engine

A lot of traders assume VC is the premium form of capital because it sounds institutional. That's the wrong mental model.

VC is not “money for promising people.” VC is risk capital for scalable companies that can become very large and exit through acquisition or IPO on a relatively compressed timeline. In the U.S., the market is big, but still selective. In 2023, 3,417 venture firms invested $170.6 billion across 13,608 deals, and investors historically targeted 25% to 35% annual returns over the life of an investment, according to the NVCA Yearbook. That should tell you everything. VCs don't need a good small business. They need a company that can move the needle for a fund.

What VCs actually want

If you strip away the jargon, most VC screening comes down to four questions:

- Can this scale fast? A software product, infrastructure layer, exchange tool, or fintech workflow can. A discretionary personal trading strategy usually can't.

- Can this serve a large market? “Traders need this” isn't enough. You need a market big enough to justify institutional time.

- Is there proof already? Not perfection. Proof.

- Can this become a big exit? If the best outcome is “nice cash-flow business,” many VCs will pass.

For traders, this distinction matters a lot. A personal trading account, even a strong one, is usually not venture-backable. A risk engine, broker infrastructure layer, execution analytics platform, retail trading SaaS, or compliance workflow might be.

Practical rule: If capital mostly helps you trade your own book, VC is usually the wrong source. If capital helps you build a repeatable product that other people will use, VC may fit.

What traders should compare instead

Here's the clean way to understand it:

| Funding path | Best for | Main tradeoff |

|---|---|---|

| Venture capital | Scalable platforms and products | Dilution and investor control |

| Bootstrapping | Early product validation | Slower growth, full founder burden |

| Debt funding | Predictable cash flows | Repayment pressure |

| Grants and other | Specific research or niche programs | Restrictions and narrow eligibility |

There's also a category many trading founders overlook: direct access to trading capital through specialized funding models. If your edge is execution rather than company-building, comparing venture money with capital options for funded projects is just rational. Don't raise equity to solve a problem that's really about access to deployable capital.

The hard truth

VC is one tool for one job. If you're building a venture-scale company, go after it seriously. If you're trying to scale your trading performance, build track record, or prove risk discipline, a more direct capital model often makes more sense.

Confusing those two paths is where founders lose time.

