You're probably used to thinking about capital in trading terms: account size, margin, drawdown, financing cost. Companies think the same way, just on a bigger stage. If you understand how funding capital projects works, you get a cleaner read on management quality, balance-sheet risk, and whether a big announcement is a smart investment or an expensive headline.

What Is a Capital Project and Why Traders Should Care

A company opens the quarter with stable margins and decent guidance. Then management announces a multiyear buildout for a new plant, data center, logistics network, or enterprise software rollout. The stock may move on the headline. The better question is what the project says about future cash flows, financing pressure, and management judgment.

A capital project is a large investment in an asset expected to produce value for years rather than months. It usually involves construction, major equipment, infrastructure, or a large technology system. Routine operating spend keeps the current engine running. A capital project changes the engine's capacity, cost structure, or strategic position.

For traders, that difference matters because capital projects are forward bets. Management is committing real capital today in exchange for uncertain cash flows later. In trading terms, it resembles putting on a long-duration position where the payoff depends on entry price, timing, volatility, and execution.

Capex versus opex in trader language

The cleanest way to frame this is capex versus opex.

Operating expense works like your recurring trading overhead. Data feeds, software subscriptions, exchange fees, and connectivity costs support activity right now. Capital expense works like buying a faster workstation, building an execution system, or funding research infrastructure you expect to use across many trading cycles.

That time horizon changes the analysis.

A trader can tolerate a one-month spike in expenses if it helps current performance. A capital project asks a tougher question. Will this asset earn more than it costs over its useful life? That is the corporate-finance version of asking whether a trade has positive expected value after financing and execution costs. If you want a better feel for how financing cost feeds into that decision, start with these interest rate benchmarks used across credit markets.

What a capital project signals to the market

A major project announcement is rarely just a growth story. It is management revealing its internal thesis about the business.

Read it like a position statement:

- Demand thesis. The company expects volume growth and needs more capacity.

- Margin thesis. New assets should lower unit costs or improve mix.

- Competitive thesis. Management believes standing still would weaken the franchise.

- Compliance thesis. The firm must spend to meet regulatory, safety, or infrastructure requirements.

Each thesis has a market implication. If the project is well chosen and funded sensibly, future earnings power can improve. If the project is late, over budget, or financed poorly, equity holders may absorb the damage through weaker returns, dilution, or balance-sheet stress.

That is the angle many public-sector or CFO-focused guides miss. Traders are not just asking, "Can the project be built?" They are asking, "What does this project do to valuation, credit risk, and the stock's upside versus downside?"

Why traders should care before the first shovel hits the ground

Capital projects can change a company before the asset produces a dollar of revenue.

They affect free cash flow, debt needs, interest expense, covenant headroom, and sometimes share issuance. They also reveal whether management allocates capital like a disciplined investor or like a promoter chasing scale. In that sense, project funding is close to reading position sizing in a trading book. Two traders can hold the same view, but the one using better sizing and financing usually survives long enough to profit.

This is also why understanding the capital stack gives you an edge in equity analysis. In real estate, for example, layered funding structures show how risk and return are split among participants. The same logic appears in corporate projects, and the framing in Homebase real estate investment strategies is a useful parallel if you want to see how stacked capital affects incentives.

A capital project, then, is not just a big expense line. It is a long-dated wager on future economics. Traders who can read that wager clearly have a better shot at spotting strong management teams, fragile balance sheets, and stock stories that are stronger or weaker than the headline suggests.

