You've passed KYC, paid for a challenge or requested a payout, and then compliance asks for source of funds verification. That's the moment most traders get annoyed, mostly because it feels like you've already proved who you are.

You haven't proved where the money for a specific transaction came from. That's what this check is for. If you understand what the team is looking for and submit the right evidence the first time, the process is usually much smoother.

What Source of Funds Verification Is and Why It Is Required

Source of funds verification means showing where the money used in a specific transaction came from. Not your identity. Not your overall net worth. The actual origin of the payment, deposit, or transfer being reviewed.

That distinction matters. A compliance team may already know your name, address, and ID details through KYC, but still need to verify the money behind a challenge payment, a large transfer, or a payout-related review.

Source of funds is not the same as source of wealth

A lot of traders mix up source of funds and source of wealth.

| Term | What it asks | Simple example |

|---|---|---|

| Source of funds | Where this specific money came from | “This payment came from salary saved in my bank account” |

| Source of wealth | How you built your overall wealth over time | “My overall assets came from work, trading, and business income” |

A firm can accept that you're generally financially legitimate and still reject a specific transaction if the incoming money can't be explained. That transaction-specific approach is standard in AML practice, and firms are expected to connect a payment to a lawful origin rather than rely on identity alone, as outlined in this overview of source of funds and modern AML expectations.

Why firms ask for it

From a trader's side, it can feel excessive. From a compliance side, it's routine.

A source of funds check exists because regulated businesses have to reduce exposure to fraud, money laundering, and terrorism financing. That's why firms look beyond a clean passport scan and ask whether a transaction fits your profile, your stated occupation, and your document trail.

Practical rule: If the money story only makes sense when you explain it verbally, your documents probably aren't strong enough yet.

High-value transactions, unusual inflows, third-party payments, and activity that doesn't match the customer profile tend to trigger closer review. If you want a wider view of how customer due diligence works in practice, including typical warning signs, this guide to AML obligations and CDD red flags is a useful companion read.

How traders should think about it

The fastest way to get through source of funds verification is to stop treating it like a personal challenge and start treating it like an audit trail.

Compliance teams usually aren't asking, “Are you a good trader?” They're asking:

- What was the original source?

- Can the documents show the path clearly?

- Do the names, dates, and amounts line up?

- Does the explanation match the transaction pattern?

If the answer is yes, the review is straightforward. If the trail breaks halfway, the team asks for more.

