You’re looking at the same setup on your screen, but the instrument you choose can change the outcome more than the entry itself. In cfd vs futures, the primary difference is not just definition. It is how margin, holding costs, execution quality, and prop firm risk rules affect whether a good trade stays manageable or turns into a problem.

CFD vs Futures Which Is Right for Your Strategy

A lot of traders ask the wrong first question. They ask whether the market is going up or down. The better question is how to express that view.

If you want to trade gold, indices, FX, or oil, both CFDs and futures can give you exposure. But they behave differently where it matters most.

| Factor | CFDs | Futures |

|---|---|---|

| Market structure | OTC with broker as counterparty | Centralized exchange-traded contract |

| Margin access | Lower margin, higher position capacity | Higher standardized margin requirements |

| Holding costs | Overnight financing can matter | No overnight financing charge |

| Execution | Depends on broker pricing and liquidity | Exchange order book and price discovery |

| Expiry | Usually no fixed expiry on standard CFDs | Contract expiry and rollover required |

| Prop fit | Flexible sizing, but easier to oversize positions | Cleaner execution, but more capital-intensive |

For a prop trader, this choice is not academic.

A lower-margin product can help you spread risk across more ideas. It can also get you to a daily loss limit faster if you trade too large. A cleaner execution product can support scalping and automation better, but contract size, expiry, and margin can reduce flexibility.

Key takeaway: In cfd vs futures, the right answer depends less on preference and more on your holding period, execution needs, and how tightly you manage drawdown.

How CFDs and Futures Contracts Work

Most traders know the labels. Fewer understand the structure underneath. That structure explains most of the trade-offs.

What a CFD really is

A Contract for Difference, or CFD, is a private agreement between you and your broker. You are not buying the underlying asset. You are agreeing to exchange the price difference between entry and exit.

Consider it a side deal with a shopkeeper on the price movement of gold. You do not take the gold home. You settle the difference in value when you close the trade.

That creates a few practical effects:

- No ownership: You are trading price movement, not taking delivery.

- Broker-defined environment: The broker sets the spread, margin terms, and execution framework.

- Flexible access: You can usually trade many markets from one platform with small position sizes.

- No standard expiry in typical retail use: Many CFD products stay open as long as your account supports the margin and you accept any overnight financing.

For active traders, this flexibility is useful. You can size in smaller increments and often access more instruments from one account.

The trade-off is structural. Your pricing and fills depend on broker infrastructure, not a central exchange book.

What a futures contract really is

A futures contract is a standardized agreement traded on a public exchange. It specifies the underlying market, contract size, and expiry month in a fixed format.

This is closer to doing business in a formal auction market. Everyone trades the same contract specifications. Orders interact on the exchange, and a clearinghouse sits in the middle to guarantee performance.

That matters because futures are built around standardization:

- Exchange-listed contracts: Terms are set in advance.

- Central clearing: The exchange framework reduces counterparty uncertainty.

- Visible price discovery: Traders work from the same market structure.

- Expiry dates: Contracts mature, so traders close or roll them forward.

In practice, futures feel more rigid but also more transparent.

If you trade an index future, a commodity future, or an FX future, you are stepping into an institutional market structure. That is why many professional traders prefer futures for execution-sensitive strategies.

Why the structure changes trader behavior

The structural difference changes how traders act.

With CFDs, traders often think in terms of convenience. Smaller capital outlay, easier platform access, simple chart-to-order workflow, broad product list.

With futures, traders think in terms of process. Contract specs, expiry cycles, session behavior, order flow, and tighter control over execution assumptions.

Neither approach is automatically better.

Use CFDs when flexibility, smaller sizing, and broad market access matter more. Use futures when transparent execution and standardized market structure matter more.

A simple way to remember it

If you want the short version, use this:

- CFD: Agreement with your broker on price movement.

- Futures: Standardized contract traded on an exchange.