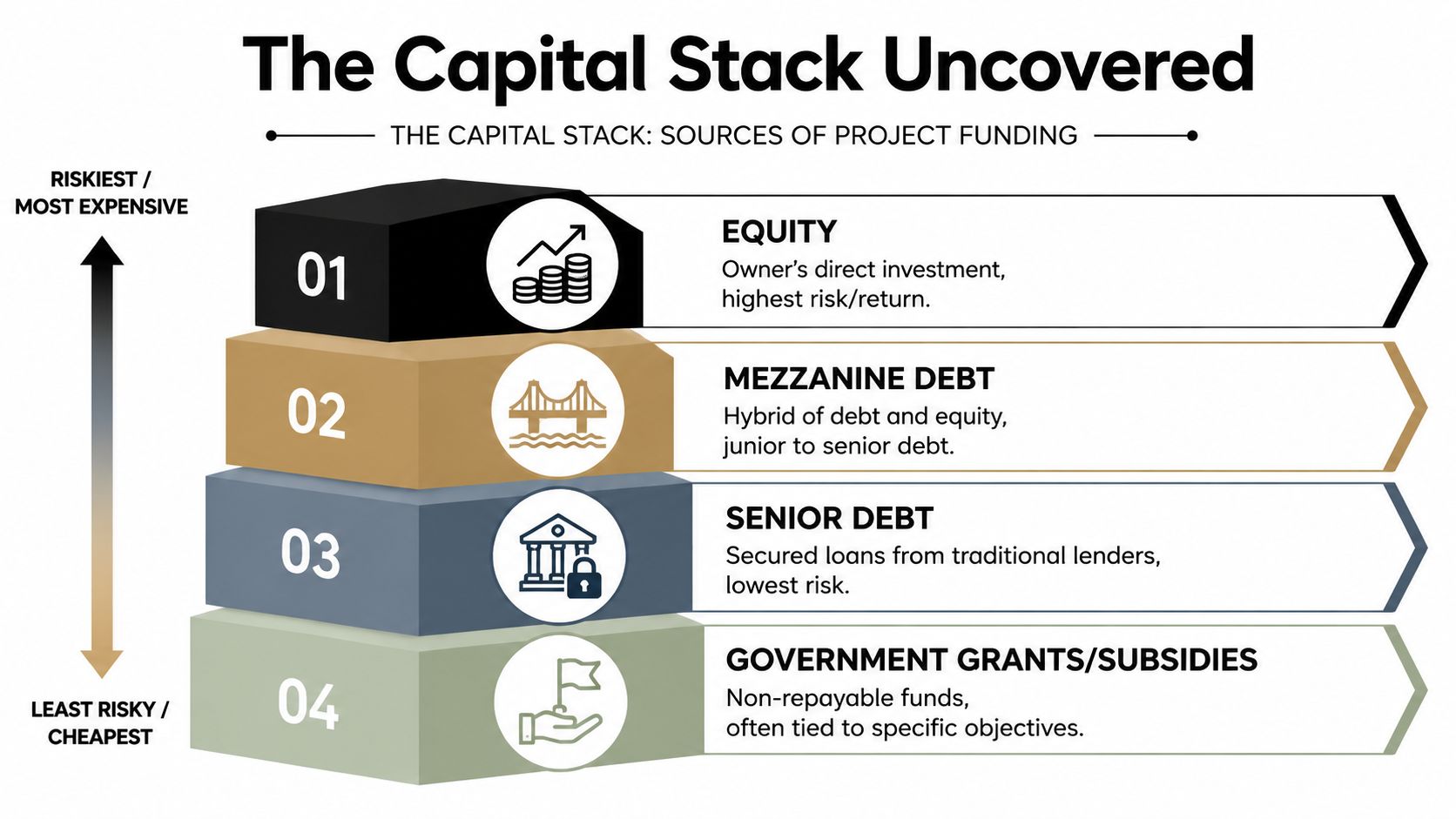

The Capital Stack Uncovered Sources of Project Funding

A capital project is rarely funded with one clean source of cash. Companies usually build a capital stack, a layered funding structure that decides who gets paid first, who takes more risk, and what the project will cost to carry before it starts producing cash.

For traders, that matters because the stack changes the payoff profile. Two companies can announce the same factory, data center, or network build. One funds it with cheap long-term debt and retained earnings. The other leans on expensive capital or dilutive equity. The project may look identical in a press release, but the equity story is not the same.

Debt financing versus equity financing

Start with the first split: debt and equity.

Debt is borrowed money with a contractual repayment schedule. Equity is capital contributed by owners, whether that comes from retained earnings or from issuing new shares. As noted in Tennessee's overview of capital funding sources and debt financing, capital projects often rely on debt-related tools such as bonds, notes, and leases.

The trader's lens helps here. Debt functions much like financed exposure. The company keeps control of the asset and any upside after obligations are met, but it now has fixed payments, refinancing risk, and covenant pressure. Equity removes the fixed repayment burden, yet it spreads the upside across more owners and can reduce control for existing shareholders.

That trade-off is the heart of the funding decision.