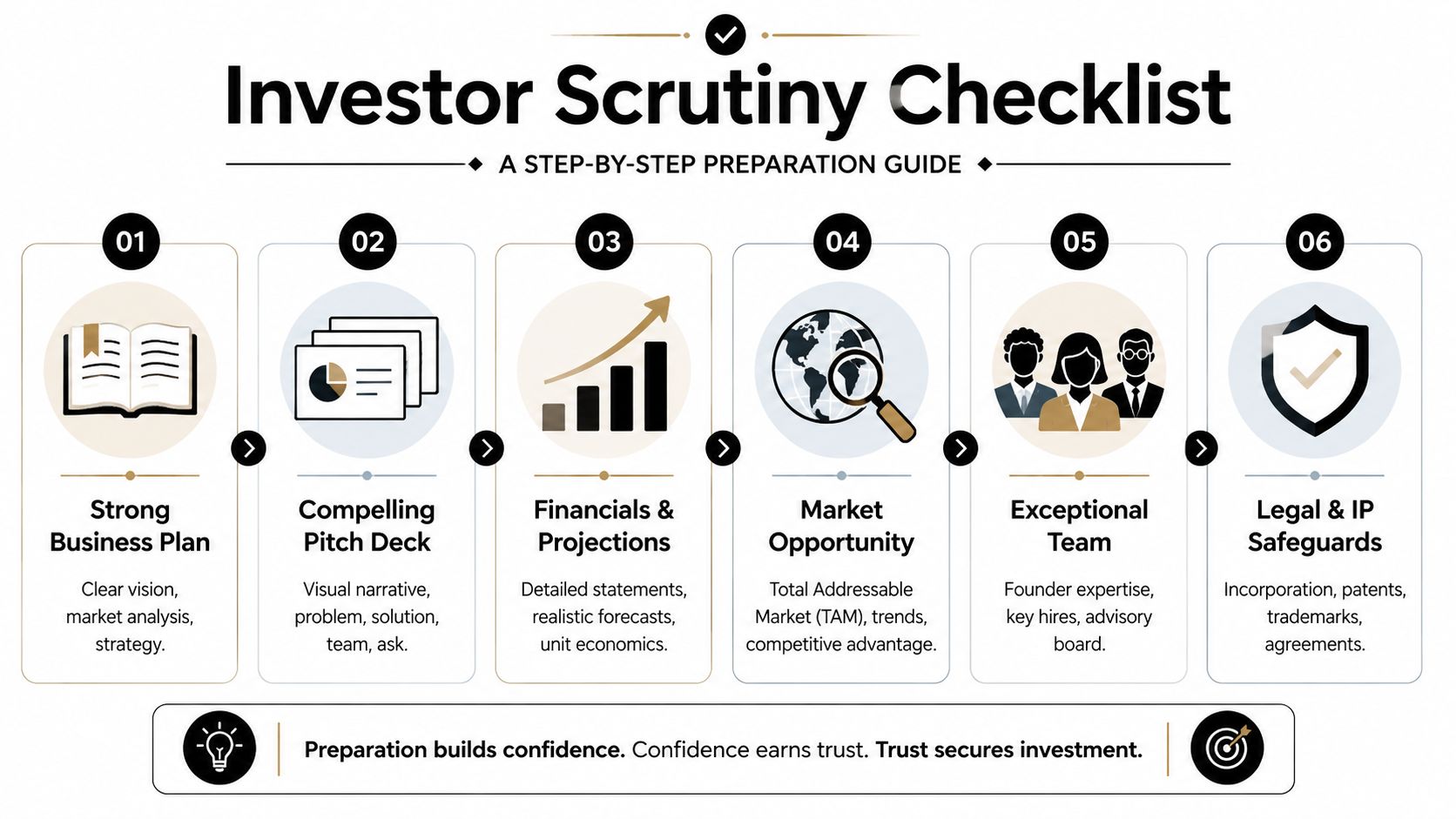

Preparing Your Venture for Investor Scrutiny

Investors don't fund effort. They fund setups.

A trader understands this immediately. Before putting on size, you want context, confirmation, and a defined risk case. Investors think the same way. If you want to learn how to get venture capital funding, stop obsessing over deck design and start building an evidence package.

A core rule of VC is simple. Investors fund scalable businesses with a path to a meaningful exit in about a decade, and they want evidence the idea is already working. The same source also notes how uneven access can be. Historically, all-female founding teams have received only 2.4% of all VC funding, as highlighted in Stripe's venture capital guidance. Don't ignore that reality. Fundraising is not a pure meritocracy. It's performance, pattern-matching, and access.

Build the case before you ask for money

Founders usually show up one layer too early. They have a concept, a vision, maybe a prototype, and they expect investors to underwrite the missing proof. Most won't.

You need three things tight before the first serious meeting:

Narrative

Your story has to answer these points without wandering:

- What problem are you solving

- Why does this problem matter now

- Why is your product better than the current workaround

- Why are you the team to build it

- Why does this become large enough for venture returns

That isn't brand copy. It's your investment thesis in plain English.

Numbers

You don't need spreadsheet theater. You do need a model that shows you understand the machine.

Investors will look for:

- Revenue logic if you have it

- User behavior if revenue is early

- Unit economics if you're selling anything

- Cash needs and milestone use of funds

- What changes after this round

If you're a quant founder, many of you will reach a point where you either shine or self-destruct. You can drown a room in detail. Don't. Show signal, not every variable.

A useful mental shortcut is the same one traders use for P&L discipline. Tie each major spend to an expected business outcome. If your model is sloppy, clean it up before you pitch. This basic profit and loss formula guide is simple, but the underlying principle matters. Investors want to see that you understand what drives gains, what creates losses, and how capital changes the curve.

Investors don't expect certainty. They expect coherence.

Team

Early-stage investors are betting on people under uncertainty. That means your team slide matters more than founders like to admit.

Show:

- relevant domain experience

- technical build ability

- distribution or market access

- ability to recruit

- emotional stability under pressure

If the founding team hasn't sorted ownership, roles, and decision rights, fix that now. Messy cap tables and vague internal agreements kill trust. If you need a practical reference on equity distribution among founders, review it before investors find gaps for you.

What counts as traction

Pre-revenue doesn't mean pre-proof. Good early traction can include:

- A live product, even if narrow

- Pilot users with clear feedback loops

- Repeat usage that shows stickiness

- Strong user pull from a niche audience

- A measurable workflow improvement, stated qualitatively if you don't have clean benchmark data

- Partnership conversations that moved beyond polite interest

For trader-focused startups, traction might be active usage by a real cohort, integrations with execution platforms, retained users in a journaling or analytics product, or firms willing to test your infrastructure.

The prep checklist founders skip

Before the first serious process, have these ready:

- A sharp pitch deck

- A financial model you can defend live

- Customer or user references

- Clear incorporation and IP ownership

- Founders agreement

- A concise use-of-funds plan

- One-line answers to obvious objections

If you don't have those, you're not fundraising. You're rehearsing in public.

How to Find and Target the Right Investors

Most founders make investor outreach far too broad. They build a giant spreadsheet, blast the same note to everyone, then conclude the market is cold. The market isn't cold. Their targeting is bad.

