Volatility is where a lot of traders get trapped. They either chase panic, short premium at the wrong time, or treat the VIX like a magic signal without understanding what it measures.

If you want to learn how to trade volatility inside a prop firm account, you need more than strategy names. You need a process that fits drawdown rules, handles news risk, and stays repeatable when markets stop behaving cleanly.

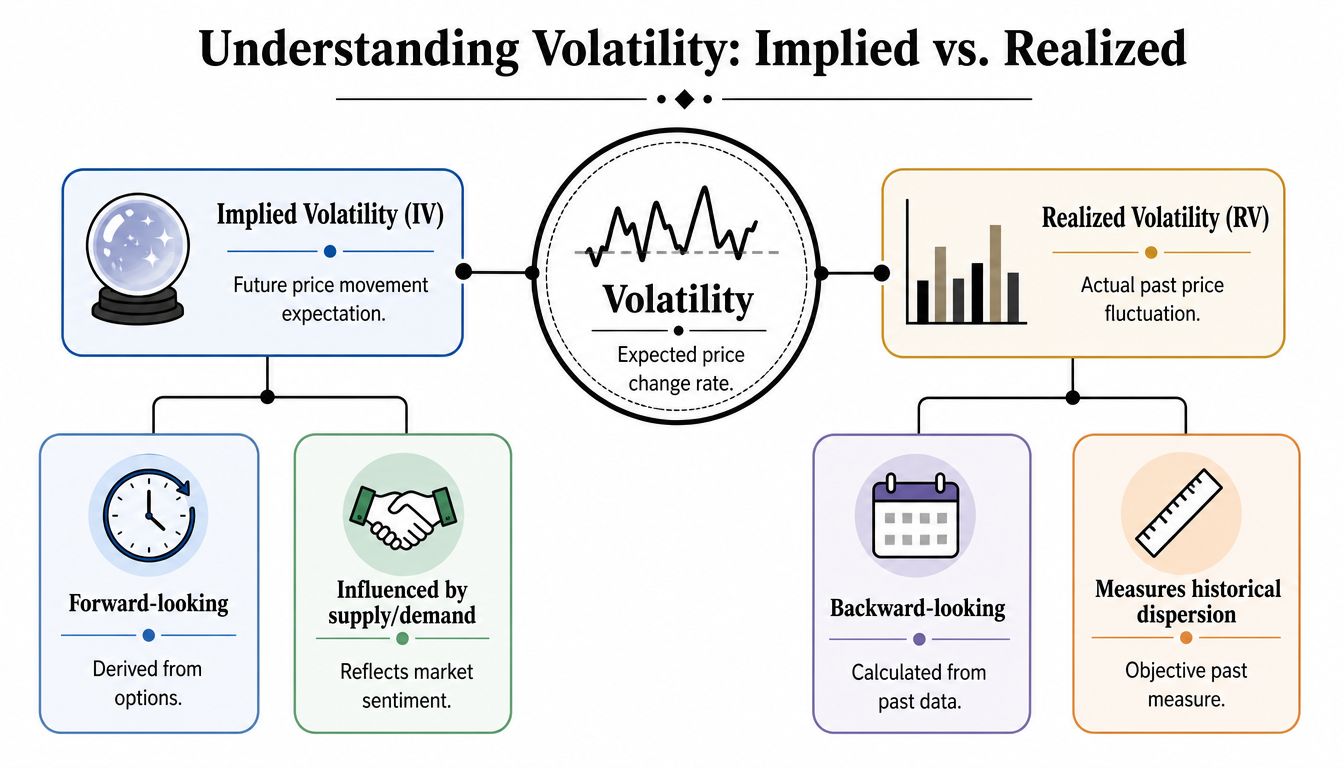

Understanding the Two Faces of Volatility

Most traders start with the wrong question. They ask whether volatility is high or low. The better question is what kind of volatility you're looking at.

At the desk level, volatility has two faces:

- Implied volatility

- Realized volatility

That distinction matters because one is about expectation, and the other is about what already happened.

Implied volatility is the market's forecast

Implied volatility (IV) comes from option prices. It reflects how much movement traders expect going forward. If traders are nervous about a central bank decision, CPI release, or earnings report, IV usually rises before the event because people bid up protection and speculative exposure.

A useful professional framing comes from Dr. Euan Sinclair. He notes that volatility traders often work by solving the Black-Scholes equation backward to derive implied volatility from the option price, then comparing that to a forecast from a time-series model. If there's a discrepancy, the option can be traded to capture it, as described in Nasdaq's introduction to trading volatility.