Debt versus equity funding comparison

| Feature | Debt Financing (e.g., Bonds, Loans) | Equity Financing (e.g., Stock Issuance) |

|---|---|---|

| Ownership | Existing owners usually keep control | Ownership can be diluted |

| Cash obligation | Requires scheduled repayment | No mandatory repayment schedule |

| Risk to company | Higher default or refinancing pressure | Higher dilution pressure |

| Return expectation | Lenders want contractual payment | Equity holders want long-term upside |

| Best fit | Predictable cash flows, long-lived assets | Early-stage growth, high uncertainty, balance-sheet flexibility |

Why debt appears so often in project funding

Long-lived assets pair well with long-term debt because the funding period can be aligned with the asset's useful life. A company building a plant that should generate value for decades does not want to fund the whole thing from current cash if that would strain liquidity or crowd out other opportunities.

This is duration matching in plain English. You would not want a trade with a long time horizon financed by a structure that has to be rolled constantly at uncertain prices. Companies face the same problem. If the asset matures slowly but the financing is short and fragile, the project can be economically sound and still create balance-sheet stress.

That is one reason debt is common. It can lower the immediate hit to cash while preserving ownership.

The stack is usually layered

Real projects often combine several sources, each with its own claim on cash flows:

- Senior debt, which usually has the first claim and the lowest required return

- Equity, contributed by owners or funded through retained earnings

- Hybrid capital, including mezzanine-style instruments that sit between debt and equity

- Grants or subsidies, used when the project serves a narrow public or policy goal

Read the stack from top to bottom as a risk ladder. The safer the claim, the lower the expected return. The more junior the claim, the higher the required return because that investor gets paid later and absorbs more downside first. Traders already know this logic from how different layers of a trade structure affect who gets protected and who gets the convex upside.

The same framework shows up clearly in property deals, which is why the Homebase real estate investment strategies piece is a useful parallel. Real estate investors break funding into tranches because each layer changes incentives, downside protection, and return targets. Corporate capital projects follow the same basic logic even when the asset is a plant or transmission network instead of a building.

One more practical point. The cost of each layer moves with rates and credit conditions, so the same project can look attractive in one financing market and much tighter in another. When you review a company's funding announcement, it helps to anchor that analysis to current interest rate benchmarks. That gives you a faster read on whether management locked in reasonable terms or committed the company to an expensive stack.

