A trader clears the profit target halfway through a prop challenge, then gives it all back in two sessions because the strategy was never tested against the daily drawdown rule. That happens more often than traders admit. Backtesting exists to prevent that kind of avoidable failure.

Backtesting means applying a strategy’s rules to historical market data before risking real money. The point is practical. You want to see how the method behaves across different conditions, how ugly the losing streaks get, and whether the risk profile still works when real constraints apply, including the hard loss limits common in funded programs such as MyFundedCapital.

Good backtesting is not about proving a system will win in the future. It is about checking whether the rules have shown consistent behavior in the past, with enough trades and enough market variety to expose weak spots. In practice, that means testing more than entries and exits. It also means testing position sizing, stop placement, session filters, and whether one bad day would have breached a daily or maximum drawdown cap.

Skip this work and the market usually sends the bill later. The strategy may look fine on a chart and still fail the first time volatility expands, spreads widen, or a normal losing streak collides with challenge rules. That is how traders lose money, lose accounts, or fail evaluations with a setup that seemed solid in theory.

What is Backtesting and Why It Is Non-Negotiable

Backtesting answers a simple question: if I had followed these exact rules in the past, what would the results have looked like? That’s it. Not “would I have felt confident.” Not “does this setup look clean.” The test is whether the rules produce a result when applied consistently.

The flight simulator analogy fits because a simulator doesn’t make someone a pilot on its own. It does show whether the pilot can follow a system before getting in a real cockpit. Backtesting does the same for traders. It lets you test entries, exits, stops, position sizing, and market selection without paying tuition to the market first.

Why serious traders use it

Backtesting isn’t a retail shortcut. It came out of professional quantitative trading. The practice took shape in the quantitative finance wave of the 1980s, and firms such as D.E. Shaw and Renaissance Technologies helped turn it into a professional standard. One example often cited is Renaissance’s Medallion Fund, which produced an average annual return of 66% before fees from 1988 to 2018 using computationally intensive backtests on historical market data (LuxAlgo on backtesting metrics and history).

That history matters because it shows how professionals think. They don’t deploy first and hope later. They test first, then decide whether the edge is real enough to risk capital on.

Practical rule: If you can’t describe your strategy in exact rules, you can’t backtest it properly.

What backtesting does for a trader

A solid backtest helps you answer questions that matter:

- Does the setup have an edge: Are the rules profitable over a meaningful sample, or are you cherry-picking charts?

- Can you survive the bad periods: Winning systems still go through drawdowns, clusters of losses, and flat periods.

- Does the strategy fit your style: A strategy can be profitable and still be a terrible match for your patience, schedule, or risk tolerance.

- Would the rules hold up inside prop limits: A strategy that looks fine on a normal equity curve can still fail under strict daily and overall drawdown rules.

Traders usually want certainty. Backtesting won’t give that. It gives something more useful. It gives evidence.

The Trader's Toolkit Data and Software

Most weak backtests fail before the first result prints. The problem is usually bad data, lazy assumptions, or software set up in a way that flatters the strategy instead of testing it accurately.

Start with data, not indicators

The core input is OHLCV data, meaning open, high, low, close, and volume. If that data is incomplete, misaligned, or poorly adjusted, the test result is unreliable. That’s the classic garbage-in, garbage-out problem.

Backtesting precision depends on high-quality OHLCV data, proper timestamps, and realistic assumptions about market behavior. Gaps, errors, or failure to adjust for corporate actions can distort the whole result. For platform-based trading, the test also needs to reflect real execution conditions such as slippage and commissions. A strategy can show 200% total profit and still be unusable if it also carries a 45% maximum drawdown, especially under a 10% maximum drawdown rule (Trade With The Pros on data quality and backtesting accuracy).

What to check before you trust the data

Use this checklist:

- Check completeness: Missing bars can break indicator logic and create fake signals.

- Check timestamps: Time zone mismatches can ruin session-based strategies.

- Check adjustments: For stocks, splits and dividends matter. For CFDs and forex, rollover behavior and session boundaries matter.

- Check execution assumptions: Add commissions, slippage, and realistic fills.

