Most advice on how to trade with algorithms starts in the wrong place. It starts with coding, or worse, with buying a bot and hoping it passes a prop challenge. The essential work starts earlier and ends later: idea quality, data quality, validation, execution, and risk controls all matter more than clever code.

If you're trying to build an algo that can survive a prop firm evaluation, you need a process that treats the strategy and the operating environment as one system. That means rules for entries and exits, but also slippage assumptions, daily loss controls, platform reliability, and a deployment setup that won't fall apart mid-session. Trading involves risk of loss. This is educational only, not financial advice.

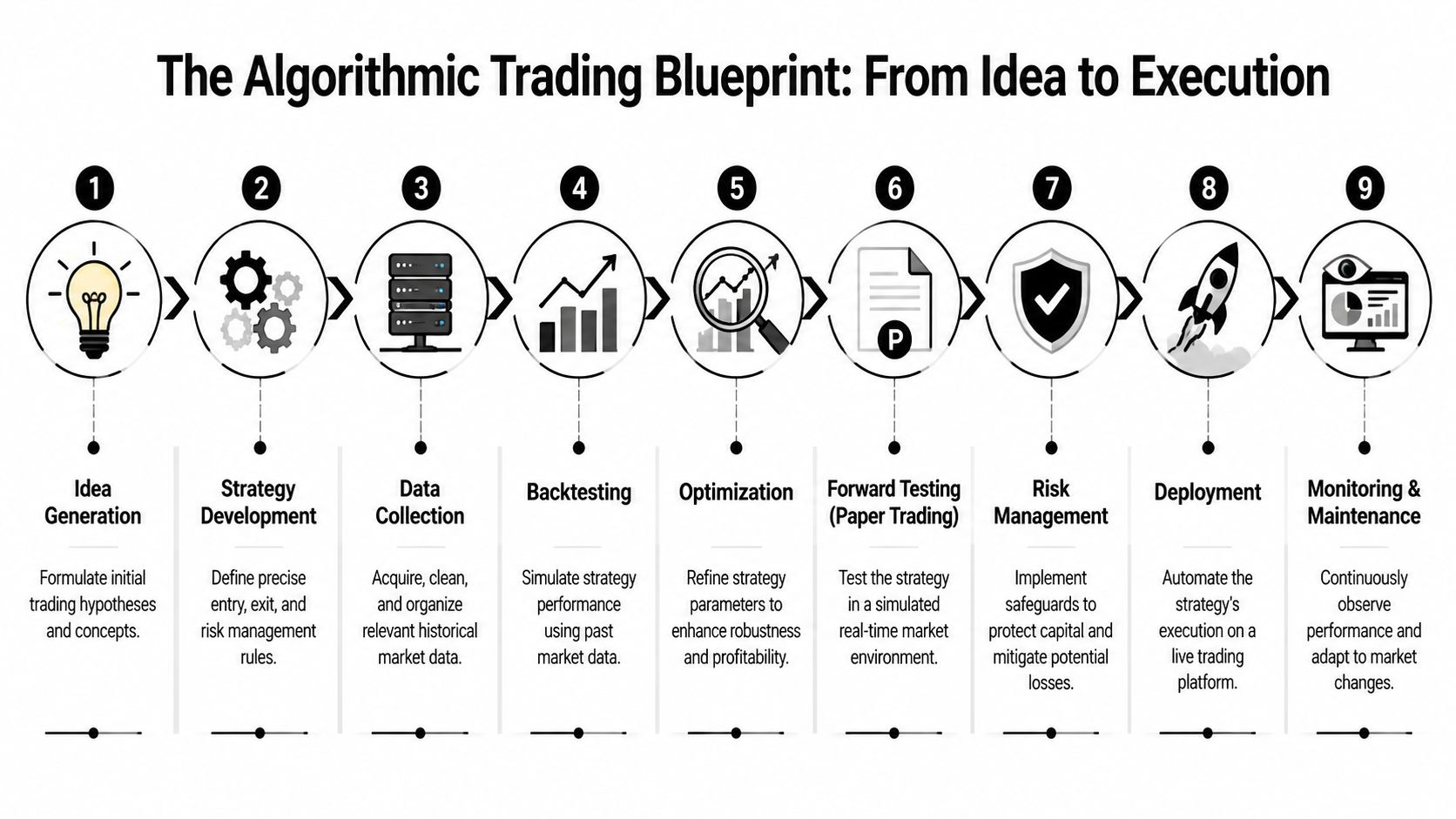

The Algorithmic Trading Blueprint From Idea to Execution

Algorithmic trading isn't a niche corner of the market anymore. Algorithms account for roughly 60 to 75% of trading volume in major equity markets, according to an industry summary on algorithmic trading statistics. That matters because you're not stepping into a slow market where loose execution can hide weak process. You're competing in an environment shaped by rule-based systems.

