You're probably here because discretionary trading feels messy, but fully automated trading still feels out of reach. That's a normal place to be. Learning how to trade with algorithms is less about finding a magic bot and more about building a process you can test, monitor, and trust under pressure.

The Foundation of Your Algorithmic Strategy

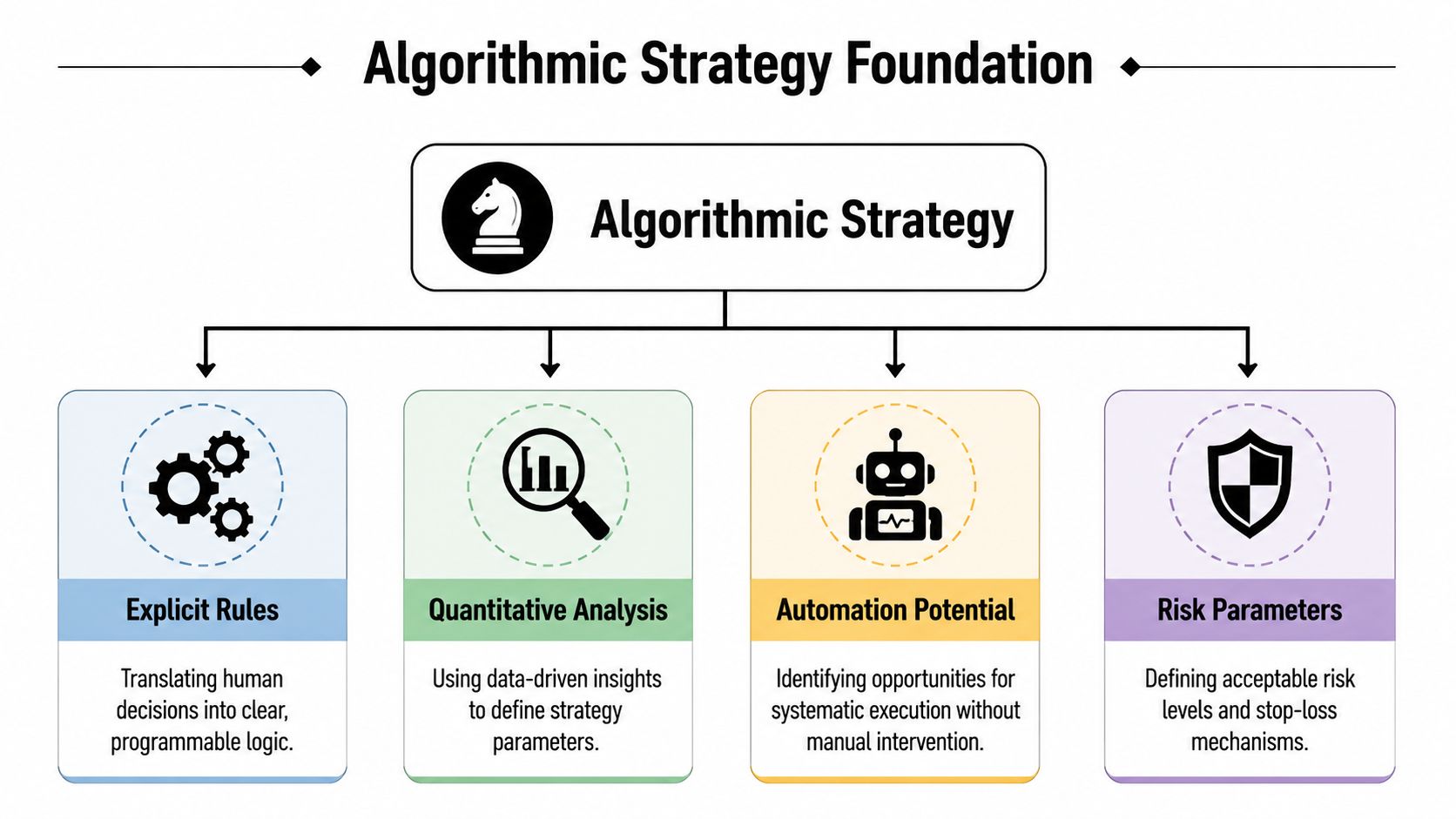

An algorithmic strategy isn't just a trade idea with alerts. It's a fully specified decision process. Every entry, every exit, every position size, and every risk limit has to be defined in a way a machine can execute without guessing.