That isn't just theory. It's the basis for a lot of practical vol trading. You're constantly comparing what options imply with what you think will happen.

Realized volatility is the tape after the fact

Realized volatility (RV) is backward-looking. It measures the actual dispersion of price movement over a past period.

If a market chops around with limited movement for days and then suddenly expands, RV catches that only after the move has occurred. IV, by contrast, may have moved before the event if traders anticipated the shock.

A simple way to think about it:

| Measure | What it tells you | Where it comes from |

|---|---|---|

| Implied volatility | What traders expect next | Option prices |

| Realized volatility | What the market already did | Historical price data |

For a solid primer on the mechanics, MFC's guide on what volatility means in trading is a useful reference for historical volatility, implied volatility, ATR, and VIX in one place.

Practical rule: If you don't know whether you're trading expected movement or actual movement, you don't have a volatility strategy yet.

Where the opportunity usually sits

The trade often comes from the gap between expectation and reality. Before a major scheduled event, IV can get inflated because traders pay up for optionality. After the event, that pricing can collapse even if price itself still moves.

That's why many beginners buy options because “something big is coming,” then lose money when the event passes and implied volatility drops faster than the underlying moves in their favor. They were right on attention, wrong on structure.

This is also why volatility trading isn't automatically neutral. Event pricing can carry directional risk, skew risk, and timing risk at the same time.