Fundraising works better when you treat it like a pipeline, not a lottery. One practical playbook recommends building your investor pipeline 12 months before you need capital and using 20 to 30 warm intro requests to create 10 to 15 actual introductions, which can lead to 8 to 12 first meetings. That implies a 50% to 75% warm-intro conversion rate when fit and network quality are strong, based on this venture fundraising workflow.

Build an investor list like a trader builds a watchlist

Don't ask, “Who invests in startups?” Ask, “Who invests in my exact setup?”

Filter for:

Stage fit

If they don't lead or participate at your stage, they're a distraction.Sector fit

Fintech is broad. Trading infrastructure, brokerage tooling, risk software, payments, and retail investing are different lanes.Check size fit

If your raise is too small or too large for the fund, the meeting is low-probability from the start.Geography and network fit

Some firms care about local density. Others don't.Partner fit

Firms don't invest. Partners do. One partner who knows your space is worth more than a famous logo with no internal champion.

If you need a research starting point, tools that help you discover startup investors can speed up list-building. But don't outsource judgment. Databases give names. You still need to qualify them.

Warm intros beat cold outreach, but only if the intro is real

A warm intro isn't “someone forwarded your deck.” A real warm intro does three things:

- explains why you fit that investor,

- signals the sender knows you,

- gives the investor a reason to take the meeting now.

Weak intros waste social capital. Strong intros create borrowed trust.

Here's the simplest way to ask for one:

- tell the connector why this investor fits

- give a short forwardable blurb

- attach deck only if requested

- make it easy to decline

Run outreach in waves, not all at once

Don't contact every target on the same day. That kills your ability to learn and improve.

Use a staggered process:

Wave one

Start with the highest-fit investors and strongest warm paths. These conversations sharpen your narrative.

Wave two

Move to the broader set once your story has tightened and your objections list is clearer.

Wave three

Follow up with people who asked for updates, passed for timing reasons, or wanted a milestone first.

Good fundraising momentum is manufactured. It comes from sequencing, not luck.

Track every conversation. Keep notes on objections, partner interest, timeline, and next step. If you can't manage an outreach CRM, investors will wonder how you'll manage a company.

Navigating the Pitch Meeting and Due Diligence

The meeting starts before the meeting.

An investor has usually skimmed your deck, checked your LinkedIn, looked at the market, and formed a preliminary view. The pitch meeting isn't where they first learn about you. It's where they test whether their early impression holds up under pressure.

What the room feels like

The first few minutes matter more than most founders think. You walk in, do the brief small talk, and then the investor wants one thing. They want the clean version fast.

Not your life story. Not every feature. Not your philosophical view on markets.

They want to understand:

- what you built

- who needs it

- why it wins

- why now

- what proof exists

- why this can become large

If you're a trader or quant founder, you may default to technical depth. Resist that urge. Use technical detail only when it supports the investment case.

How to structure the pitch

A strong meeting usually flows like this:

Start with the problem

Make it concrete. If the pain sounds vague, the opportunity sounds small.

Show the product simply

Demo only what proves the point. Don't click through every screen. A product demo should reduce doubt, not create confusion.

Explain why users care

Use customer behavior, workflow improvement, retained usage, pilots, or demand signals. Keep it grounded.

Cover the business model

How do you make money, or how will you? If revenue is early, explain the path cleanly.

Address the market and expansion logic

Show where the first wedge is and what broader market opens if you win there.

End with the ask

State how much you're raising, what it funds, and what milestone that capital should reach.

A pitch is not a product tutorial. It's an argument for why this company deserves capital now.

Handling hard questions

The uncomfortable questions are the meeting.

Expect pressure around:

- customer acquisition

- retention

- compliance or regulatory exposure

- concentration risk

- competitive moat

- technical defensibility

- founder-market fit

- timeline to meaningful traction

Answer directly. If you don't know, say so and explain how you'll find out. Evasive founders look dangerous.

One mistake I see often is defensiveness. Investors are stress-testing the position. Traders should recognize that instinct. Pressure reveals weak assumptions. Treat questions like risk review, not a personal attack.

Due diligence is where discipline shows up

If the meeting goes well, diligence starts. Many rounds often slow down during this phase because the founder is still building basic materials while trying to look polished.

Your data room should be organized before investors ask for it.

Include:

- corporate documents

- cap table

- financial statements and model

- customer contracts or pilots

- product roadmap

- IP assignments and legal docs

- team information and hiring plans

- compliance materials if relevant

- board materials if they exist

What investors are really checking

Diligence isn't just document collection. Investors are looking for consistency.

They compare:

- your deck versus your model

- your claims versus user evidence

- your cap table versus your story about control

- your hiring plan versus your burn logic

- your urgency versus your actual preparedness

A founder who answers quickly, sends clean documents, and stays consistent earns trust. A founder who changes the story mid-process usually loses it.