That one distinction explains most of cfd vs futures. Margin, costs, slippage, and regulation all flow from that starting point.

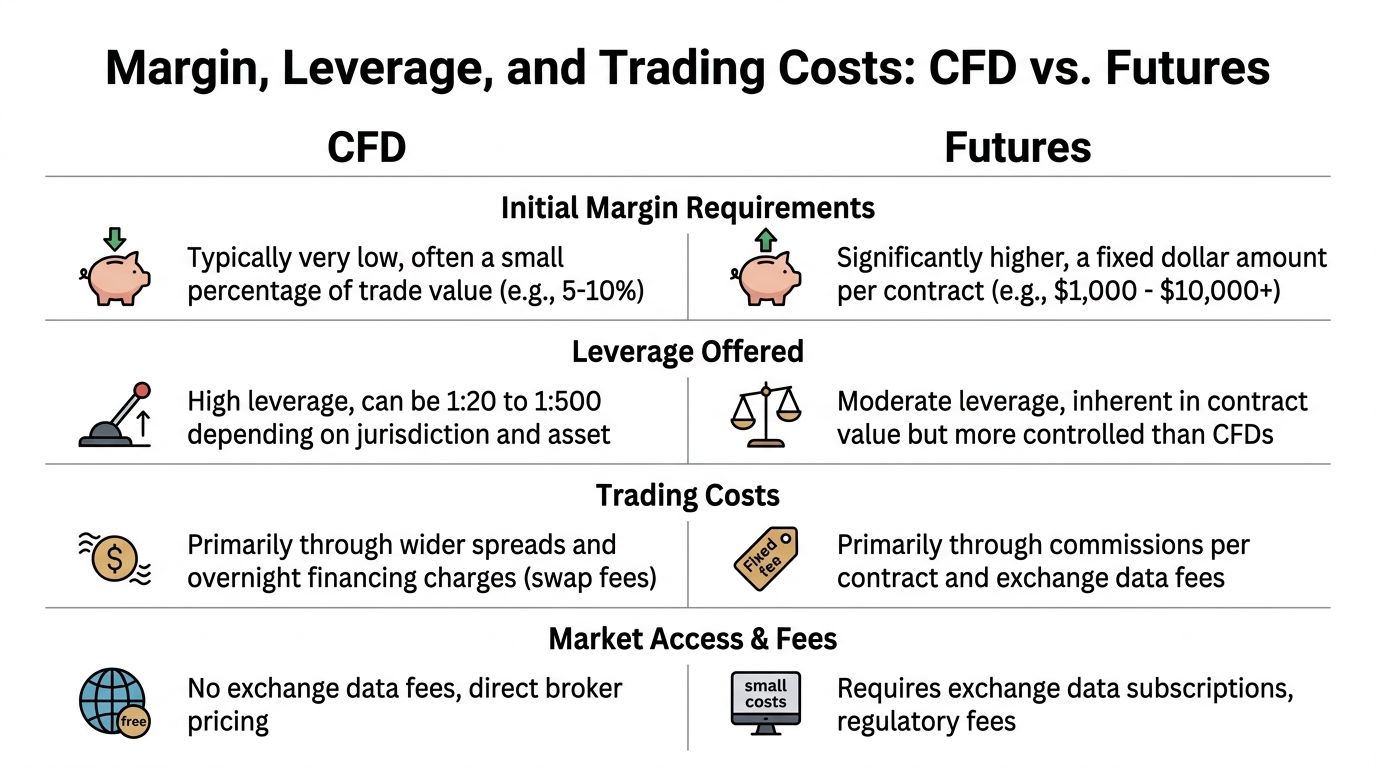

Margin, Position Sizing, and Trading Costs Compared

A trader can call direction correctly and still fail the account because the instrument made risk control harder than it needed to be.

That shows up fast in prop firm trading. Daily drawdown rules, max loss limits, and consistency targets punish sloppy sizing more than bad market reads. The question is not which product gives more exposure. The question is which product lets you express the trade without creating unnecessary damage when it goes wrong.