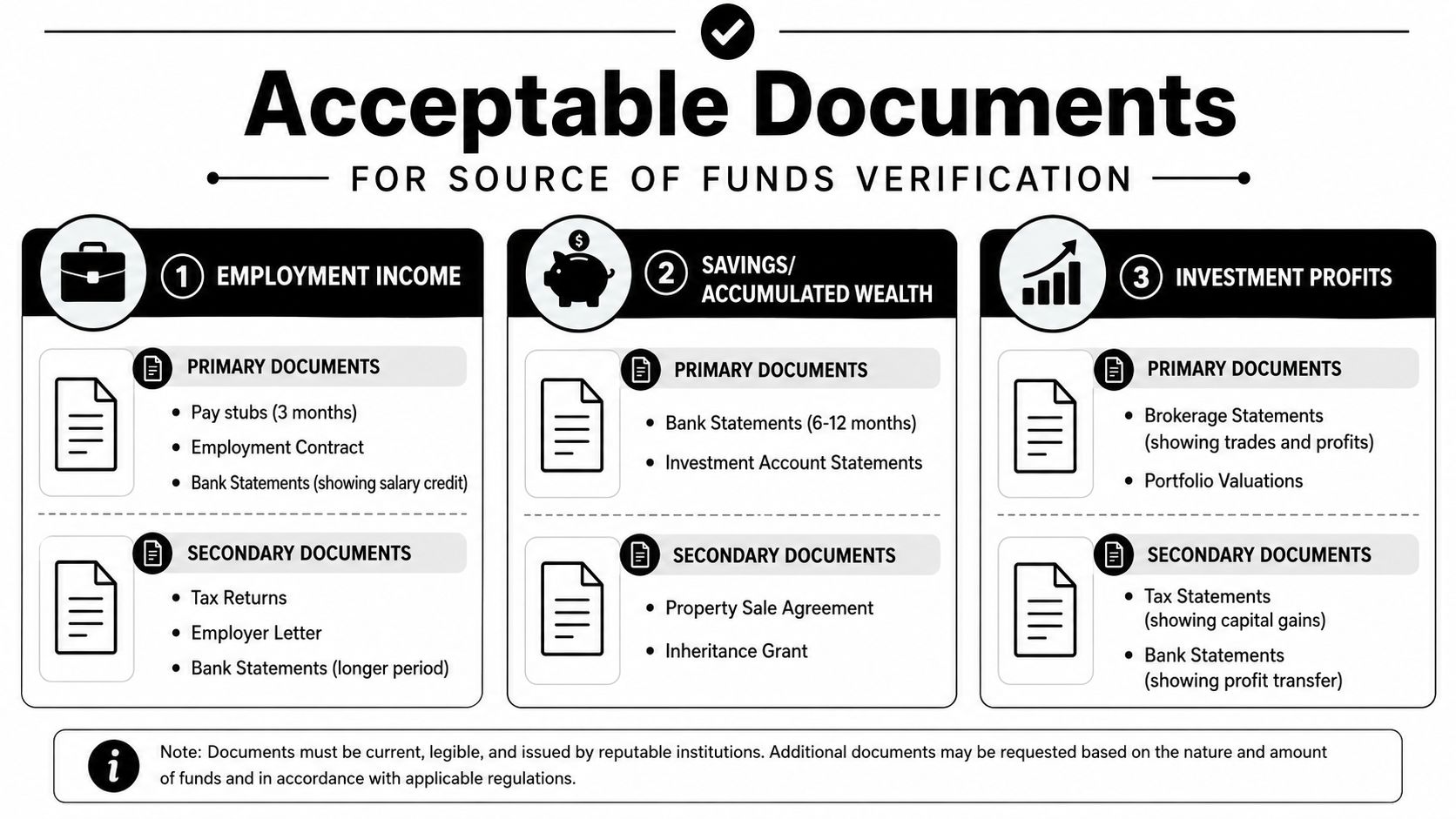

Acceptable Documents for Common Funding Sources

Most rejections happen because traders upload one document when the payment needs a document chain. A bank statement showing a balance is often not enough by itself. The better approach is to prove both the origin and the path.

Employment income and accumulated savings

If your trading-related payment came from salary or long-term savings, keep it simple and traceable.

- Employment income: Recent payslips, your employment contract, and bank statements showing salary credits.

- Savings built from income: Bank statements over time showing funds accumulating, not just appearing suddenly.

- Helpful support: Tax records can help if your salary or self-employment income needs extra context.

A good submission tells one story. Example: payslip shows employer and amount, bank statement shows matching salary deposits, current account shows funds used for the transaction.

Sale of assets and investment proceeds

If the funds came from selling something, prove both the sale and the receipt.

- Property or vehicle sale: Sale agreement, transfer confirmation, bank statement showing proceeds received.

- Brokerage or investment profit: Account statements showing holdings sold, realized proceeds, and transfer into your bank.

- Business-related asset sale: Contract plus business account statement plus transfer into your personal account if applicable.

Sending only the final bank statement often leads to failure for traders. A large credit with no sale document behind it leaves a gap.

Gifts, inheritance, and unusual one-off funds

These are valid sources. They just need more explanation.

- Gift from family or partner: Signed gift letter, donor ID if requested, donor bank statement showing transfer, your statement showing receipt.

- Inheritance: Probate-related documents, executor communication, bank evidence of distribution.

- Lottery or betting proceeds: You'd want official payout evidence and bank proof of receipt. If you're dealing with tax treatment questions around winnings, this summary from Australia Wide Tax Solutions on lottery income is useful context.

The compliance problem isn't that the source is unusual. It's that unusual sources are often documented badly.

Business profits and self-employed income

Self-employed traders, freelancers, and business owners need to show commercial logic.

- Primary evidence: Business bank statements, invoices, contracts, and payment receipts.

- Secondary support: Tax filings, company ownership records, or accounts that support the business activity.

- Best practice: If money moved from a business account to a personal account, show that transfer clearly.

Don't just label a transfer “business income” and assume that's enough. The reviewer will usually want to see the customer, invoice, payment, and onward movement.

Crypto source of funds

Crypto is where generic advice breaks down. For more complex cases like crypto, acceptable evidence may include exchange histories, wallet records, mining payout history, or employment contracts for crypto-paid work, because AML guidance treats source of funds as transaction-specific and expects the money trail to connect end-to-end, as explained in this practical guide to proof of source of funds.