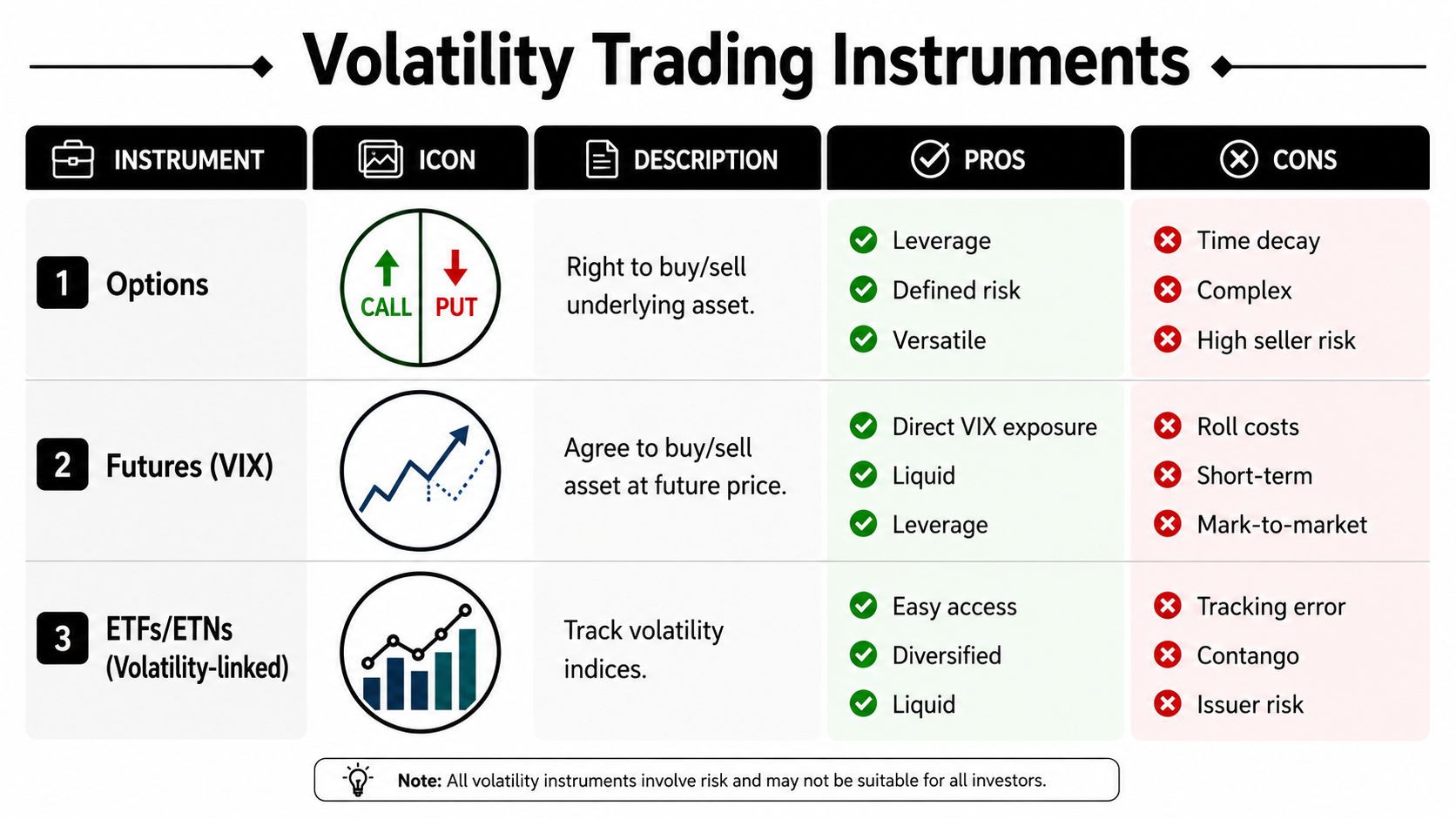

Your Toolkit for Trading Volatility

You don't trade volatility with one instrument. You choose the tool that matches the job, your account rules, and your ability to manage the position.

A trader trying to catch a short-term panic move shouldn't use the same structure as someone fading high volatility over several sessions. The instrument changes the risk profile.

Options are the most flexible tool

For most beginner-to-intermediate traders, stock and index options are the cleanest way to express a volatility view.

They let you shape exposure with:

- Long premium trades when you expect expansion

- Short premium trades when you expect contraction

- Defined-risk spreads when you need tighter downside control

- Delta-neutral structures when you want to isolate volatility more than direction

Pros

- Defined risk when you buy options or use debit spreads

- Flexible structures for directional and non-directional views

- Direct access to Greeks like vega and gamma

Cons

- Time decay works against long premium

- Short premium can get ugly fast during sharp moves

- Good execution requires understanding IV, RV, and term structure

VIX futures and VIX options are more direct, but less forgiving

If you want cleaner exposure to volatility itself, VIX futures and VIX options are the specialist instruments. They're designed for trading volatility, not just price direction in an index.

They're useful, but they're not beginner-friendly. You need to understand futures behavior, term structure, roll effects, and how VIX products can move differently from what newer traders expect.

VIX products often look simpler than they are. The chart is easy to see. The structure behind it isn't.

These instruments suit traders who already know how volatility indexes behave around stress, decay, and reversion.

Volatility ETPs are accessible, but they come with baggage

Volatility exchange-traded products give retail traders easier access than futures. The verified data specifically notes that some traders use VTEPs that track the VIX directly as a simpler route than options or futures.

That's practical, but it comes with trade-offs:

- Accessibility: Easier than futures for many traders

- Complexity: Lower than options portfolios, but still not simple

- Risk: Tracking issues and term-structure effects can distort the trade

They're useful when you want exposure without building a complex options book, but they aren't a shortcut around risk.

CFDs and FX can express volatility indirectly

Some prop traders don't trade listed options at all. They use FX, indices, commodities, or CFDs and build volatility-based setups around ATR expansion, breakout conditions, or contraction-to-expansion patterns.

That isn't “pure vol trading,” but it is often the most practical route inside funded account rules. If your platform supports broad market access rather than a full options chain, volatility still shows up through price behavior, range expansion, and regime change.

Here's a simple comparison:

| Instrument | Best for | Main weakness |

|---|---|---|

| Options | Flexible volatility views | Complexity and time decay |

| VIX futures/options | Direct vol exposure | Advanced structure risk |

| Volatility ETPs | Simpler market access | Tracking and term-structure issues |

| CFDs/FX/index products | Prop-friendly execution | Indirect exposure to volatility |

The right tool is the one you can size correctly, understand fully, and exit cleanly.

Actionable Volatility Strategy Templates

Most traders don't need more theory. They need setups they can test, reject, refine, or keep.

Below are four templates that cover expansion, contraction, and mean reversion. Each has a place. Each can also blow up if you force it into the wrong market.

Long straddle or long strangle

This is the classic long volatility trade. You use it when you expect a large move but don't have strong conviction on direction.

When to use it

- Scheduled event risk

- Compression before a breakout

- A market that's been coiling and looks ready to expand

How to set it up

- A straddle buys a call and put at the same strike

- A strangle buys a call and put at different strikes, usually cheaper but requiring a larger move

The logic is simple. You need realized movement to outrun the premium paid.

What to watch out for

- If implied volatility is already inflated, you can still lose even on a decent move

- Time decay accelerates if price stalls

- Traders often overpay for “certainty” just before the event

This works best when the market is underpricing the coming move, not when everyone already knows chaos is coming.

Iron condor for quiet conditions

The iron condor is a short-volatility structure for range-bound markets. You're selling premium while defining the risk on both sides.