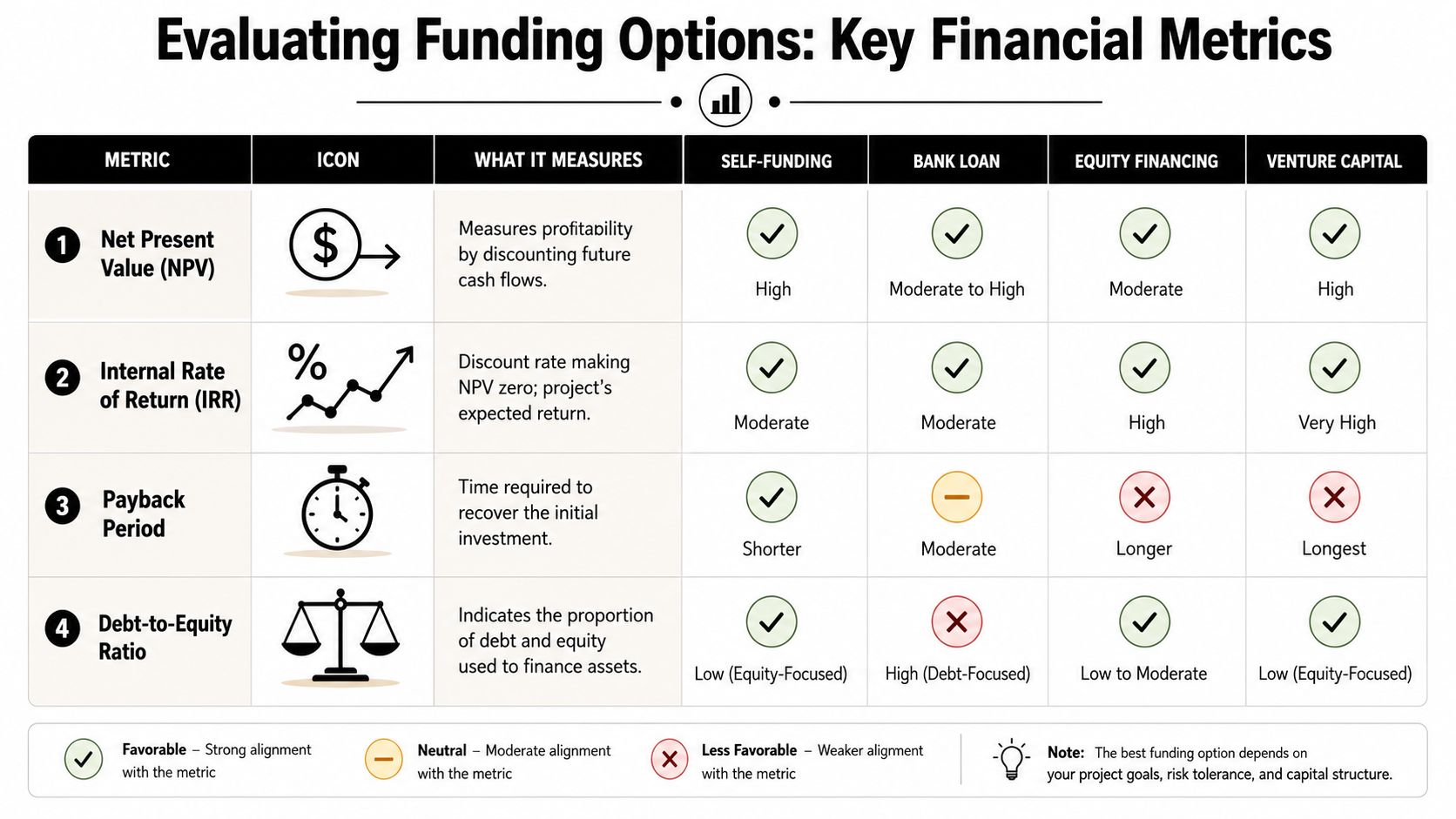

How to Evaluate Funding Options With Key Metrics

A company can have access to funding and still make a bad capital decision. The true test is whether the project is worth doing after adjusting for timing, risk, and financing cost.

That's where core metrics come in. The big ones are NPV, IRR, and the company's cost of capital. You don't need to be a CFO to use them. You just need to think in discounted cash flows instead of headlines.

Think of NPV like trade expectancy

Net Present Value (NPV) asks a simple question: if we discount future cash flows back to today, does the project create value above its cost?

In trader language, it's similar to asking whether a strategy's future expected gains are worth the capital and risk committed today.

A positive NPV usually means the project clears the required return hurdle. A negative NPV means management is effectively paying too much for the expected payoff.

A simple example without fake precision

Suppose a company is considering a new facility.

- It spends a large amount upfront.

- It expects the facility to generate cash inflows over several years.

- Finance discounts those future inflows back to present value.

- If present value exceeds upfront cost, NPV is positive.

No magic. Just time-adjusted math.

IRR and why traders should care

Internal Rate of Return (IRR) is the discount rate that makes NPV equal zero. You can think of it as the project's implied annualized return.

If IRR is above the company's cost of capital, the project may make sense. If it's below, it may destroy value even if the story sounds good.

Don't confuse a good story with a good spread. Traders know this instinctively. Capital budgeting works the same way.

Match funding to asset life

One core rule matters more than most formulas. The financing structure should match the asset's useful life. Longer-lived assets are usually better paired with long-term financing, while using short-term debt for a long project can create refinancing risk, as explained in OpenGov's discussion of how to finance capital projects and the pros and cons of each method.

That's the same mistake a trader makes when financing a long-duration idea with funding that can vanish too soon.

A practical checklist for evaluating funding capital projects

- Start with cash flows. Don't begin with the financing press release. Begin with what the asset is expected to earn or save.

- Check time horizon. The longer the asset lasts, the more important duration matching becomes.

- Separate project quality from funding convenience. Cheap debt can make a weak project look acceptable.

- Evaluate the debt load. A good project can still strain a balance sheet if the company stacks on too much debt.

- Stress assumptions. Delays, lower demand, and cost overruns can flip a project from attractive to marginal.