That matters because machine-driven execution is already the norm, not the fringe. Projections for 2026 put algorithmic trading at roughly 60 to 75% of trading volume in major equity markets, with about 70% of U.S. stock market trading volume generated by algorithmic systems, according to algorithmic trading statistics. The same source notes that high-frequency trading firms make up about 2% of trading firms but generate roughly 73% of equity trading volume. If you want to compete in modern markets, rule-based execution isn't optional.

A good starting point is to understand the difference between these two statements:

- “I buy when price looks strong.”

- “I buy when the fast moving average crosses above the slow moving average, volatility is below my threshold, spread is acceptable, and the trade keeps portfolio risk within limits.”

Only the second one is fit for automation.

Think in rules, not opinions

Most beginners struggle because they try to automate a discretionary style that was never precise in the first place. If you can't explain your setup in plain language with no ambiguity, you can't code it well and you can't test it reliably.

Your first draft should answer four questions:

- What triggers the trade

- What invalidates the trade

- How much size the bot takes

- When the system stands down

That last one gets ignored too often. A strategy that only knows how to trade, but not when to stop, usually causes the damage.

Practical rule: If two different developers would code your logic in two different ways, your rules still aren't clear enough.

Choose a simple strategy archetype

Most retail traders should start with one of three broad models.

| Strategy type | Basic idea | Retail-friendly example |

|---|---|---|

| Mean reversion | Price stretches, then snaps back | Fade short-term extremes after a volatility spike |

| Trend following | Price movement persists | Trade in the direction of a moving average slope |

| Statistical arbitrage | Relative pricing creates opportunity | Trade a spread or paired relationship when it diverges |

You don't need to be fancy. You need to be testable.

A basic mean reversion system might buy after a sharp move down if the market is still above a higher-timeframe trend filter. A trend system might only take longs when the shorter average stays above the longer one. A relative-value system might compare two correlated instruments and act when their relationship deviates from normal behavior.

If you want examples of broader algorithmic trading strategies, that resource is useful for seeing how strategy logic changes across market types.

Define your edge in measurable terms

An edge isn't “this setup looks good.” An edge is a repeatable pattern that survives testing. Before you write code, write a one-paragraph strategy memo that includes:

- Market and timeframe: forex, indices, crypto, intraday or swing

- Setup logic: exactly what conditions must be true

- Execution method: market order, limit order, stop order

- Exit logic: stop loss, profit target, trailing exit, time stop

- Risk model: fixed fractional sizing, volatility sizing, hard stop on daily loss

If you need a clean overview of the building blocks, this guide on what algorithmic trading is is a useful baseline before moving into coding.

The traders who last in this game stop treating strategy ideas like inspiration. They treat them like systems.

Designing and Coding Your First Trading Bot

A trading bot is just your strategy translated into logic that a machine can execute the same way every time. Most bad bots fail before they ever reach the market because the logic was vague, inconsistent, or overloaded with conditions that sounded smart but didn't survive contact with real data.

Turn the idea into machine rules

Start with three blocks. Entry, exit, and sizing.

A weak spec sounds like this:

- Buy when momentum is strong

- Exit when momentum fades

- Risk a small amount

A usable spec sounds like this:

- Enter long when the fast moving average crosses above the slow moving average and spread is below your max threshold

- Exit if price hits the stop, reaches the target, or the averages cross back

- Size the trade so the predefined stop risks a fixed fraction of the account

That's enough to build a first bot.

