You've probably hit this wall already. You have a setup that works when you're focused, rested, and at the screen, then a rushed click, a missed entry, or a rule bend ruins the day.

That's where an algorithmic trading strategy starts to matter. Not because automation is magic, but because it forces your logic into rules you can test, monitor, and enforce under pressure. This guide is educational only, not financial advice, and trading always involves risk of loss.

Introduction Why Manual Trading Is Not Enough

Manual trading breaks down in predictable ways. Attention slips. Execution gets inconsistent. A decent system turns random because the trader changes size after a loss, skips a valid signal, or takes a low-quality trade out of boredom.

That problem gets worse when you try to scale. You can't watch every pair, every session, and every trigger without missing something. You also can't trade with machine-level consistency when the market speeds up.

By 2019, about 92% of FX trading volume was driven by automated strategies rather than human decision-making, which shows how heavily modern currency markets depend on systematic execution and why sound, risk-aware strategy design matters for anyone trading in that environment (algorithmic trading in FX).

What automation fixes, and what it doesn't

An algorithmic trading strategy can help with:

- Rule enforcement: The system takes only the trades that match your conditions.

- Execution discipline: It enters, exits, and sizes positions without hesitation.

- Market coverage: It can monitor more instruments and more time windows than a human can.

- Repeatability: You can test the same logic on historical and live data.

It won't fix bad logic.

Practical rule: If you can't explain your edge in a few plain sentences, you're not ready to automate it.

The real shift from discretionary to systematic

Most traders shouldn't start by trying to build a complex black box. Start by turning one discretionary habit into explicit logic:

- Define the setup clearly: What has to happen before you enter?

- Define the invalidation: What proves the trade is wrong?

- Define the exit logic: Fixed target, trailing logic, time exit, or signal reversal?

- Define the risk budget: How much damage can one trade, one session, or one day do?

That's the bridge from theory to execution. In a prop-style environment with hard limits, that bridge matters more than having a clever indicator stack.