Margin access changes behavior before it changes returns

CFDs usually let traders control a position with far less cash posted upfront. Earlier data from VT Markets illustrated that gap clearly with examples in gold and single-stock exposure.

The practical takeaway is simple. Lower margin makes entry easier, but it also makes oversizing easier. I see newer traders confuse cheap access with controlled risk all the time. Those are not the same thing.

Futures are less forgiving on this point. The contract size and exchange margin framework force a sizing decision that is harder to ignore. That can feel restrictive in a small account, but in a prop setting it often works in your favor because it prevents casual overexposure.

For prop firm traders, this matters more than the usual retail discussion about "capital efficiency." If one futures contract risks too much relative to your daily loss limit, the setup may be valid and still be untradeable. If a CFD lets you scale down more precisely, you may be able to keep the same idea inside the firm's risk rules.

If you need a cleaner understanding of how margin works before comparing products, this guide on trade margin definition is worth reviewing.

Position sizing reveals significant differences

The biggest day-to-day advantage of CFDs is granularity. You can usually trim size in smaller increments, which helps if you risk a fixed percentage per trade or need to scale around tight drawdown limits.

Futures give you standardization, but standardization creates lumpiness. If the contract is too large for your account, you do not have many ways to fix that. You either trade the micros, reduce trade frequency, widen the stop and cut size elsewhere, or skip the setup.

That is why instrument choice should start with risk math, not preference. Traders who work in firms with a hard daily drawdown cap should calculate worst-case loss per position first, then choose the product. If you are still refining that math, learning how tick value affects risk per contract will make these sizing decisions much cleaner.

Trading costs depend on how long you hold

Costs hit differently depending on the strategy.

For CFDs, the visible cost is usually the spread. The less visible cost is financing if you hold overnight. Intraday traders may not feel that charge much. Swing traders do.

For futures, the cost profile is usually cleaner for overnight holding, but you still have to account for commissions, exchange fees, and potential roll costs if you stay in the trade long enough. Nothing is free. The difference is that futures costs are often easier to model in advance, while CFD carrying costs can distort a strategy that looked profitable on entry.

This matters in prop accounts because a good trade plan can still underperform if carrying costs chip away at open equity or net profit. If your firm measures trailing drawdown off balance or equity, those details stop being theoretical.

What tends to work better in practice

CFDs fit better when:

- You need precise size control: Small increments help keep each trade inside strict loss limits.

- You trade intraday: Closing before rollover avoids one of the main CFD cost problems.

- Your account size is too small for the futures contract you want: The idea may still be tradable with a smaller CFD position.

Futures fit better when:

- You hold overnight or over several sessions: Financing is less likely to erode the trade.

- You want a cleaner fixed-cost framework: Commissions and fees are easier to map out before entry.

- You trade a liquid market with a contract size that matches your account: The structure becomes an advantage instead of a constraint.

The mismatch is what hurts traders.

A swing trader who ignores CFD financing can watch a decent setup lose efficiency trade by trade. A prop trader who uses the easy sizing of CFDs to press too hard can breach the daily drawdown limit in a single sloppy sequence. A futures trader can have the opposite problem. The setup is fine, but the minimum contract size makes the risk too chunky for the account.

A practical checklist before you choose the instrument

Ask these questions before placing the order:

Will I hold this past the session close?

If yes, carrying costs need to be in the plan.How much can I lose before I hit the firm's daily drawdown threshold?

That number should determine size, not conviction.Do I need to scale in or out in small increments?

CFDs often handle that better.Does one futures contract make the trade too large for my stop distance?

If yes, use a smaller contract, switch products, or pass.Is the expected edge wide enough to absorb spread, fees, and financing?

Small-edge strategies get punished first by bad cost selection.

Practical rule: Choose the product that lets you survive normal variance without violating your risk rules. In a prop environment, the better instrument is often the one that makes it harder to do something stupid.