- Check instrument behavior: Crypto, indices, forex, and commodities don’t all trade with the same rhythm.

A clean equity curve built on dirty data is still dirty.

Choosing software that matches your style

You don’t need to code to start. Manual chart replay works for simple discretionary systems if your rules are tight and you record every trade. But once the strategy gets more detailed, automation saves time and removes human bias.

Common options include:

- Platform tools: cTrader and DXtrade-style environments are useful when you want testing close to the platform where you’ll execute.

- Dedicated backtesting software: Good for structured reports and repeatable tests.

- Python frameworks: Useful when you need custom rules, portfolio logic, or prop-style restrictions.

If you’re building repeatable systems, it helps to borrow ideas from software development best practices. Version control, testing changes one at a time, and documenting assumptions all reduce the chaos that ruins strategy development.

For traders comparing practical tools, MyFundedCapital also has a guide to back test software for traders that breaks down what to look for in a testing setup.

Key Backtesting Methods Explained

A trader spends two weeks tuning an EURUSD breakout system, runs one backtest, and sees a smooth equity curve. Then the same system hits a prop challenge, clips the daily loss limit in three sessions, and the account is gone. The problem usually is not the idea itself. The problem is the testing method.

Different backtesting methods answer different questions. One helps build the strategy. Another checks whether it still works on unseen data. A third shows whether it can survive the kind of regime shifts that wreck funded accounts.

In-sample testing

In-sample testing is where strategy development happens. You pick a block of historical data, set the rules, and adjust entries, exits, filters, or risk parameters until the system behaves reasonably.

That process is useful. It is also where traders do the most damage.

If you keep tweaking until every dip in the past is smoothed out, you are not improving the strategy. You are fitting it to noise. I see this a lot with newer traders chasing the "perfect" stop size or session filter. The result looks clean in the report and falls apart the moment conditions change.

For prop-style trading, in-sample work should include the actual rule set you plan to trade under. That means testing position sizing, loss caps, and shutdown rules that respect maximum drawdown limits in funded accounts, not just raw return.

Out-of-sample validation

Out-of-sample validation is the first real stress check. After building the strategy on one historical segment, you freeze the rules and test them on a different period the system has not seen.

At this stage, inflated confidence usually gets cut down to size.

A strategy that stays reasonably profitable out of sample has a chance. A strategy that collapses as soon as optimization stops was never stable enough to trust with challenge capital. In practice, I do not look for perfect continuity between the two periods. I look for behavior that is still recognizable. Similar trade logic, manageable drawdowns, and no sudden dependence on one market phase.

| Method | What happens | What it tells you |

|---|---|---|

| In-sample | You build and tune the strategy on one historical segment | Whether the idea can be shaped into a rules-based system |

| Out-of-sample | You test fixed rules on unseen data | Whether the edge survives outside the development window |

| Walk-forward | You repeat build, validate, and roll forward through time | Whether the strategy can adapt to changing conditions without constant rescue |

Walk-forward testing

Walk-forward testing is the method I trust most once a strategy looks promising. You optimize on one period, test on the next, then roll the window forward and repeat. That process is slower, but it is much closer to live trading because markets do not stay still.

This method matters even more if your goal is to pass a challenge at a firm like MyFundedCapital. A strategy can look excellent across one cherry-picked year and still fail under recurring drawdown rules. Walk-forward testing exposes whether a system keeps producing acceptable results as volatility, trend strength, and session behavior shift over time.

Good testing also depends on clear reporting and disciplined review. Teams working in analytics in finance use repeated validation cycles because one attractive result is never enough to trust a model with capital. Traders should apply the same standard.

One more practical point. Do not hunt for one magical setting. A strategy that only works with a 17-period filter, a 1.3 ATR stop, and one exact session cutoff is fragile. A strategy that still works with modest parameter changes is usually the one worth taking forward.

Measuring What Matters Performance and Risk Metrics

A backtest can show a rising equity curve and still be untradable.

That happens all the time in prop evaluations. A strategy makes money in the report, then breaks a daily loss limit after two bad sessions or clips the overall drawdown cap before the edge has time to play out. If you trade with firms like MyFundedCapital in mind, the job is not to find the prettiest return number. The job is to find out whether the strategy can survive the rules.