Here's simple pseudocode for a moving average crossover:

IF no open position

AND fast_MA > slow_MA

AND previous_fast_MA <= previous_slow_MA

AND spread_ok

THEN

calculate_position_size_based_on_risk

place_buy_order

set_stop_loss

set_take_profit

END IF

IF long_position_open

AND fast_MA < slow_MA

THEN

close_position

END IF

That's not advanced. It doesn't need to be. First bots should be clear, not clever.

Pick the language that fits your platform

Retail traders often overthink language choice. The better question is what environment you'll run.

- Python: great for research, prototyping, data work, and custom workflows

- C#: natural fit if you're building on cTrader through cAlgo

- MQL5: useful for MT5 users and existing EA ecosystems

- API-first setups: often a practical option on platforms like DXtrade if you want language flexibility

If you're using a platform builder or hiring a developer, your job is still the same. You must define the rules precisely enough that implementation doesn't require interpretation.

For traders looking at retail-friendly bot frameworks and execution ideas, this overview of strategies for algo trading helps map strategy logic to actual platform workflows.

A bot doesn't become good because the code is elegant. It becomes useful because the rules are unambiguous and the execution behavior matches the design.

Build around failure points early

Most first bots focus only on entries. That's backward. Entries are easy. Failures usually come from exits, duplicate orders, bad state handling, and risk logic that breaks when conditions change.

Use this pre-code checklist:

- Order handling: What happens if the order is partially filled or rejected?

- Position awareness: Can the bot detect whether it already has exposure?

- Session rules: Will it trade during illiquid periods, news spikes, or rollover?

- Risk limits: What happens after a losing streak or abnormal spread?

- Logging: Can you see why the bot entered, exited, or skipped a trade?

A junior trader often asks what to automate first. The honest answer is the part you already execute consistently by hand. If your discretionary process changes every week, coding it just locks in confusion.

Keep version one narrow

Your first bot should trade one market, one setup, and one timeframe. Don't build a “universal AI system” that tries to scalp, trend trade, mean revert, and hedge itself across everything.

That approach usually creates two problems:

- You can't tell what's working.

- Debugging becomes a nightmare.

A narrow system gives you feedback you can use. Once the logic is stable and the results make sense, then you can expand.