Execution Quality Slippage and Market Access

A lot of traders blame themselves for bad fills that were largely structural. Sometimes the issue is not your timing. It is the market you chose.

Futures execution is built around transparency

Futures trade on centralized exchanges such as CME and NYMEX. According to QuantVPS, major contracts like ES, NQ, and CL attract substantial institutional volume, with transparent order books, tight bid-ask spreads, and consistent matching. The same source notes that this creates more predictable execution and negligible slippage for algo scalping strategies in the right conditions (QuantVPS on futures vs CFD trading).

For a manual trader, that means cleaner fills.

For an algo trader, it matters even more. If your system expects a certain spread and fill logic, exchange structure gives you a more stable environment than broker-dependent OTC pricing.

CFD execution depends on the broker

CFDs are over-the-counter products. Your broker is part of the execution chain, not just a neutral pipe.

That creates practical variation:

- Pricing can differ across brokers

- Spreads can widen sharply in fast markets

- Slippage may increase around news

- Order fills depend on broker-side liquidity setup

None of that means CFDs are unusable. It means broker selection matters a lot more.

A liquid index CFD with a strong broker can trade well enough for many discretionary traders. But if you are scalping around releases, running an EA, or measuring edge in very small increments, broker-side variation becomes harder to ignore.

For traders studying short-term market movement, understanding trading the tick helps. Execution quality matters most when your trade logic depends on small price changes.

Market access is broader on CFDs

In this area, CFDs often win.

If you want a broad menu of global markets from one retail platform, CFDs are usually easier. You can access forex, indices, commodities, crypto, and often a longer list of single-name products without learning separate contract specifications.

Futures are more concentrated around core institutional markets. That is not a weakness if those are the products you trade. It is a limitation if your strategy depends on niche names or broad platform convenience.

Which traders feel the difference most

Execution differences matter most for:

- Scalpers: A small change in spread or fill quality can erase the trade.

- Algo and EA traders: Strategy assumptions break faster when fills become inconsistent.

- News traders: Volatility exposes the gap between exchange order flow and broker-managed pricing.

Discretionary intraday traders feel it too, just less mechanically.

Tip: If your review process shows repeated stop-outs, slippage spikes, or missed fills around volatile periods, test whether the problem is your execution venue before rewriting the strategy.

CFD vs Futures in a Prop Firm Environment

A prop environment changes the cfd vs futures decision because the account is not judged only on profit. It is judged on rule compliance.

The most common mistake I see is traders choosing an instrument for convenience, then discovering that the product clashes with drawdown rules, session rules, or their own execution habits.

High position sizing capacity helps until it hurts

In a funded setup with a flat 5% daily loss limit and up to 10% maximum drawdown, position sizing capacity is never just an opportunity. It is a drawdown accelerator if used carelessly.

CFDs can help a trader stay active with lower margin usage. That is useful when you want flexibility, smaller sizing increments, or multiple trade ideas across markets.

But the same flexibility creates a trap. Because the margin requirement is light, many traders size based on what the platform allows instead of what the risk model allows.

That behavior does not last long in a prop account.

Futures push back in the other direction. The margin is heavier and the structure is more rigid, which often stops impulsive oversizing. The downside is that some traders end up taking fewer but larger exposures because contract sizing gives them less flexibility.

The holding period matters more in funded trading

Prop traders often obsess over payout timing but ignore holding cost and instrument behavior.

If your style is intraday and flat by the end of the session, CFDs can be a workable fit. If your style relies on holding positions longer, the issue shifts toward cost drag, contract management, and event exposure.

You also need to think about operational details:

- CFDs: Usually simpler for continuous exposure, since standard retail contracts do not force a traditional expiry cycle.

- Futures: You need to track expiry and roll when necessary.

- Weekend and news rules: Product structure interacts with these account permissions in different ways.