Understanding the Term Sheet and Closing the Deal

Getting a term sheet feels like the finish line. It isn't. It's the start of a negotiation that will shape your economics and control for years.

Founders often obsess over valuation because it's visible and flattering. That's a mistake. A high headline valuation can still produce a bad deal if the rest of the paper is ugly.

The terms that matter most

Valuation

Valuation matters, but not in isolation. What you care about is how much ownership you're giving up, what milestones the capital buys, and whether the next round becomes easier or harder because of today's pricing.

If you overprice the round and miss expectations, the next financing gets messy fast.

Liquidation preference

This term decides who gets paid first in an exit. Founders ignore it because it sounds legal. It's economic.

This resembles the payout order in a stacked trade. If the downside case happens, this term determines how proceeds flow before common shareholders see anything.

Board seats and control

Money comes with influence. Don't pretend otherwise.

A board seat changes how decisions get made, especially when things go sideways. You need investors who add pressure in a useful way, not chaos.

Founder vesting

Some founders act insulted by vesting. Don't. Investors want to know the founding team stays locked in after the round.

If a founder can walk away with a large equity stake while execution risk remains high, investors will push back.

The best term sheet isn't the one that feels best on signing day. It's the one you can live with through a hard year.

What to negotiate and what not to romanticize

Good founders know the difference between symbolic wins and structural wins.

Push hardest on:

- clean economics

- reasonable control terms

- clear governance

- founder alignment

- future financing flexibility

Don't burn trust fighting over every tiny point just to feel tough. Save your energy for the terms that compound over time.

Closing the round without losing momentum

Once legal starts, founders often disappear into documents and stop running the business. That's another mistake.

Keep operating. Keep hiring if needed. Keep customers moving. Investors get nervous when a company goes flat during a financing process.

Also, keep communication tight:

- confirm timelines

- respond fast to counsel

- clean up open diligence items

- avoid surprise disclosures late in the process

If something ugly exists, surface it early. Hidden problems kill deals. Known problems can sometimes be priced or structured.

Avoiding Pitfalls and Answering Key Questions

Most fundraising mistakes aren't dramatic. They're procedural. Founders talk too early, target the wrong firms, overtalk in meetings, and underprepare for scrutiny.

That's fixable if you're honest about where the process usually breaks.

The mistakes that burn rounds

Raising before you have proof

A concept isn't enough. In the current selective market, founders need tighter unit economics, clearer milestones, and stronger documentation than vague traction stories. Global VC deal count fell to around 35,660 in 2024, according to this overview of the current funding environment. Fewer deals means more scrutiny.Pitching the wrong business model to VC

If your venture doesn't scale like software or platform infrastructure, you may be forcing a fit that isn't there.Confusing product complexity with investor appeal

Advanced tech doesn't automatically mean venture-backable. The market and monetization still have to work.Ignoring risk discipline

Founders who can't explain operating risk, customer concentration, burn exposure, or execution bottlenecks look immature. The same habits behind solid trading discipline also apply in company-building. Basic risk management practices are not optional.Running a messy process

Slow replies, inconsistent numbers, and missing documents signal operational weakness.

What proof is enough right now

There isn't one universal benchmark, and anyone pretending there is is selling certainty that doesn't exist.

For most early-stage companies, “enough proof” means investors can see three things clearly:

- real demand

- credible execution

- a believable path to a bigger business

If you're pre-revenue, proof might be user behavior, active pilots, strong retention in a narrow niche, or serious design-partner engagement. If you have revenue, the bar shifts toward quality of revenue, repeatability, and economic logic.

If an investor has to imagine all the proof for you, you're too early.

FAQ

Can a trader raise venture capital for a trading strategy

Usually no. A personal or small-team trading strategy is generally not what VC funds want. They tend to back scalable products and platforms, not capital allocation to an individual trading edge.

Is a fintech or trading tool more venture-backable than a trading record

Yes. A tool, platform, analytics layer, execution system, or infrastructure product can scale across users. That fits the venture model much better than a strategy that depends on your own decisions.

Should I bootstrap before trying to get venture capital funding

In many cases, yes. Bootstrapping enough to build a product, validate demand, or secure early users strengthens your position. It also tells you whether the business deserves institutional capital or just disciplined self-funded growth.

What if I need capital now, not a long fundraising process

Then be honest about the problem. If you need deployable trading capital, VC is often too slow and structurally mismatched. If you need company-building capital for a scalable startup, begin the process early because fundraising rarely moves as fast as founders want.

If your real goal isn't building a venture-backed startup, but getting access to more trading capital under clear rules, take a look at MyFundedCapital. You can compare funding paths, account types, and evaluation models that fit active traders, algo traders, and disciplined risk-takers. Trading involves risk of loss, and this article is educational only, not financial advice. If you want a more direct route than equity fundraising, start by reviewing their programs and choose the structure that matches how you trade.