The metrics worth your attention

Start with the small group of numbers that affect live decisions:

| Metric | What It Measures | What to Look For |

|---|---|---|

| Profit Factor | Gross profit divided by gross loss | Higher is better, but only if the trade count and drawdown also make sense |

| Sharpe Ratio | Risk-adjusted returns | Helps show whether returns came with controlled volatility or a rough equity curve |

| Maximum Drawdown | Worst peak-to-trough decline | Must sit comfortably inside the risk limits you plan to trade under |

| Expectancy | Average profit per trade | Shows what each trade is worth over a large sample |

| Calmar Ratio | Return relative to drawdown | Useful for judging whether the return was earned efficiently |

As noted earlier in the article, experienced quants often judge backtests by the relationship between return and pain, not by profit alone. The practical benchmark is simpler than any single number. The strategy should make enough, lose in a controlled way, and do it across a sample large enough to trust.

Read the report like someone who has to keep the account

Profit factor gets abused a lot. A high number can come from a small sample, one outsized winner, or a strategy that barely traded. Expectancy has the same problem. Positive expectancy is good, but it means little if the distribution of outcomes includes strings of losses that would push you into a rule breach before the average edge shows up.

Maximum drawdown usually decides whether a system is usable. If your backtest shows a 9 percent drawdown and your challenge allows 10 percent, that is not a safety margin. That is a warning. Slippage, spread widening, missed fills, and one ugly week can close the gap fast. Review your maximum drawdown rules in prop trading with that in mind.

Sharpe and Calmar help sort smooth systems from stressful ones. I care about Calmar more than many retail traders do because it forces return to justify drawdown. In funded trading, that matters. You are not trying to impress anyone with a heroic equity swing. You are trying to stay inside hard risk limits long enough to finish the objective.

For a broader view of how professionals evaluate consistency, risk, and decision quality with data, this overview of analytics in finance is a useful reference. Trading system review should follow the same standard. Measure what affects survival and repeatability.

Put every metric next to the rulebook

A clean backtest usually shows three things:

- Drawdowns stay well below the account limits, not just barely under them.

- Returns are earned without violent equity swings.

- Profit factor, expectancy, and drawdown support the same story instead of contradicting each other.

That last point matters. If profit factor looks strong but drawdown is ugly, something is off. If expectancy is positive but one losing streak would fail the challenge, the edge may be real but the execution plan is wrong for that account type.

A useful backtest report answers one practical question. Can this strategy survive the rules while still producing enough return to matter? If the answer is unclear, the test is not finished.

Common Backtesting Pitfalls That Invalidate Results

A trader passes a challenge in the simulator, then blows the account in week one of live execution. The market usually is not the actual problem. Bad testing is.

Backtests fail for predictable reasons, and each one gets more expensive when you trade under prop firm rules. A strategy can show a nice equity curve and still be unusable if the test ignored execution, used future information, or was tuned so aggressively that one normal losing day would breach a daily drawdown limit at a firm like MyFundedCapital.

Overfitting turns a strategy into a costume

Overfitting happens when you keep adjusting inputs until the past looks clean. Change the moving average lengths. Add one more session filter. Tighten the stop. Remove a few ugly trades. After enough tweaking, the system starts fitting noise instead of behavior that can repeat.

I see this a lot with challenge-focused traders because the temptation is obvious. They are not only trying to find an edge. They are trying to find an edge that also stays inside hard rules on daily loss, maximum drawdown, and consistency. That pressure leads some traders to optimize for the report instead of the market.

A useful test should still work when conditions are a little worse than expected.

Look-ahead bias poisons results

Look-ahead bias means the strategy used information that was not available at the decision point. Sometimes that happens in code. Sometimes it shows up in manual testing when the trader can already see how the candle finished before deciding on the entry.

That single mistake can make an average strategy look disciplined and profitable.

The practical test is simple. Ask what you knew at that exact bar, tick, or session close. If your rules depend on the final high, low, or close of a candle before that candle closes, the result is contaminated. If your backtest assumes the perfect fill inside a fast move, the result is contaminated. If your stop and target both sit inside the same bar and your software always gives you the favorable outcome, the result is contaminated.