Use a layered submission:

- Exchange records: Deposit and withdrawal history, trade history, account ownership details.

- Wallet evidence: Wallet screenshots or explorer references that align with your transfers.

- Original acquisition proof: Fiat purchase records, mining payouts, staking records if available, or employment evidence if paid in crypto.

- Conversion proof: If crypto was sold for fiat before the payment, show the exchange sale and bank receipt.

A clean crypto explanation can look like this:

“Funds used for this payment came from BTC sold on Exchange A. The BTC was originally purchased from my personal bank account over time. Attached are my exchange account history, wallet transfer records, and bank statement showing fiat received after sale.”

That kind of note helps because it tells the reviewer exactly how to read the file.

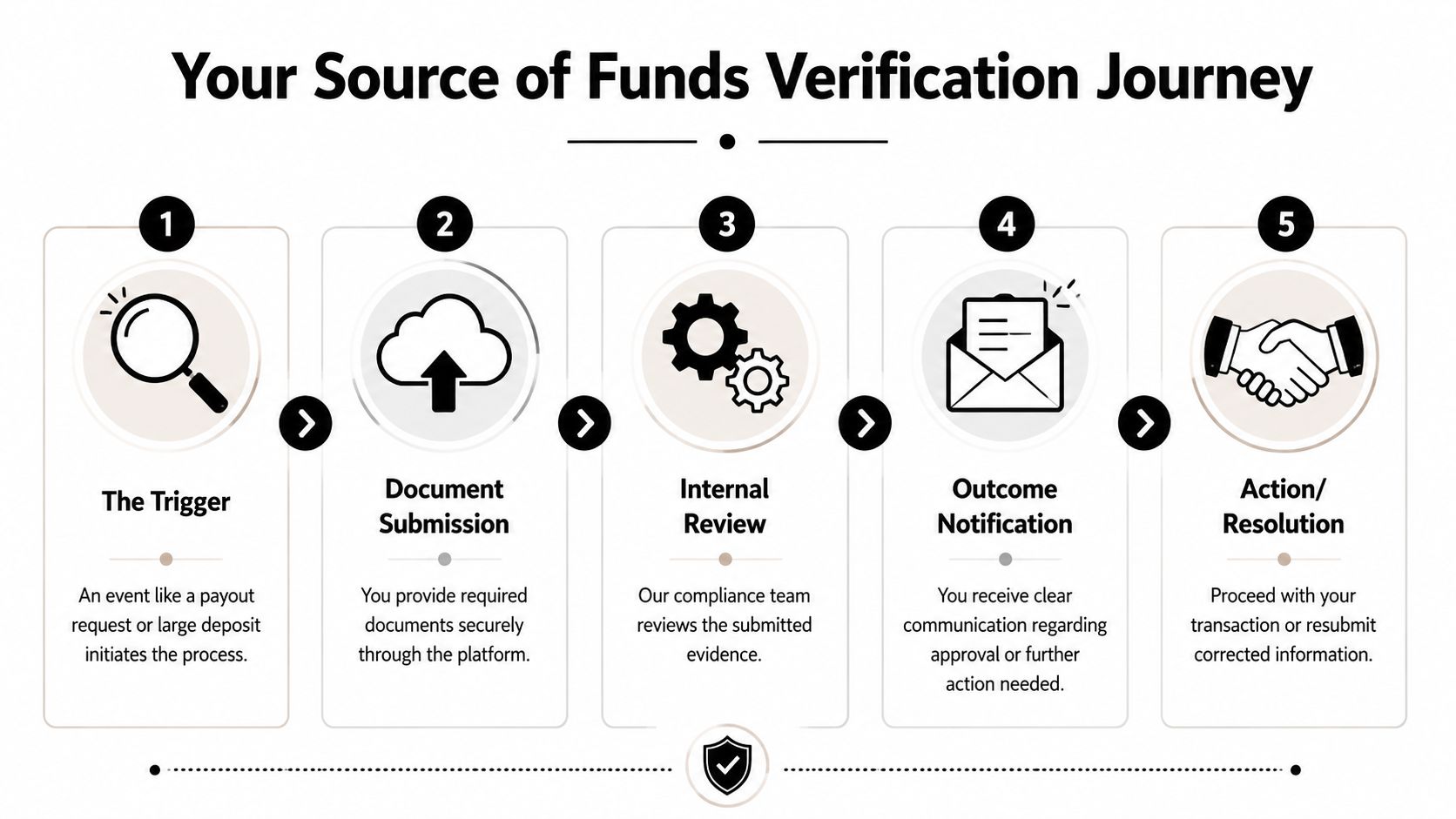

The Verification Process Step by Step

Most traders are less frustrated by the check itself than by not knowing what happens next. In practice, the workflow is usually predictable.