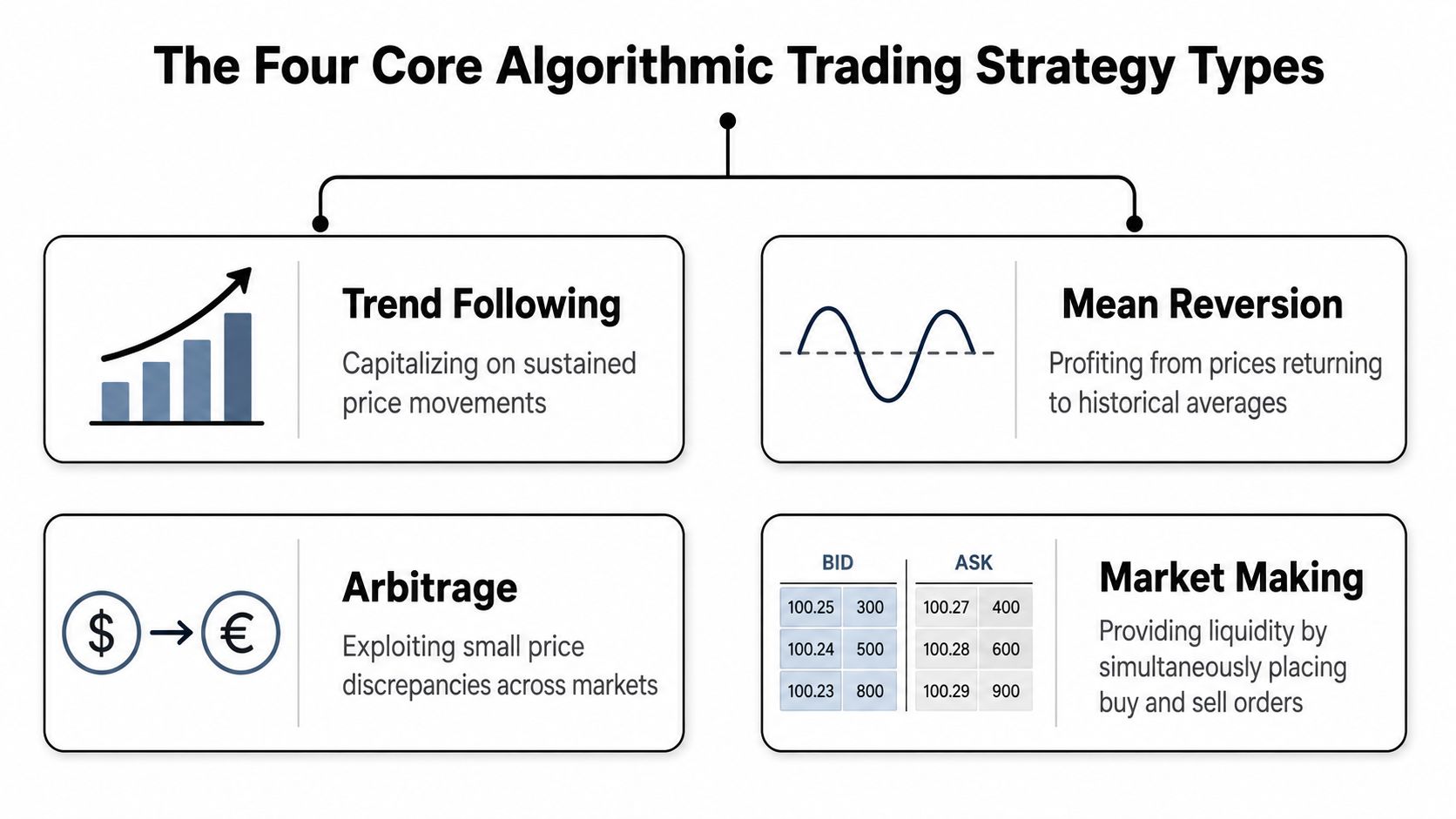

The Four Core Algorithmic Trading Strategy Types

Most systems fall into four buckets. If you don't know which one you're building, you'll mix incompatible ideas and end up with a strategy that behaves differently every month.

Trend following

Trend following assumes price can keep moving in the same direction longer than most traders expect. The goal isn't to buy the exact low or sell the exact high. The goal is to catch the middle of the move and avoid fighting strength.

A practical FX example is a setup where the daily trend and the 4-hour trend must both point the same way before entry on pairs like EURUSD or USDJPY, which helps cut down on whipsaws by forcing multi-timeframe confirmation (trend-following setup example).

This type works best when markets trend cleanly. It struggles when price chops inside a range and reverses before follow-through develops.

Mean reversion

Mean reversion assumes short-term moves often stretch too far, then snap back toward a normal range or average. These systems usually buy weakness in a stable structure or fade strength after an overextended move.

This style can work well in range-bound conditions. It can fail badly when a move that looks “too far” is the start of a new trend. That's why mean reversion systems need strict stop logic. A cheap-looking market can get much cheaper.

A lot of beginners pick mean reversion because entries feel smart. The problem is that fading strong moves feels smart right up until trend day starts.

Statistical arbitrage

Stat arb looks for temporary dislocations between related instruments. The logic is relative, not directional. You're not saying one market must rise. You're saying two related markets moved out of line and may realign.

This approach usually demands stronger data handling, cleaner execution, and more validation than retail traders expect. If your data prep is sloppy, your “edge” is often just noise.

Market making

Market making tries to earn the spread by posting bids and offers and managing inventory risk. In theory, it sounds attractive because you're harvesting micro-opportunities repeatedly.

In practice, this is one of the hardest styles for independent traders to execute well. Speed, queue position, platform behavior, and adverse selection matter a lot. You can collect small spreads for hours, then give it back fast when price moves through your quotes.

Algorithmic Strategy Types at a Glance

| Strategy Type | Core Principle | Ideal Market Condition | Key Risk |

|---|---|---|---|

| Trend Following | Trade in the direction of sustained price movement | Trending markets | Whipsaws in choppy conditions |

| Mean Reversion | Trade the move back toward an average or range | Range-bound markets | Catching a real breakout too early |

| Statistical Arbitrage | Exploit temporary dislocations between related assets | Relative mispricing environments | False relationships and noisy data |

| Market Making | Earn spread while providing liquidity | Liquid, active markets | Adverse selection and execution risk |

If you want a broader view of how traders structure these systems in practice, this guide on strategies for algo trading is a useful companion.

Your Development Workflow From Idea to Live Trading

Most weak algos fail before they ever go live. The trader skips structure, overfits the backtest, and mistakes a clean equity curve for a durable edge.

A workable process is slower than generally desired. That's a good thing.

Start with a narrow hypothesis

Don't begin with “build a profitable bot.” Begin with one trade idea.

Examples of usable hypotheses:

- Breakout logic: Price expansion after compression may continue during active sessions.

- Pullback logic: Trend pullbacks into structure may resume if momentum stabilizes.

- Relative value logic: Two related instruments may revert after temporary divergence.

The hypothesis has to be simple enough to test and strict enough to code.

Build on data you trust

Bad data ruins good research. Before you test anything, clean the series, align timestamps, and make sure your price history matches the market you plan to trade.

For U.S. equities, adjusted data matters because splits and dividends can distort results. For intraday systems, bar construction, spread assumptions, and session boundaries matter more than most beginners realize.

If you're designing the broader software stack around the strategy, not just the signal logic, it helps to study how teams approach fintech development strategies, especially around architecture, reliability, and deployment discipline.