Small samples create false confidence

A short run of good trades proves very little. Ten wins in a row can happen in a weak system. So can one clean month.

The question is whether the strategy has seen enough conditions to expose its flaws. That means enough trades, enough different volatility regimes, and enough ugly periods where execution gets harder and discipline slips. If you only test the recent trend, you are not testing resilience. You are grading the strategy on its favorite exam.

This matters even more for prop challenges. A low-frequency setup may look safe because it rarely trades, but that also means one bad sequence can define the whole evaluation.

Costs and execution assumptions ruin many "good" systems

A strategy that survives only with zero slippage and ideal fills does not survive. Spread, commission, slippage, partial fills, rollover, and session liquidity all belong in the test.

Backtests often separate retail hobby results from trading results you can use.

Scalping systems are the usual casualty, but swing traders are not exempt. News spikes, gaps, and thin sessions can push a perfectly acceptable paper drawdown into a rule breach in a funded account. If your test says the worst day was close to the daily loss limit before realistic costs, then the live version is already too fragile.

Rule drift makes manual backtests unreliable

Manual testing can work well, but only if the rules are specific enough that another trader would take the same trade. If one day you skip a valid setup because it "looked weak," and the next day you include a borderline trade because it "fit the context," you are no longer testing a strategy. You are testing your memory and your mood.

That kind of drift usually flatters the results. Traders remember the clean entries and explain away the ugly ones.

Write rules that remove interpretation wherever possible. Entry, exit, invalidation, trade window, sizing, and what to do after a loss all need to be defined before the test starts.

A short pitfall checklist

When results look unusually smooth, check these first:

- Future leakage: Did the setup use information from a bar that had not closed yet?

- Ignored costs: Did the test include spread, commissions, slippage, and realistic fills?

- Over-optimization: Did small parameter changes destroy the edge?

- Weak sample: Did the strategy face enough trades and enough market conditions?

- Rule drift: Would two traders following the written rules take the same trades?

- Prop rule mismatch: Did you test against daily drawdown and maximum drawdown limits, or only total return?

- Survivorship bias: Did you only test symbols and periods that were easy to trade in hindsight?

A backtest is valid only if it survives hard questions. If it breaks the moment you apply real execution and funded-account risk rules, it was never ready.

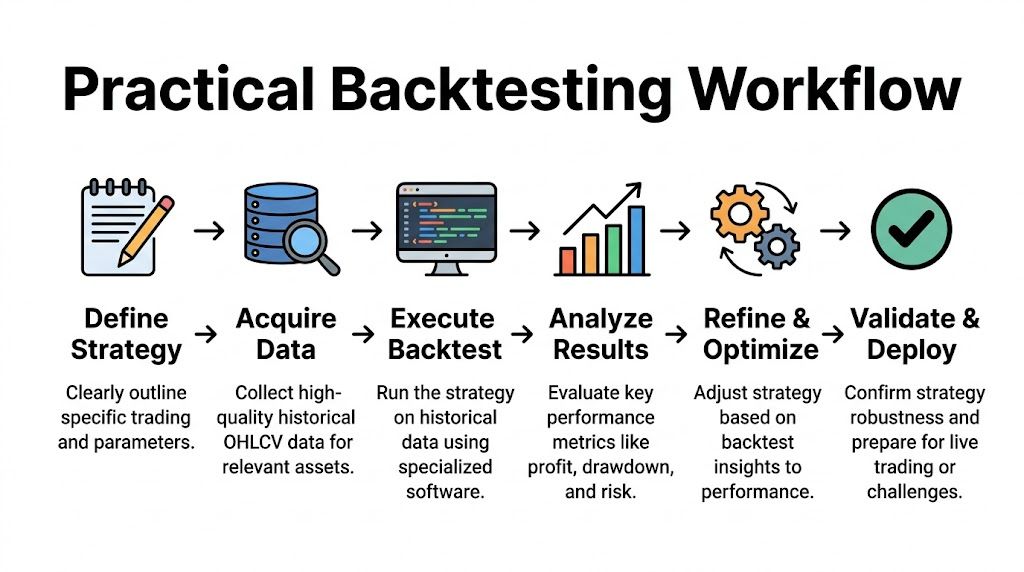

A Practical Backtesting Workflow Step by Step

The cleanest way to backtest is to treat it like a process, not a one-off experiment. That keeps you from jumping between indicators, changing rules mid-test, and fooling yourself with selective memory.