The five stages you'll usually go through

A trigger happens

Common triggers include a first payout request, an unusual funding pattern, a larger payment, a third-party transfer, or activity that doesn't match the profile on file.You receive a request

The message usually asks for documents tied to a declared source such as salary, savings, business income, gift, loan, or crypto.You upload documents securely

Good platforms use structured submission rather than random email attachments. If you're trying to understand what that workflow typically looks like, this overview of the account verification process is a useful reference point.Compliance reviews for consistency

The reviewer checks whether the documents support the stated origin, whether the transfer path makes sense, and whether names, dates, and amounts align.You get an outcome

Usually one of three things happens: approved, request for more information, or rejected with a reason to fix.

What determines speed

Historically, these checks were manual and document-heavy. Some providers now report that open-banking-enabled reviews can be completed “almost instantly”, which shows how much source of funds verification has shifted toward near-real-time analysis of account inflows and transaction history in some workflows, according to Veriphy's description of open-banking-enabled SoF reviews.

That said, speed depends on complexity.

| Scenario | Typical review experience |

|---|---|

| Simple salary or savings case | Often faster if the documents are complete |

| Business income with multiple transfers | Usually needs closer manual review |

| Crypto or third-party funding | Often slowed down by missing chain-of-funds evidence |

What helps the reviewer most

A short cover note can save time. Include:

- What the funds came from

- Which attached documents prove it

- How the money moved from source to payment

- Anything unusual that needs context

If a reviewer has to guess which transaction matters, you've made the file harder than it needs to be.