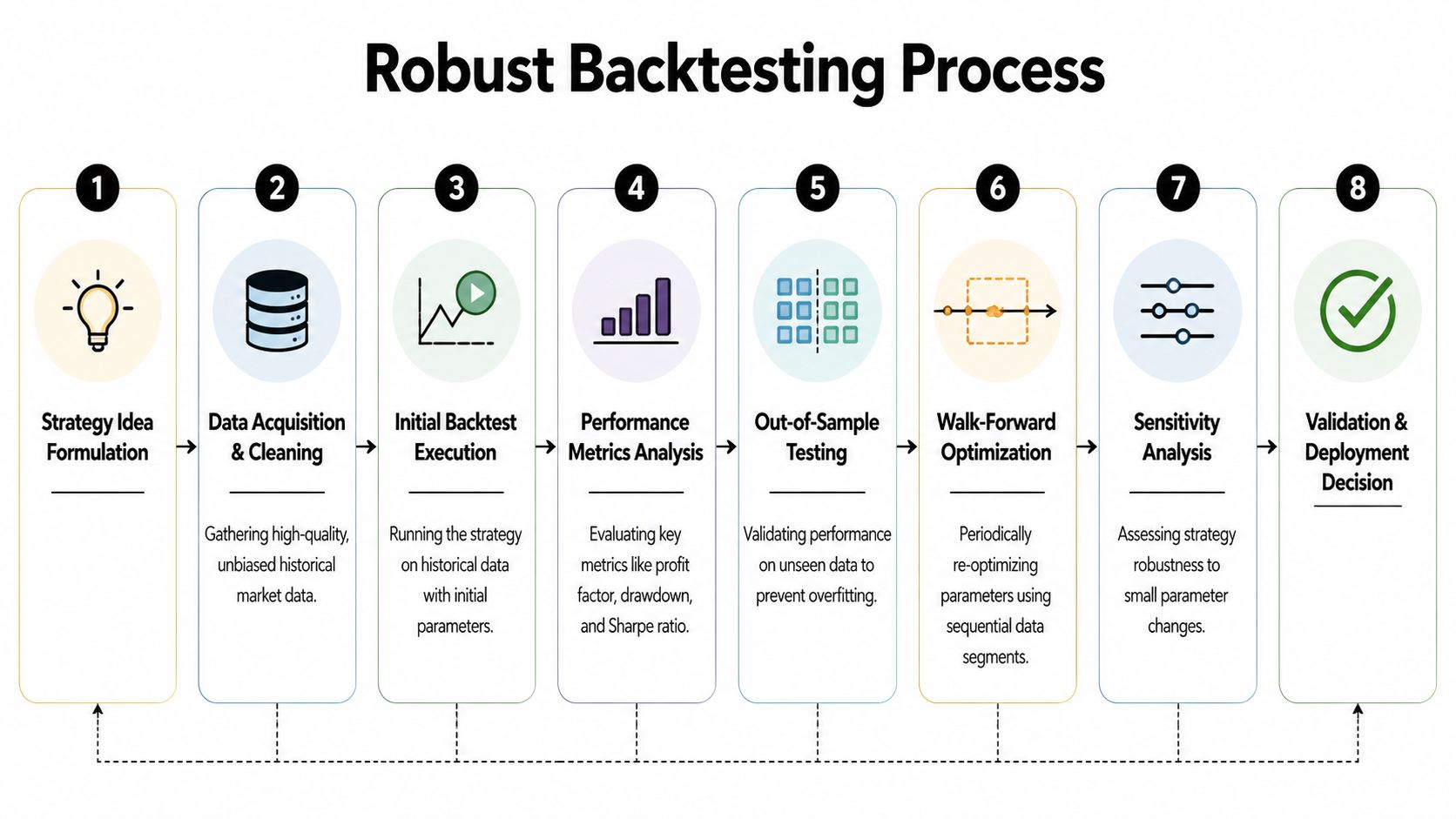

Rigorous Backtesting and Validation Methods

A profitable backtest can still be worthless. That's the part many traders learn the hard way.

The standard workflow is straightforward: define the strategy with explicit rules, backtest it on clean historical data, then validate it with out-of-sample and walk-forward testing before paper trading and going live, as Interactive Brokers explains in its guide to algorithmic trading for beginners. The dangerous mistake is skipping validation. A strategy can look strong in-sample and then fail once market conditions shift.

Why simple backtests fool traders

A simple backtest answers one narrow question. “Did this logic make money on this historical sample?”

That's useful, but not enough. It doesn't answer:

- Whether the result depends on one lucky period

- Whether small parameter changes break the system

- Whether your assumptions about spread, fills, and slippage are realistic

- Whether the strategy survives a different market regime

If you optimize too aggressively on one dataset, you usually end up fitting noise. The equity curve looks smooth. Live trading looks ugly.

Hard truth: The cleaner and prettier the backtest, the more suspicious you should become if the strategy logic is complex.

Use a validation stack, not one test

A stronger process looks like this:

| Stage | Purpose | What to watch for |

|---|---|---|

| In-sample test | Develop the initial model | Don't over-tune parameters |

| Out-of-sample test | Check unseen data | Similar behavior, not exact replication |

| Walk-forward test | Simulate repeated adaptation over time | Stability across changing conditions |

| Paper trading | Test live behavior without capital risk | Execution mismatches and logic bugs |

At this point, traders should slow down.

If a strategy only works with one exact moving average length, one exact stop distance, and one exact session filter, that's usually a warning. Resilient systems tend to tolerate modest changes without collapsing.

Test what actually breaks live systems

Most retail backtests ignore the details that matter later. That's a mistake.