The seven-stage workflow that actually works

Most new traders blur research, testing, and live trading into one messy loop. That's how they end up changing a strategy after every losing streak. A cleaner workflow looks like this:

Ideation

Start with a market behavior, not an indicator. Trend persistence after breakout, mean reversion after exhaustion, momentum during session overlap, range behavior after failed expansion. The idea comes first. The indicator is just a way to express it.Data sourcing

Get the right data for the way the strategy trades. If your system reacts intraday, daily bars won't tell you enough about path, spread, or fill quality.Strategy coding

Translate the idea into fixed rules. Entry, exit, stop logic, position sizing, session filters, and no-trade conditions all need exact definitions.Backtesting

Test on historical data with costs included. If the strategy only works before costs, it doesn't work.Optimization

Tune carefully. Small, sensible parameter ranges are fine. Endless tweaking usually means you're fitting noise.Forward testing

Put the algo in paper trading or a demo environment and watch how it behaves bar by bar in live conditions.Live deployment

Run it with operational controls. Logging, reconnect logic, platform monitoring, and hard risk limits matter as much as signal generation.

What separates hobby scripts from tradable systems

A beginner usually asks, "Can I automate this setup?" A trader trying to pass a prop evaluation should ask better questions:

- Can this logic survive a spread spike

- Can it obey a daily loss rule automatically

- Can I explain when it should be turned off

- Can I verify fills and slippage on my platform

- Can I monitor it without staring at it all day

Practical rule: If you can't describe why a strategy should work in one plain paragraph, you shouldn't code it yet.

The blueprint also needs one extra layer that most generic articles miss. In a prop setting, your strategy isn't judged only by return. It's judged by whether it can operate inside firm rules without accidental breaches. That changes how you build everything from sizing logic to daily shutdown conditions.

Designing and Coding Your First Trading Algorithm

The fastest way to fail at how to trade with algorithms is to begin with platform syntax. Python, C#, and MQL5 are just implementation tools. The hard part is turning a trading belief into a rule set that can be tested without ambiguity.

Start with a market hypothesis, not a favorite indicator

A solid first algorithm usually comes from one of a few simple ideas:

- Trend-following: Price continuation after confirmation.

- Mean reversion: Reversal after overextension.

- Breakout: Expansion after compression.

- Session behavior: Different conditions around opens, overlaps, or closes.

Keep the first version narrow. One setup, one instrument group, one timeframe family. Don't combine five ideas into a "smart" strategy and call it diversification. That's usually just complexity hiding uncertainty.

A useful way to think about the design process:

- Behavior first: What repeated market pattern are you trying to capture?

- Trigger second: What exact condition defines entry?

- Risk third: What gets you out when you're wrong?

- Exit logic last: How do winners end? Fixed target, trailing stop, opposite signal, or session close?

Use statistics where they matter

A recent 2025 study in Nature Scientific Reports found that increased algorithmic trading was correlated with lower short-term volatility, with measured declines in several intraday volatility metrics in the sample studied, as reported in the Nature paper on algorithmic trading and market quality. For a retail trader, the practical takeaway isn't academic. It means algo trading sits on top of measurable market structure, so your design process should include tools like volatility regimes, autocorrelation, and sometimes cointegration rather than pure chart pattern intuition.

The cleaner your statistical framing, the easier it is to tell whether the strategy failed because the idea was bad or because execution was bad.

Common Algorithmic Strategy Types

| Strategy Type | Core Logic | Best Market Condition | Example Indicator |

|---|---|---|---|

| Trend-following | Enters in the direction of established movement | Sustained directional markets | Moving average |

| Mean reversion | Fades short-term overextension back toward a baseline | Range-bound or stretched markets | Bollinger Band |

| Breakout | Enters when price escapes a defined range | Compression followed by expansion | Donchian channel |

| Momentum filter | Ranks strength and trades with relative pressure | Clean directional sessions | Rate of change |

If you want more setup ideas before coding, this guide on algorithmic trading strategy ideas is a useful starting point.