The six-step workflow

Define the strategy

Write exact rules for entry, exit, stop-loss, sizing, trading session, and filters. “Buy strong momentum” is useless. “Buy when the 20 EMA crosses above the 50 EMA on the H1 chart and price closes above both averages” is testable.Acquire the data

Use historical data that matches the asset and timeframe you plan to trade. If the strategy depends on session timing or event behavior, make sure the dataset reflects that.Execute the backtest

Run the strategy through software or a disciplined manual replay. Include costs and realistic execution assumptions.Analyze the results

Look at the full picture, not just profit. Read the equity curve, losing streaks, drawdown profile, and basic performance metrics together.Refine and optimize

Make small changes with a reason. Change one thing at a time so you know what improved or harmed the system.Validate and deploy

Confirm the rules still hold up on unseen data. If they do, move to forward testing or a simulated environment before trusting the strategy in a challenge.

What usually works, and what doesn't

What works is boring. Clear rules, clean logs, honest assumptions, and patient iteration.

What doesn’t work is also predictable:

- Constant tweaking: If you edit after every ugly patch, you never learn what the strategy really is.

- Jumping timeframes: Traders often rescue weak logic by moving to another chart instead of fixing the underlying rule set.

- Testing without notes: If you don’t document what changed, you can’t repeat the result.

A backtest is only useful when someone else could reproduce it from your notes and get the same output.

Interpreting Results for Funded Trading Challenges

A strategy can be profitable and still be a terrible fit for a funded evaluation. That’s where many traders get blindsided. They test for return, then fail on risk rules.

Read the backtest through challenge rules

Standard backtests often ignore prop-specific constraints. That matters because challenge accounts don’t just care whether the strategy makes money. They care whether you stay within the rules while making it.

One major overlooked issue is daily loss control. Verified industry material notes a 70% to 80% challenge failure rate when traders ignore prop-specific rules in testing, and recommends simulating hard stops such as a 5% daily loss limit to judge whether the strategy is viable for funded trading (Indeed background reference as specified in verified data).

What to look for in a challenge-ready report

Focus on these practical questions:

- Does the equity curve stay orderly: A strategy with violent swings may pass a normal backtest and still breach daily limits.

- Would any loss cluster break the rules: Review the worst days, not just the average day.

- Does the trade frequency fit the evaluation: Slow strategies can be valid, but they may not suit the structure or goals of a challenge.

- Are there rule-sensitive exposures: News trading, overnight holds, and weekend gaps need to be modeled if they apply to your style.

If funded trading is the goal, you need to test for challenge survival, not just theoretical profitability. That’s the difference between a strategy that looks good in a spreadsheet and one that can survive a live-style evaluation like a prop firm challenge.

Frequently Asked Questions About Backtesting

| Question | Answer |

|---|---|

| Do I need to know coding to backtest a strategy? | No. You can start with manual chart replay if the rules are simple and objective. Coding becomes more useful when you want speed, consistency, or custom logic. |

| How much historical data is enough? | It depends on trade frequency, but the minimum standard is 100 trades, and strong testing often means using data that covers multiple market cycles. Slow strategies usually need a much longer historical window than fast ones. |

| Should I trust a strategy or EA I bought online? | Not without testing it yourself. Treat every prebuilt system as unproven until you’ve run it on your own data, with your own execution assumptions and risk rules. |

| What matters more, win rate or drawdown? | Drawdown usually matters more. A high win rate can hide poor risk control, while a lower win rate system can still be solid if expectancy and drawdown are healthy. |

Backtesting is educational, not predictive. Markets change, execution differs, and trading always carries risk of loss. Nothing in a backtest guarantees future results, and none of this is financial advice.

If you want to put your strategy in a structured environment, review the funding options at MyFundedCapital, compare the account types, and choose a challenge that matches your trading style and risk control.