In construction-heavy industries, estimating discipline matters before financing even starts. Tools such as Exayard plumbing estimating software show the kind of operational detail that feeds cleaner project budgets. Better estimates won't guarantee a good investment, but they reduce the odds that management is underwriting fantasy.

To turn the financial influence of projects into trading intuition, adopt a margin loan calculator mindset. The same core question applies: how much financing can the cash flows support before the structure becomes fragile?

Understanding Risk Allocation in Project Finance

A financing deal isn't just about raising money. It's about deciding who absorbs which failure mode.

That matters because capital projects face several predictable risks. Construction can run late. Demand can come in lower than expected. Rates can move. Political or regulatory conditions can change. Input costs can rise. Each of those risks affects equity holders, lenders, contractors, customers, or taxpayers differently.

Read project finance like a hedge structure

Traders already understand risk allocation. You size positions, set stops, hedge exposures, and avoid taking risks you aren't being paid for. Project finance applies the same discipline through contracts instead of orders.

A well-designed project structure tries to place each risk with the party best able to manage it:

- Construction risk often sits with contractors through build terms and performance obligations.

- Financing risk often sits with the borrower and lenders through rate terms, covenants, and repayment schedules.

- Operating risk may sit with the asset owner or operator.

- Policy risk may remain partly unavoidable, especially in regulated sectors.

Why this matters for stock analysis

A company that keeps all project risk on its own balance sheet may get more upside, but it may also be more exposed if something goes wrong. A company that allocates risk carefully may look slower or more conservative, but it can be more resilient.

That's useful when you're reading earnings calls or capex announcements. Ask:

- Who takes the hit if construction slips?

- Who bears rate risk?

- Is project debt tied to the asset, or does it threaten the whole company?

- What assumptions must hold for repayment to work?

Risk allocation is the capital-project version of not letting one bad trade blow up the account.

For traders building the same habit in their own work, these best practices for risk management offer a familiar framework. The setting is different, but the logic is identical. Survive first, optimize second.

A Glimpse at Deal Structuring and Documentation

By the time a capital project reaches closing, the easy part is over. The story has been sold, the rough economics have been modeled, and the parties now need documents that turn intention into enforceable commitments.

The term sheet is the project blueprint

A term sheet is usually the starting point. It lays out the broad economics and structure:

- funding source

- repayment logic

- pricing

- maturity

- security or collateral

- conditions that must be met before money is released

It's not the whole legal package, but it tells you what the deal probably looks like.

The key documents signal seriousness

After that come the heavier documents. Their names vary, but the functions are familiar:

- Loan agreement for debt terms, covenants, events of default, and repayment mechanics

- Security documents for collateral rights

- Shareholder or equity agreements if outside equity is involved

- Construction and operating contracts that define who does the work and who carries which obligations

We plan to build” evolves into “we're legally committed to build, borrow, and perform.

What traders should take from the paperwork

A signed financing package tells you more than a press release does. It says management has moved from narrative to obligation.

That matters because formal documents force specificity. Vague optimism gets replaced by repayment schedules, draw conditions, milestones, and downside provisions. When a firm reaches that stage, the project is no longer just strategic messaging. It's a real capital commitment with measurable consequences for future cash flows and risk.