When to use it

- Range-bound index conditions

- No obvious catalyst directly ahead

- IV high enough to justify premium sale, but without signs of imminent expansion

How to set it up

You sell an out-of-the-money call spread and an out-of-the-money put spread. The goal is for price to stay inside the range through expiration.

What to watch out for

- Sharp trend days can break the structure quickly

- Gamma risk grows as expiration approaches

- A “safe” condor often becomes dangerous when traders oversize it

Short volatility looks easy until the range breaks. Then the adjustment decisions get emotional fast.

Mean reversion using VIX extremes

The most systematic retail-friendly volatility template in the verified data is mean reversion around the VIX.

The core premise is that volatility tends to revert toward its long-run average. The verified data states that the VIX has historically averaged approximately 19.5% over the long term, while it can spike to over 80% during crisis periods like March 2020, then revert within months. It also notes that when the VIX rises above 40, historical data shows a 75% probability of declining within 10 trading days, and when the VIX falls below 12, there is a 70% probability of rising within 30 days. Those details come from the verified dataset provided for this article.

A practical version uses:

- Bollinger Bands to locate extreme deviation

- ATR to gauge whether the move has enough force

- A stop-loss at 1.5 times the ATR to control false reversions

- A target of exactly two times the initial risk

- A 10-period moving average for trend confirmation

- A consolidation of at least three sideways bars before breakout entry

- A 20-period moving average as a trailing exit

Execution note: Mean reversion works when volatility is stretched, not simply “high.” If the tape is still expanding and structure hasn't stabilized, fading it early can turn a clean setup into a rule violation.

This is one of the better bridges between classic volatility theory and practical prop trading because it gives you objective triggers instead of gut feel.

Calendar spreads for term structure trades

A calendar spread trades volatility across time rather than pure direction. The verified data describes the structure as selling a near-term option and buying a longer-dated option at the same strike, aiming to profit when near-term implied volatility is higher than long-term implied volatility, particularly in contango conditions, as outlined in TradeStation's discussion of options strategies for volatility spikes.

This is useful when you think front-end fear is overpriced relative to later expiries.

Use it when

- Near-term event premium looks inflated

- You expect volatility to normalize after the event

- You want a more nuanced view than buying or selling premium outright

Watch the risk

- Term structure can shift against you

- Direction still matters more than many traders realize

- Calendar spreads can become harder to manage if the underlying starts trending hard

If you're interested in trading volatility professionally, it's worth looking at how job descriptions frame the skill set. A DeFi quant trader position gives a good sense of how firms think about systematic risk, derivatives logic, and execution discipline.

For a more retail-facing breakdown of options-specific volatility structures, MFC also has a practical guide to volatility trading with options.

Airtight Risk Controls for Volatility Trading

A volatility trader who doesn't think like a risk manager usually doesn't last. This is even more obvious in prop trading, where one bad decision can end the account before the good setups have time to matter.

The dangerous part is that short volatility often feels safe right before it isn't. Premium comes in, price seems contained, and the position looks under control. Then the market reprices faster than your structure can absorb it.

Why drawdown kills more traders than bad entries

The verified data makes the warning plain. Mean-reversion tactics thrive when VIX is above 25, yet 78% of retail traders lose money on short-vol strategies because they ignore directional risk, a problem that matters even more with a 5% daily loss limit in a prop environment, as noted in this discussion of volatility trading.

That failure usually isn't about signal quality alone. It's about traders assuming volatility is a neutral product when the market is still moving directionally with force.

Non-negotiable controls

Use controls that fit the structure you're trading:

- Defined risk first: Spreads are usually easier to govern than naked short premium.

- Volatility-based stops: The verified methodology above uses 1.5 times ATR as a stop framework for false mean-reversion attempts. That's a market-based stop, not an emotional one.

- Smaller size in unstable regimes: If volatility is expanding, size must usually shrink.

- Event filters: If your setup relies on contraction, don't hold it blindly into a major catalyst.

- Hard invalidation points: Know exactly where the thesis fails before entry.

A funded trader doesn't get paid for being brave during a volatility shock. They get paid for staying inside the risk box long enough to exploit the next clean setup.

The risk most traders underestimate

Gamma risk is the trap in many short options trades. When the underlying starts moving hard, the position can become more directional than planned, and the P&L can accelerate against you.

That's why “I'll manage it if it gets close” is not a plan. In fast markets, the adjustment window can disappear. If your position structure can breach your daily limit during a single disorderly move, the structure is too large or too loose for a prop account.