Focus your review on these points:

- Data quality: bad candles and missing data ruin conclusions

- Execution assumptions: market orders and limit orders behave differently

- Trade clustering: losses often arrive in streaks, not neat alternation

- Regime behavior: some systems die in chop, others die in trend

- Parameter sensitivity: slight changes shouldn't destroy the edge

A lot of traders only ask, “Did it make money?” A better question is, “Why did it make money, and does that reason still make sense?”

If you're building a proper testing workflow, this guide on what backtesting is is worth reviewing alongside your platform's own tester documentation.

A practical pass or fail standard

You don't need perfection. You need consistency.

A strategy earns the next stage when:

- The logic makes economic sense

- Out-of-sample performance is still credible

- Walk-forward behavior doesn't collapse

- The system survives different conditions without needing constant rescue

- The backtest assumptions are conservative enough to survive real execution

If any of those fail, keep it in research. Don't push a fragile system live just because the equity curve looked exciting.

Deployment and Paper Trading Your Algorithm

Once the strategy has survived testing, the next problem is operational. Can the bot run reliably when you're asleep, when your internet drops, or when the platform reconnects after a disruption?

That's why serious deployment starts with infrastructure, not optimism.

Use a stable execution environment

Running a bot from a home laptop sounds convenient until the machine sleeps, updates, crashes, or loses connectivity. A VPS is the usual solution because it gives your bot a more stable environment and keeps it closer to continuous uptime.

The setup usually includes:

- Trading platform or execution engine

- Broker or platform API connection

- A hosted environment such as a VPS

- Logging and alerting

- A manual shutdown path

If you're trading on cTrader, native bot deployment is more straightforward because the platform was built with algorithmic workflows in mind. If you're using DXtrade or another API-access environment, the main concern is whether your order routing, authentication, and position tracking behave predictably under real-time conditions.

For traders who want a broader technical view of market infrastructure, including exchange-style architecture and on-chain order book DEX development, it helps to study how matching, order state, and execution pathways are designed. Even if you never build an exchange, the mindset is useful.

Paper trading is where the real bugs show up

A paper account is the first place your strategy meets live conditions without the cost of live mistakes. This phase is about checking whether the bot behaves as designed when prices update in real time, orders are submitted live, and the market doesn't follow your backtest script.

Watch for issues like:

- Missed signals: the backtest entered, but the live bot didn't

- Duplicate entries: reconnects and retries can create accidental stacking

- Incorrect stops or targets: order logic often fails at the edges

- Session timing errors: timezone and rollover bugs are common

- Unexpected state drift: the bot thinks it is flat when it isn't

Paper trading doesn't prove your strategy has an edge. It proves your software can survive contact with the market.

Treat deployment like a dress rehearsal

The right mindset is simple. Your first live environment should be boring.

Use a checklist before every run:

- Confirm data feed integrity

- Check platform connection and API permissions

- Verify symbol mapping and contract specifications

- Review risk settings and trade size constraints

- Test alerts and emergency shutdown procedures

If you can't explain exactly how the bot starts, trades, logs, fails, and stops, it isn't ready. Most losses blamed on strategy weakness are often basic deployment mistakes wearing a different name.

Live Risk Management and Performance Monitoring

A live algorithm isn't a vending machine. It's a process that can drift, break, misread data, or execute badly even when the core idea is sound.

At the execution layer, algorithmic trading is often about order management, not just signals. Common institutional styles include VWAP, TWAP, implementation shortfall, POV, and liquidity-seeking approaches, all designed to split larger orders and reduce market impact and execution cost, as summarized in this overview of algorithmic trading and execution methods. The same source highlights the operational side that retail traders often underestimate: a sound setup needs broker API access, continuous monitoring, and risk controls such as stop losses, position-size limits, daily loss limits, and circuit breakers. Even live algorithms need active monitoring for feed delays, execution errors, and unusual behavior.