A trader holding through volatile periods may find futures cleaner from an execution and pricing standpoint. Another trader may prefer the convenience of CFDs if the strategy depends on flexible retail access and smaller sizing.

Which instrument fits which prop trader

Use CFDs if most of these describe you:

- You trade intraday.

- You need smaller and more adjustable position sizes.

- You trade several asset classes from one platform.

- You can stay disciplined with position sizing even when margin access is easy.

Use futures if most of these describe you:

- You care significantly about execution quality.

- Your strategy depends on repeatable fills.

- You trade core markets like index, commodity, or FX futures.

- You are comfortable managing contract rollover and standardized specs.

For traders specifically exploring futures evaluations and how funded futures setups work, futures prop trading is worth reviewing as part of the selection process.

What tends to fail in prop accounts

A few patterns show up repeatedly:

CFD traders using margin capacity as their sole sizing guide

The account survives until one volatile session breaks the daily limit.Futures traders ignoring contract mechanics

They understand the chart but not the product details.News traders assuming all instruments react the same way

They do not. Broker spread widening and exchange-driven movement are different problems.Algo traders optimizing entries without testing live fill conditions

Backtests can look clean while execution reality is messy.

There is also one broader operational point. Some firms support manual and automated strategies across platforms like cTrader and DXtrade. MyFundedCapital is one example, offering simulated funded trading across multiple instruments and account formats under published risk parameters. That matters if your instrument choice is tied to platform workflow rather than theory alone.

Navigating Regulation and Tax Differences

Most traders spend too much time comparing position sizing and not enough time checking whether the product even fits their legal and tax reality.

That is a mistake. Net returns are what matter.

Regulation changes access and protections

Futures trade on regulated exchanges with standardized contract terms. CFDs are OTC products, and the rules around them vary by country.

In practical terms, that means traders in different regions do not face the same choices. Some can access both products. Others mainly trade one.

This affects more than availability. It affects what kind of platform environment, broker framework, and product protections you are dealing with.

Tax treatment is highly jurisdiction-specific

The tax side is less discussed and often more important than traders expect.

The verified guidance here is narrow but useful. The available comparison notes that tax treatment for CFDs depends heavily on jurisdiction and structure, while futures treatment is often more standardized. It also highlights that traders in the UK, EU, Australia, and Singapore may face very different outcomes, that EU traders holding CFDs may benefit from capital gains treatment rather than income tax, and that US-based futures traders often face Section 1256 “60/40” treatment (Shares on CFD vs futures tax differences).

That same source points out a gap many traders ignore. It does not clearly address how prop firm profit splits such as 80/20, 90/10, and 100% interact with local tax treatment, or how evaluation-stage demo trading relates to tax once profits are paid out.

Those are not minor details. They affect what you keep.

What to do before you choose an instrument

Use a short checklist:

- Confirm availability in your jurisdiction

- Ask how trading profits are classified locally

- Check whether funded payouts are treated differently from self-directed trading gains

- Get advice from a local tax professional before scaling

If you trade from Australia, a practical primer on Capital Gains Tax on Investments gives useful background before you speak to an accountant.

Important: This article is educational only and not financial or tax advice. Trading involves risk of loss, and tax treatment depends on your jurisdiction, structure, and personal circumstances.

A Decision Framework Which Instrument to Trade and When

A prop trader passes an evaluation with clean intraday discipline, then gives back a week of progress by using the wrong instrument for the next phase. The setup was fine. The mismatch came from holding time, sizing constraints, and how the product behaved against the firm’s drawdown rules.

Instrument choice is a risk management decision first. Strategy fit comes right behind it.

Start with the holding period

Short holding periods give CFDs a fair case. If the plan is to open, manage, and close within the session, the product can do the job well enough, especially when flexible sizing matters.

Longer holding periods shift the balance. As noted earlier, overnight financing can eat into CFD returns while futures pricing handles carry differently. For a prop trader, that matters twice. It affects net expectancy, and it can force a good trade to spend longer near your daily loss limit before the move pays.