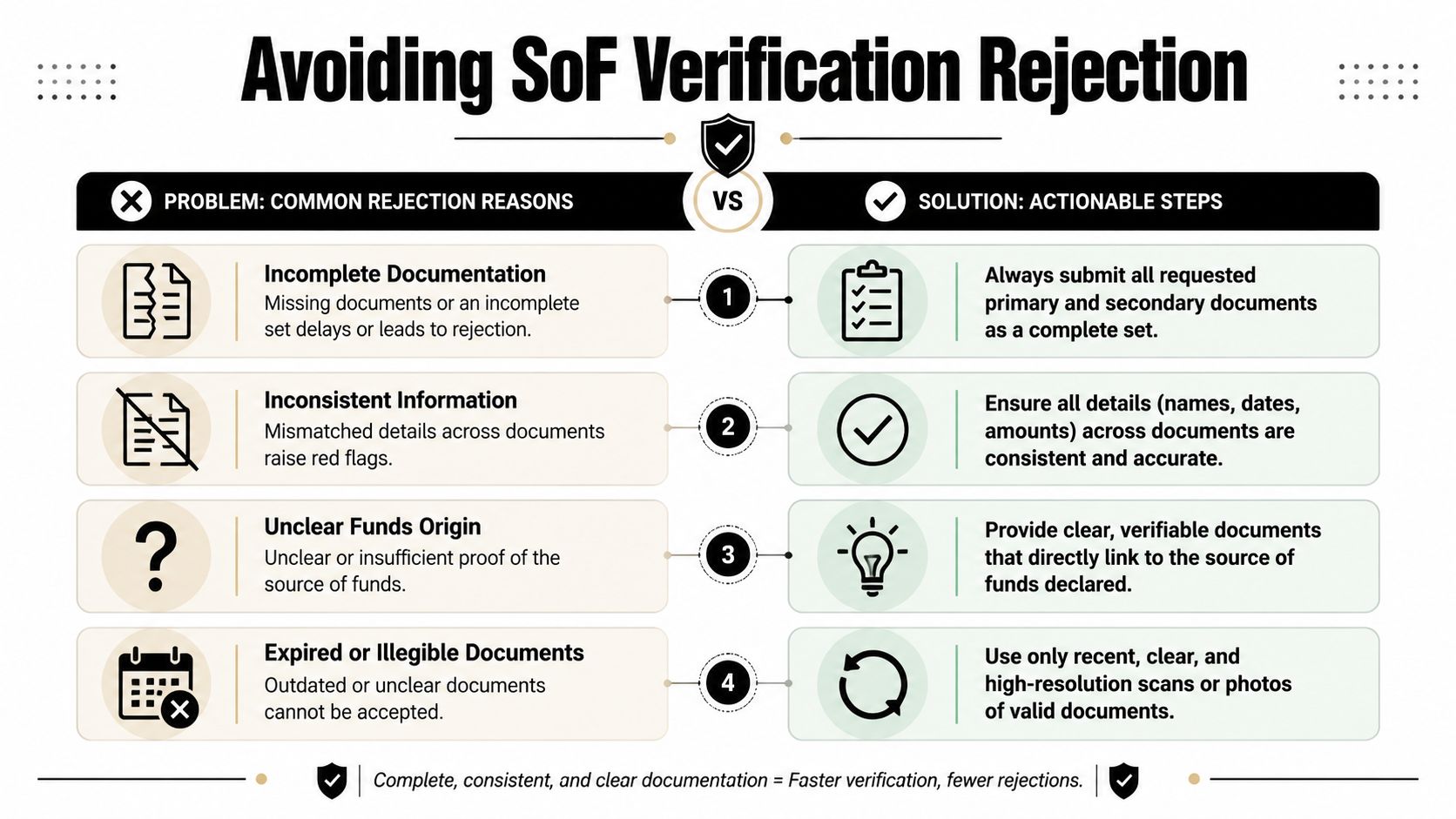

Common Reasons for Rejection and How to Avoid Them

A rejection usually doesn't mean the funds are illegitimate. It usually means the evidence is incomplete, inconsistent, or too hard to follow.

Mismatch between your account and your documents

This is one of the easiest ways to get delayed.

Bad example:

You submit a bank statement from an account in a relative's name, but your trading profile is in your own name.

Good example:

Your statement, ID, and customer profile all match. If a third party is involved, you explain why and provide supporting evidence.

Balance shown, origin missing

A large balance doesn't explain where the money came from.

Bad example:

You upload a statement that shows enough money, but no salary trail, no sale agreement, no exchange history, and no transfer explanation.

Good example:

You provide the statement plus the documents behind the relevant credit or accumulation pattern.

Third-party transfers with no story

This is a major red flag. In higher-risk scenarios involving gifts or large third-party inflows, the evidence needs to explain not just where the money came from, but why it moved through that pathway. Unexplained third-party transfers are a classic laundering concern, so firms often ask for contracts, invoices, donor documentation, and sometimes evidence of the donor's own source of funds, as described in this guide to source of funds verification challenges.

A quick comparison:

| Problem | Weak submission | Strong submission |

|---|---|---|

| Gift | “My father sent it” | Gift letter, donor transfer proof, your receipt evidence |

| Business transfer | Personal statement only | Invoice, business statement, transfer into personal account |

| Third-party payment | No explanation | Counterparty context and full transaction trail |

Poor file quality or over-redaction

Blurry screenshots, cropped PDFs, missing pages, and blacked-out key details create avoidable friction.

Use redactions carefully. Hide irrelevant sensitive details if needed, but don't hide your name, the account identifier, dates, or the transactions that prove the source.

One rule that works: redact for privacy, not for convenience.

Inconsistent narrative

If you say the money came from savings but the statement shows a recent unrelated incoming transfer, the reviewer will stop and ask questions.

Before you upload anything, compare your explanation against your own documents. If they don't tell the same story, rewrite the explanation or add the missing evidence.

Source of Funds Tips for MyFundedCapital Traders

Prop traders run into source of funds verification in slightly different ways than a standard retail banking customer. The friction points tend to be challenge fees, first payout reviews, and crypto-related activity.

Before you pay for a challenge or instant funding

Don't wait until a request arrives. If you're serious about getting funded, prepare your file before you make the payment.

Keep a folder with:

- Your funding source documents: salary, savings, business income, sale proceeds, or crypto records.

- Your account ownership proof: statements that clearly show your name.

- Your transaction path: the actual route from source to the payment method used.

If you're still deciding which route fits your situation, it helps to review how a funded trading account typically works before you start sending documents reactively.

If you paid using crypto

Crypto can be clean and legitimate. It just needs better organization.

Use this checklist:

- Show exchange ownership: account profile or statements that tie the exchange account to you.