Choose tools that match your platform

For most traders, the stack is straightforward:

- Python: Good for research, prototyping, and data work.

- C# for cTrader: Good if you plan to run cBots directly on cTrader.

- MQL5: Common if you're building around MetaTrader workflows.

- Spreadsheets plus scripting: Fine for simple logic validation before full automation.

The mistake is trying to build industrial infrastructure on day one. You don't need a giant architecture to test a simple rule-based strategy. You do need clean code and explicit logic.

A practical coding checklist

Before you call a strategy "ready for testing," make sure the code answers these questions:

- Entry definition: Exactly what must happen for a trade to open?

- Exit definition: What closes the trade in profit, loss, or timeout?

- Sizing rule: Is lot size fixed, volatility-based, or equity-based?

- Session filter: When is trading allowed or blocked?

- Conflict handling: Can the algo open multiple positions at once?

- Failure state: What happens if data is missing or the platform disconnects?

Your first algorithm should be boring. Boring is good. Boring means you can explain it, test it, and fix it.

The Litmus Test Backtesting and Forward Testing

A backtest can lie to you in ways that look professional. Nice equity curve, acceptable drawdown, plenty of trades. Then you run it live and the edge disappears because your fills are worse, the spread widens at the wrong time, or the strategy only worked in one market regime.

A good backtest is not enough

This is the point most articles miss. The question isn't "did it backtest well?" The question is "did it survive realistic validation?"

According to LuxAlgo's strategy development best practices, rigorous testing should include a train and validation split, forward testing with realistic transaction costs, multiple market cycles, and at least 100 trades for statistical reliability. That's a much higher standard than loading a chart, pressing run, and admiring the result.

If you need a primer on testing workflows, this walkthrough on how to backtest trading strategies helps frame the basics.

What to include in your validation process

A serious validation stack usually includes:

- In-sample testing: Used to develop the initial logic.

- Out-of-sample testing: Held back until after development.

- Walk-forward testing: Repeatedly re-trains and tests through time.

- Paper trading: Runs in live market conditions without real capital impact.

- Cost modeling: Includes commissions, spread, and slippage assumptions.

Don't treat optimization and validation as the same thing. Optimization tries to improve a model. Validation tries to break it.

Curve-fitting usually looks impressive

Overfitted systems often share the same warning signs:

- Too many parameters: Every extra switch gives you another way to fit noise.

- Fragile settings: A small parameter change ruins results.

- One regime dependence: It works only in a narrow historical window.

- Unrealistic execution assumptions: The test assumes fills you won't get live.

One hard lesson: If a strategy needs perfect historical tuning to work, live markets will punish it quickly.

A simpler system with fewer moving parts often survives longer because you can understand its failure modes. That's especially important in prop evaluations, where a temporary breakdown can violate your loss limits before you diagnose the issue.

Metrics that matter more than headline return

New traders fixate on total profit. Professionals care more about consistency and pain.

Review your test with questions like these:

- How bad were the losing streaks

- How quickly did the strategy recover after drawdown

- Did performance hold across bull, bear, and sideways conditions

- Were there enough trades to trust the result

- Would this equity curve be psychologically tradable under prop rules

A strategy that produces decent expectancy with manageable drawdown is usually more usable than one with a flashy historical return and ugly path dependence.

Deploying Your Algorithm on a Live Platform

Live deployment is where many decent strategies break. Not because the logic is wrong, but because the operational setup is weak. Beginner content often stops at paper trading, yet the move from test results to live execution is where data quality, slippage, and out-of-sample behavior become decisive, as noted in Interactive Brokers' guide to beginner algorithmic trading.

Local machine or VPS

You can run an algo on your own computer. Many traders do at first. The trade-off is reliability.

A local setup can work if you:

- Trade limited sessions: You only need the bot active during specific hours.

- Monitor it directly: You're nearby and can restart it if needed.

- Accept interruption risk: Power, internet, updates, and sleep mode can kill execution.

A VPS is usually the more practical choice when:

- You need stable uptime

- You want lower latency to the broker environment

- You don't want your trading to depend on your laptop staying awake

For prop evaluations, reliability often matters more than shaving tiny amounts off execution speed. Missed stops, duplicate orders, or a frozen platform are much more dangerous than being a bit slower.

Platform-specific notes for cTrader and DXtrade

On cTrader, most algo traders use cBots written in C#. The main benefit is direct alignment between your strategy code and your execution platform. Your job is to keep the bot simple, log every decision, and test order handling under realistic session conditions.