Backtesting and Executing Your Trades

A volatility setup isn't real until you've tested it. Chart screenshots and one good week don't count.

For a prop trader, backtesting has one main purpose. It tells you whether the strategy can survive the bad stretches without blowing through your allowed drawdown. MFC's guide on what backtesting is and how traders use it is a useful starting point if your process is still manual.

A simple testing workflow

Start with one idea, not five. For example, test a VIX mean-reversion setup only after your trigger conditions are fully defined.

A clean workflow looks like this:

Define the signal clearly

Write the exact entry conditions. No vague language like “looks extreme.”Define the exit before testing

Use the same stop and target logic every time in the first pass.Track more than win rate

Focus on:- Maximum drawdown

- Profit factor

- Sharpe ratio

- Equity curve stability

Segment the results

Separate calm regimes from panic regimes. Volatility strategies often behave very differently across those environments.

What matters in live execution

Good backtests still fail in live trading when execution gets sloppy.

Use a checklist before every trade:

- Is the setup valid right now

- Is there scheduled news that changes the profile

- Does the position size fit the account's rules

- Is the stop placed where the thesis fails

- Do I know what I'll do if volatility expands immediately instead of reverting

Your strategy should survive bad execution days. If it only works when you trade perfectly, it isn't robust enough for a funded account.

Execution discipline matters more in volatility than many traders expect because the market often moves fastest when your emotions are least useful.

Trading Volatility within Prop Firm Rules

Volatility trading changes when the account has hard guardrails. In a personal account, a trader can absorb more noise, average badly, or hold through a rough day. In a funded account, those habits become disqualifying.

That's why the first filter isn't “What setup do I like?” It's “What setup fits the rule set?”

Match the strategy to the rule book

The publisher profile for this article states that MyFundedCapital accounts use a flat 5% daily loss limit and up to 10% maximum drawdown. Those constraints matter a lot for volatility trading.

Some clear adaptations follow from that:

- Defined-risk structures fit better than undefined-risk short premium

- Short holding periods reduce overnight uncertainty

- News-sensitive trades need rule awareness before entry

- Scaling should follow consistency, not excitement after one big vol day

A long straddle may be expensive, but its maximum loss is known. A naked short straddle can become impossible to defend if volatility expands and price trends at the same time. In a prop environment, that difference isn't academic.

Use the constraints to your advantage

Good prop traders don't treat rules as a burden. They use them to eliminate low-quality decisions.

For volatility trading, that usually means:

| Situation | Better fit inside prop rules |

|---|---|

| Expecting expansion | Long premium or defined-risk breakout structure |

| Expecting contraction | Smaller, defined-risk premium-selling structure |

| Fading panic | Rule-based mean reversion with hard ATR stop |

| Unsure about event impact | Stand aside |

If your firm allows add-ons for news trading or weekend holding, those features can expand what you can do with volatility setups. If the account doesn't allow that exposure, don't try to force an event strategy into a rule set that punishes it.

Capital scaling also changes the mindset. The goal isn't to hit one giant volatility trade. The goal is to prove that your process handles stress cleanly enough to justify more size later.

Frequently Asked Questions About Volatility Trading

Is volatility trading only for options traders

No. Options are the clearest direct tool, but traders can also approach volatility through VIX-linked products, index products, FX, CFDs, and rule-based breakout or mean-reversion systems built around ATR and price expansion.

The key is understanding what you're expressing. Some products give direct volatility exposure. Others only reflect it indirectly.

Is short volatility easier than long volatility

It often feels easier because premium decay can make the P&L look smoother for a while. That smoothness fools people.

The verified data notes that traders seeking negative Vega, which profits from a drop in high volatility, often use strategies that sell volatility and benefit from premium decay, and that this works best when entered before a volatility spike with tail risk management, as discussed in this explanation of negative Vega exposure. The hidden problem is that one sharp move can erase many smaller gains.

Can beginners learn how to trade volatility safely

Yes, but “safely” means starting with structures that have defined risk and clear invalidation points. It doesn't mean volatility becomes harmless.

A beginner usually has a better chance with one tested setup, small size, and strict stop logic than with a toolbox full of advanced strategies they can't yet manage.

What is the biggest mistake in volatility trading

Confusing a market that is stretched with a market that has stopped expanding. Traders fade high volatility too early, sell premium into directional momentum, or ignore how quickly drawdown can compound when volatility and direction move together.

If you want to apply these ideas in a structured environment, explore MyFundedCapital to compare funding programs, account types, and challenge models that fit your style. Trading involves risk of loss, and this article is educational only, not financial advice.