- Show asset history: how the crypto was acquired, not just that you currently hold it.

- Show movement: wallet records or exchange withdrawals that line up with the payment.

- Explain conversions: if fiat became crypto or crypto became fiat, include both sides of that movement.

A weak crypto file usually starts too late. It shows only the final wallet balance or only the outgoing transfer. A stronger file starts with the original acquisition and follows the trail forward.

Before your first payout request

The first payout is where many traders discover whether their records are usable.

Have these ready:

| Document set | Why it helps |

|---|---|

| ID and profile consistency | Prevents name and account mismatches |

| Original challenge payment trail | Helps if the payment method itself is reviewed |

| Bank details or crypto payout details | Reduces back-and-forth on ownership and destination |

| Short written explanation | Gives the compliance team context quickly |

If your profile details changed since signup, fix that before requesting payout. Old addresses, mismatched names, and changed wallet usage create avoidable review friction.

For traders funded by family or a business entity

At this stage, many submissions go sideways.

If someone else helped fund your challenge fee or trading-related payment, say that clearly from the start. Don't call it personal savings if the money came from a parent, partner, or company account.

Use a basic structure:

- Who provided the funds

- Why they provided them

- What documents support the transfer

- How the origin of their funds is evidenced if requested

That's more effective than uploading random statements and hoping the reviewer connects the dots.

What actually speeds things up

The traders who get through source of funds verification smoothly usually do four things well:

- They submit a full pack, not one isolated screenshot

- They label files clearly

- They explain unusual flows in one short note

- They avoid mixing personal, business, and third-party funds without documentation

Trading already involves enough operational stress. Don't add compliance chaos because your records live across six apps and two old email accounts.

Protecting Your Privacy and Security

A lot of traders don't mind proving the source. They mind sending sensitive financial documents online. That concern is reasonable.

The right way to think about it is controlled disclosure. A reputable verification flow should use a secure portal, limit who can access submitted documents, and keep review tied to compliance need rather than broad internal visibility. If you want background on how firms think about monitoring and control environments around regulated data, this overview of regulatory compliance SIEM gives helpful security context.

What you can redact and what you shouldn't

You can usually obscure information that has nothing to do with the review. You shouldn't remove the data that makes the document usable.

Usually safe to redact if irrelevant:

- unrelated transactions

- partial account numbers

- unrelated payee details

Usually not safe to redact:

- your name

- your address if it's needed for matching

- statement dates

- the transaction that proves the source of funds

- account ownership indicators

If you're completing a smaller account review and want to understand the kind of identity flow some firms use before or alongside these checks, the 2K account verification steps are a simple example of how structured verification can work.

Basic submission hygiene

Use PDFs when possible. If you're using photos, make sure all corners are visible and text is readable. Don't send documents through random support chats unless the firm specifically instructs you to.

Send the minimum needed to prove the transaction clearly. Not less, and not your entire financial life.

That balance matters. Under-submit and you get delays. Overshare and you create unnecessary privacy exposure.

Frequently Asked Questions About SoF Verification

Do I need to do source of funds verification for every payout

Not always. Many firms focus on onboarding, first payout, unusual activity, or cases where your transaction pattern changes. But policies differ, and ongoing monitoring is part of modern due diligence, so a past approval doesn't guarantee that no future review will happen.

My KYC was approved. Why do you need this too

Because the checks do different jobs.

KYC confirms who you are.

Source of funds verification checks where the money for a specific transaction came from.

You can pass identity verification and still need to explain a payment trail.

What if the money came from a loan or a family gift

That can still be acceptable. The key is documentation.

For a loan, provide the agreement and evidence the money was received.

For a gift, provide a signed declaration or gift letter, transfer proof, and be prepared for the donor's source of funds to matter in some cases.

Is bank transfer better than crypto if I want to avoid checks

Not really. The payment rail doesn't remove the compliance requirement. The main issue is whether the source is understandable and documented.

Bank transfers are often easier to present because people already have statements in familiar format. Crypto can work fine too, but it usually needs more careful recordkeeping to show the full path.

If you want a prop firm setup with clear rules, flexible funding paths, and payout options that fit different trading styles, explore MyFundedCapital. Compare the available programs, check which account type suits your strategy, and start a challenge only when you're comfortable with the rules and the risk. Trading involves risk of loss, and this article is educational only, not financial advice.