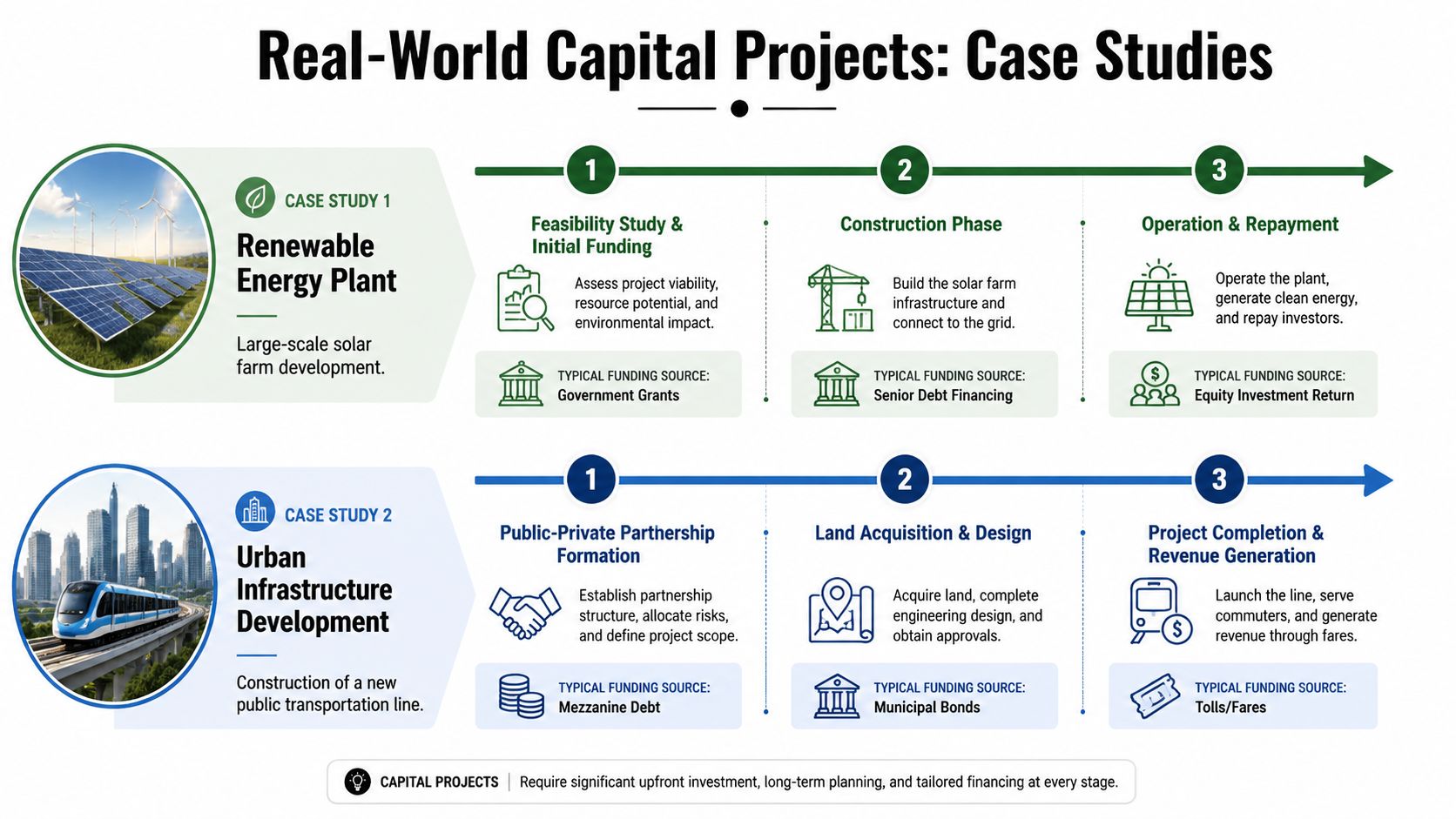

Real-World Examples of Capital Projects

A trader scans two headlines before the open. One company announces a factory expansion. A public agency announces funding for broadband and community facilities. Both sound like simple growth stories. They are not. Each is really a financing story about who supplies the capital, what conditions come attached, and how long the market may wait for proof.

Public example with targeted capital funding

A good public example is the U.S. Treasury's Capital Projects Fund, discussed earlier. The important lesson for traders is not just that governments can supply project money. It is that the money comes with a narrow mandate, defined uses, and a staged award process.

That structure matters. Public capital often works like a limit order, not a market order. The funding is available only at specific terms and for specific assets. If a project fits those terms, financing can become possible. If it does not, the theoretical capital is irrelevant.

From an analyst's perspective, this tells you to read beyond the headline amount. Ask:

- who is eligible

- what asset types qualify

- whether funds arrive all at once or in tranches

- what long-term service or capacity the project is supposed to create

That lens helps traders avoid a common mistake. Announced funding is not the same as economically flexible funding.

Corporate example with analyst-style reading

Now shift to a corporate case. Suppose a company plans a new data center, factory expansion, or logistics hub. Management may not publish the full capital stack, but you can still build a solid view from public clues.

Start with the balance sheet. A company with modest debt and ample liquidity has more room to fund a long-dated asset without straining itself. A company already near its covenant limits may still build the asset, but the market should treat the financing choice as part of the thesis, not as a side detail.