That second point gets missed a lot. In a personal account, you may tolerate some carry drag if the thesis is intact. In a prop account with a hard daily drawdown, extra cost and slower payoff can turn a valid swing idea into a rule breach.

Next, measure how much execution quality matters to your edge

If your average win is modest and your stop is tight, small fill differences matter. They matter a lot.

Choose futures more often if your setup depends on:

- Scalping a few points or ticks

- Fast entries around news or momentum bursts

- Automation or semi-systematic execution

- Consistent order book behavior

- Cleaner slippage tracking in review

Choose CFDs more often if your setup depends on:

- Discretionary entries with wider tolerance

- Fractional sizing precision

- Simple access through a familiar retail platform

- Intraday trading where you can avoid rollover

This is the practical test I use. If a trade idea still works after slightly worse execution, CFDs may be acceptable. If one poor fill changes the trade from positive to mediocre, futures usually fit better.

Then match the product to the account rules

Prop firm traders require a different framework than standard retail traders.

A $100,000 evaluation account does not give you the same freedom as a personal account with the same nominal size. Daily drawdown, trailing max loss, consistency rules, and payout conditions all change what “efficient” trading looks like. An instrument that offers more exposure can still be the wrong choice if it makes it easier to violate firm rules.

Use CFDs when

You need fine control over position size.

You are trading short-duration setups and expect to be flat before rollover.

You know the broker’s execution is good enough for your style.

Your main challenge is sizing precisely around a fixed daily loss limit.

Use futures when

You need a more standardized trading environment.

You expect to hold beyond the session.

Your strategy is sensitive to fill quality.

You want trade review to reflect market behavior more than broker-specific pricing.

Avoid both when

You have not defined invalidation before entry.

You are selecting the product based on buying power instead of dollar risk.

You cannot explain how the trade fits the prop firm’s daily drawdown and max loss rules.

That last point matters more than traders admit. I have seen juniors choose CFDs because the small contract increments felt safer, then overtrade because the account looked easy to scale. I have also seen traders pick futures for the cleaner market structure, then force setups in products that were too large for their stop and daily limit. In both cases, the instrument was not the problem. Position sizing discipline was.

A practical decision matrix

| Situation | Better fit |

|---|---|

| Intraday discretionary trading with small flexible sizing | CFDs |

| Multi-session trade where holding cost can affect expectancy | Futures |

| Execution-sensitive scalping or automation | Futures |

| Platform-driven retail workflow with broad product access | CFDs |

| Trader with a history of oversizing under loose margin conditions | Usually futures |

The right question is not which product is better. The right question is which product gives your strategy room to perform without putting you in constant conflict with the account rules.

Frequently Asked Questions About CFDs and Futures

Which is better for scalping

Usually, futures.

The exchange-traded structure, transparent order book, and more consistent fills make futures a better fit for strategies that depend on tight execution. CFDs can still work for scalping if your broker is strong and the market is liquid, but the margin for error is smaller.

What happens when a futures contract expires

You usually do not hold it into expiry as a retail trader.

Most traders close the position before expiry or roll into the next contract month if they want to keep exposure. That requires a bit more operational awareness than standard CFD trading.

Are CFDs or futures more profitable

Neither instrument is more profitable by nature.

Profit comes from the quality of your process, your risk control, and whether the product matches your strategy. A good setup traded in the wrong instrument can underperform because of financing, slippage, or sizing problems.

Which is better for a funded trader

It depends on how you trade.

If you are intraday, need flexible sizing, and can stay disciplined with position sizing, CFDs may fit. If you need consistent execution, hold longer, or run systematic strategies, futures often fit better.

Trading involves risk of loss. This article is educational only and not financial advice.

If you want to put this framework into practice, review the account options at MyFundedCapital and compare which setup fits your strategy, platform preference, and risk discipline before starting a challenge or funding program.