Hard-code the risk rules

If you're trying to trade in a funded-account style environment, risk controls can't be optional. They need to exist in code, not just in your intentions.

Your live bot should include:

- Per-trade stop loss: every trade needs a predefined invalidation point

- Position-size cap: the strategy shouldn't scale exposure because of emotion or code bugs

- Daily loss limit: if the bot hits the threshold, it stops trading

- Circuit breaker: pause trading after repeated errors, abnormal spread, or unusual slippage

- Kill switch: a manual and automatic way to shut the system down

This is what traders mean when they say the risk model matters more than the signal once you go live.

Monitor the bot like an operator

A trader who says “my bot trades by itself” usually hasn't traded live for long. Live systems need supervision.

Track these in real time:

| What to monitor | Why it matters | Typical response |

|---|---|---|

| Data feed health | Bad data creates bad signals | Pause trading if feed quality degrades |

| API connectivity | Lost connection can leave stale assumptions | Reconcile open positions immediately |

| Fill quality | Slippage can erase the edge | Adjust order type or stop trading |

| Strategy drift | Live results can diverge from tested behavior | Investigate before increasing size |

| System health | Server or process issues stop execution | Restart only after state checks |

The market rarely sends you a warning label. Your monitoring stack has to do that job.

Watch for performance drift, not just losses

A strategy can stay profitable for a while and still be degrading. Maybe entries are arriving late. Maybe spread has widened during the hours you trade. Maybe the logic still works, but execution quality has slipped enough to weaken the edge.

Review logs and trading behavior regularly:

- Compare live entries to expected model signals

- Check whether stop and target placement match the design

- Flag abnormal fill patterns

- Review skipped trades and rejected orders

- Pause the system if behavior no longer matches the tested model

The traders who keep bots running the longest are usually the least romantic about them. They don't defend the system. They audit it.

FAQ About Algorithmic Trading

Can I trade with algorithms on a prop firm account

Yes, if the firm allows algorithmic trading and your setup follows the account rules. In practice, that means your bot has to respect platform limits, risk limits, and prohibited-strategy rules. The platform matters too. cTrader is generally bot-friendly, while API access and implementation details can vary on other environments such as DXtrade.

Before you deploy anything, check three things:

- Platform compatibility: can your bot run natively or through an API

- Risk rule compliance: does your bot enforce daily and overall drawdown limits

- Execution style: does the strategy rely on behavior the firm may restrict

Do I need to be a professional coder

No. You do need to think clearly.

A trader with average coding skill and excellent strategy discipline usually does better than a strong coder with vague trading logic. You can build with Python, C#, MQL5, no-code tools, or by hiring a developer. The hard part isn't typing syntax. It's specifying the system so that another person, or a machine, can execute it exactly.

That said, basic technical literacy helps. You should understand logs, parameters, order states, and how to verify whether the bot did what it was supposed to do.

What are realistic profit expectations

There isn't a fixed answer, and anyone promising one should make you cautious. Algorithmic trading doesn't remove risk. It changes the form of the work.

Your target should be process quality first:

- Is the edge well defined

- Has the strategy survived validation

- Does live execution match the model

- Are losses contained when conditions change

That mindset sounds less exciting than social media promises. It's also the one that keeps traders in the game.

How much capital do I need to start

It depends on your route. Self-funded traders may need to budget for data, software, hosting, and testing infrastructure. The exact amount varies by market, platform, and toolset, so it's better to plan qualitatively than guess.

If you're researching the broader direction of finance technology and where automation fits into trading workflows, this industry piece from NineArchs LLC is a useful read for context.

A practical approach is to start small, keep your system narrow, and prove the workflow before you scale anything. Most traders don't fail because they started too small. They fail because they scaled a weak process.

If you want to apply this workflow in a funded-account environment, explore MyFundedCapital. You can compare challenge types, review supported platforms like cTrader and DXtrade, and choose a path that fits manual or algorithmic trading. Trading involves risk of loss. This content is educational only and not financial advice.