Then ask what the asset is supposed to do. Some projects increase volume. Others lower unit cost. Others remove a bottleneck that has been capping revenue. Those are very different payoff patterns. In trading terms, you are estimating whether the company is buying more upside, more resilience, or conversely, more complexity.

The timing matters too. A project with cash flows that arrive years from now usually fits better with long-term debt or patient equity than with short-term funding. That is the same matching problem traders see in positions. You do not want a financing clock that expires before the thesis has time to play out.

Watch execution just as closely as funding. A company that has delivered similar projects before deserves a different probability weighting than one trying something new in an unfamiliar region or technology.

The market often reacts on announcement day. Subsequent repricing usually comes later, when construction progress, budget discipline, and early operating results either support or weaken the original thesis.

An opportunity exists for traders to get an edge over headline readers. Do not stop at “management is investing.” Ask whether the project's expected return is likely to clear its cost of capital. That is the corporate version of asking whether a trade has positive expected value.

A well-funded project can strengthen a bullish view by expanding capacity or improving margins with a financing mix the company can carry. A poorly funded one can dilute shareholders, pressure cash flow, or trap the firm in years of underwhelming returns even if reported revenue rises.

FAQ and Funding Your Own Trading Ambitions

What's the difference between capital spending and operating spending

Start with the time horizon.

Capital spending buys or builds something expected to produce benefits for years. Operating spending keeps the current engine running. A new plant, warehouse upgrade, or software platform usually sits in the first bucket. Payroll, rent, utilities, and routine maintenance usually sit in the second.

For a trader reading filings, that distinction matters because each type of spending changes the story in a different way. Operating spending affects near-term margins. Capital spending affects future capacity, depreciation, financing needs, and, if management is right, later cash flow. It is similar to separating a trade entry cost from the capital you commit to a longer-duration position. One hits current performance quickly. The other is meant to shape future returns.

Why do grants rarely solve the whole problem

Grants usually fill one layer of the stack, not the whole stack.

They often come with restrictions on timing, eligible uses, reporting, or matching requirements. That means a company, nonprofit, or public entity still has to assemble the rest of the funding package with debt, equity, internal cash, donations, or partner capital. As noted earlier, grants are often partial and conditional, which makes them helpful but rarely sufficient on their own.

For traders, the takeaway is simple. If management announces grant support, do not stop at the headline. Ask what share of the total project cost it covers, what conditions attach to it, and what funding gap still needs to be filled.

Does project debt automatically make a stock less attractive

No. The better question is whether the debt fits the asset and the company.

Debt can work well when the project has visible cash flows, the repayment schedule lines up with the asset's useful life, and the issuer keeps enough liquidity to absorb delays or cost overruns. Debt becomes dangerous when maturities are too short, covenants are tight, or the project needs perfect execution to service the obligation.

A trader can read this like position sizing. Borrowing against a high-conviction setup with defined risk is very different from borrowing against a thin thesis that needs everything to go right. Same tool. Different outcome.

How does this help me as a trader

It improves how you judge management quality.

A company that funds projects with discipline is often showing more than financing skill. It is showing how it underwrites risk, how it matches funding to payoff timing, and how realistic it is about downside cases. Those habits can support a stronger stock over time because they affect dilution risk, interest burden, and the odds that a project earns more than its cost of capital.

There is a personal parallel too. Traders need their own capital structure. Some self-fund and grow slowly. Some keep size small until their process is consistent. Some use external capital models with strict rules. The right choice depends on your edge, your drawdown profile, and how much pressure your strategy can handle before execution degrades.

MyFundedCapital is one example of a prop firm offering simulated funded trading programs through instant funding and challenge-based models. Treat that as a structure to evaluate, not as a shortcut. Review the drawdown rules, payout terms, scaling conditions, and reset mechanics the same way you would review covenants and waterfall terms in a project deal.

Capital helps. It does not fix weak execution.

That is the core lesson in both project finance and trading. More money behind a bad process usually increases the size of the mistake. Use the same analyst mindset on yourself that you use on companies. What is the expected payoff? What can break? How much room do you have before a temporary drawdown becomes a permanent loss?

Trading involves risk of loss. This article is educational only and not financial advice.

If you want to apply the same capital-allocation thinking to your own trading, take a look at MyFundedCapital. Compare account types, review the risk parameters, and decide whether a funded model fits your strategy, time horizon, and risk tolerance.