On DXtrade, the workflow depends more on how you're integrating automation into the environment. The big priority is confirming what your strategy does at the order layer: market order, stop, limit, cancellation logic, and behavior during volatile periods. Don't assume a clean backtest translates into clean order behavior.

For traders looking for a prop-compatible environment that supports algorithmic trading on DXtrade and cTrader, MyFundedCapital's automated trading programs are one example of a setup built around that use case.

Your live deployment checklist

Before a bot touches a live evaluation, check these operational pieces:

- Logging: Record signals, orders, fills, errors, and shutdown events.

- Reconnect behavior: Define what the algorithm does after a disconnect.

- Position reconciliation: Confirm platform position state matches internal strategy state.

- Kill switch: Stop trading after abnormal execution or rule breach.

- Session controls: Block trading outside approved windows.

- Version control: Know exactly which code version is live.

Deployment mindset: Treat live trading like running software in production, not like launching an indicator on a chart.

A stable deployment isn't glamorous. It is what keeps a valid strategy from dying due to preventable execution mistakes.

Algorithmic Risk Management for Prop Firm Success

If you're building an algo for a prop challenge, your first priority isn't maximizing return. It's preventing disqualification. A simple strategy with disciplined controls usually beats a complex model with sloppy risk handling.

That fits what many retail traders learn the hard way. For most retail traders, the bottleneck isn't writing more complex rules but avoiding overfitting and managing risk. Simpler, transparent systems are often easier to validate and their failure modes are easier to predict, as explained in Finzer's discussion of algorithmic trading strategy trade-offs.

Build the prop rules into the code

If the firm uses a 5% daily loss limit and up to 10% maximum drawdown, those limits shouldn't live on a sticky note next to your monitor. They should sit inside the algo's risk layer. In the case of MyFundedCapital's account rules and trading conditions, those are part of the operating environment, so your code should respect them automatically.

Your strategy logic and your risk logic should be separate. Think of the risk layer as a supervisor that can override the setup logic at any time.

A practical master risk layer can include:

- Daily loss kill switch: Stops all new trading once the daily threshold is approached or hit.

- Equity-based sizing: Reduces position size automatically as account equity falls.

- Max trades per day: Prevents revenge-style overtrading coded into a loop.

- Session shutdown rule: Ends trading after a defined loss sequence or bad execution window.

- Instrument exposure cap: Prevents stacking correlated positions that behave like one oversized bet.

What usually fails in prop evaluations

Most failed algo challenges don't fail because the entry signal was terrible. They fail because the system had no guardrails.

Common failure patterns look like this:

- The bot keeps firing after a bad morning

- Lot sizing doesn't adjust after drawdown

- A ranging day triggers repeated false breakouts

- The algo opens correlated trades across several symbols

- A disconnect or execution error leaves an unmanaged position

Don't ask whether the strategy can make money first. Ask whether it can stay inside the rules on its worst day.

That's the right standard for how to trade with algorithms in a funded environment. Protect the account first. Preserve optionality. Then let the edge do its job.

Frequently Asked Questions About Algorithmic Trading

Do I need advanced math to trade with algorithms

No. You need logic, discipline, and a repeatable process more than academic credentials. Many tradable systems are based on simple rules that are well tested and tightly risk-managed. The challenge isn't making the idea sound complex. It's making it reliable.

Can I use a pre-built bot for a prop firm challenge

You can, but black-box bots create obvious problems. If you don't understand the logic, you won't know when to disable it, how to adjust the risk, or why it failed. A bot can only be useful in a prop setting if you can control its sizing, shutdown logic, and trading windows.

Is it better to code my own algorithm or buy one

Coding your own gives you transparency and control. Buying one may save time up front, but it often creates dependency on someone else's assumptions. A middle ground works well for many traders: start with a simple framework, then customize the rules and the risk layer yourself.

How long should I paper trade before going live

Long enough to catch execution issues, platform mismatches, and behavior across different sessions. The point of forward testing isn't to collect a pretty equity curve. It's to see whether the algo behaves as expected when the market is moving and your platform is handling real-time orders.

If you're ready to put this process into practice, explore MyFundedCapital to compare funding programs, review supported platforms like cTrader and DXtrade, and choose a challenge structure that fits your trading style. If you plan to run an algorithm, build it to respect the rules from day one. That's the difference between a bot that looks good in a backtest and one that's ready for evaluation.