Backtest for robustness, not beauty

A backtest is useful only if it survives contact with reality. You should aim for at least 100–200 independent trades across multiple market regimes, and realistic slippage plus brokerage costs can cut apparent Sharpe ratios by 0.2–0.5 points or more (robust backtesting guidance).

That changes how you should read results.

A backtest checklist worth following

- Trade count first: If the sample is thin, the metrics are fragile.

- Use multiple regimes: Bull, bear, and sideways behavior all matter.

- Model costs explicitly: Spread, slippage, and commissions must be included.

- Stress the assumptions: Shift entries, widen spreads, and test tougher fills.

- Reject brittle parameter sets: If small tweaks destroy performance, the edge is weak.

The cleanest equity curve is often the most dangerous one. Real strategies usually look rougher because real execution has friction.

Walk forward, then paper trade

Optimization isn't the same as validation. Once you tune the strategy, test it on unseen periods. Then run it in a demo or paper environment with live market flow.

That stage exposes issues a backtest hides:

- Signal timing mismatches

- Order rejections

- Unexpected platform behavior

- Different fills during volatile periods

For traders moving from research into deployment, this primer on how to trade with algorithms gives a practical overview of what changes once a strategy leaves the notebook and enters a live platform.

Evaluating Performance with Key Metrics and Risk Controls

A strategy isn't good because it made money in a test. It's good if it can survive losses, fit the account constraints, and behave predictably when execution gets messy.

That means you need metrics that answer operational questions, not just ego questions.

The metrics that matter in practice

Maximum drawdown

For a prop-style trader, this is the first metric to respect. If the strategy routinely suffers deep equity dips, the rest barely matters. A system can be profitable over time and still be unusable if its path to returns violates the account's limits.

Sharpe ratio and Sortino ratio

These help compare return quality, not just raw outcome. Sharpe looks at return relative to total volatility. Sortino focuses more on downside volatility.

Neither metric should be read in isolation. A high ratio built on unrealistic fills or tiny sample size is still junk.

Profit factor

This tells you whether gross profits outweigh gross losses by a useful margin. It's a decent health check, but it can hide ugly behavior if a strategy wins often and occasionally takes a damaging loss.

Risk controls belong in the code

You don't bolt on risk management at the end. You write it into the strategy logic from day one.

A practical control stack includes:

- Hard stop logic: Every trade needs a predefined invalidation point.

- Position sizing rules: Size should respond to account risk, not trader confidence.

- Session filters: Some systems should avoid thin liquidity or event-heavy windows.

- Trade frequency caps: Prevent revenge behavior in automated form.

- Kill-switch conditions: Shut the system down when behavior leaves expected bounds.

Good research asks, “Can this make money?” Good risk control asks, “Can this account survive the bad week?”

If you're thinking about building a career around systematic trading, browsing firms hiring in the space can sharpen your standards. These Valgorithm jobs on LatoJobs give a sense of how serious teams think about quant research, engineering, and execution quality.

Execution Slippage and Choosing the Right Platform

Execution is where many promising systems falter. The signal logic may be fine. The live results still disappoint because the platform, feed, or order handling doesn't match the assumptions in testing.

Slippage is the gap between the price your model expects and the price you receive. Sometimes that gap is small. Sometimes it changes the whole expectancy of the system.

Why slippage shows up

Common causes include:

- Latency: Your order reaches the market later than your model assumes.

- Liquidity gaps: The displayed price may not have enough size behind it.

- Fast conditions: News and session opens can move price before the order fills.

- Order type mismatch: Market, limit, and stop orders all behave differently under stress.

A slow swing strategy can tolerate some slippage. A short-horizon system usually can't. The shorter the holding period, the more execution details dominate the result.

Platform choice changes strategy viability

Not every platform is equal for every style.

If you're comparing environments such as cTrader, DXtrade, and MT5 when it's available to you, focus on practical questions:

- API access: Can you automate cleanly, or are you forcing awkward workarounds?

- Order handling: How predictable are fills and rejections?

- Data quality: Does the feed match the market behavior you tested on?

- Monitoring tools: Can you track logs, latency, and failed actions quickly?

- Broker or firm rules: Does the environment support your specific algo style?

A basic trend system may run acceptably on several platforms. A latency-sensitive scalper may behave like a completely different strategy depending on platform architecture.

For a deeper breakdown of the issue itself, this article on what slippage is in trading is worth reviewing before you trust any live expectancy number.

What works better than optimism

Use these habits:

- Paper trade on the target platform: Don't assume platform behavior is interchangeable.

- Log every fill: Compare expected entry, actual fill, and market state.

- Segment by session: London open behavior won't look like late U.S. afternoon.

- Avoid fragile edges: If a strategy needs perfect fills, it isn't resilient enough.

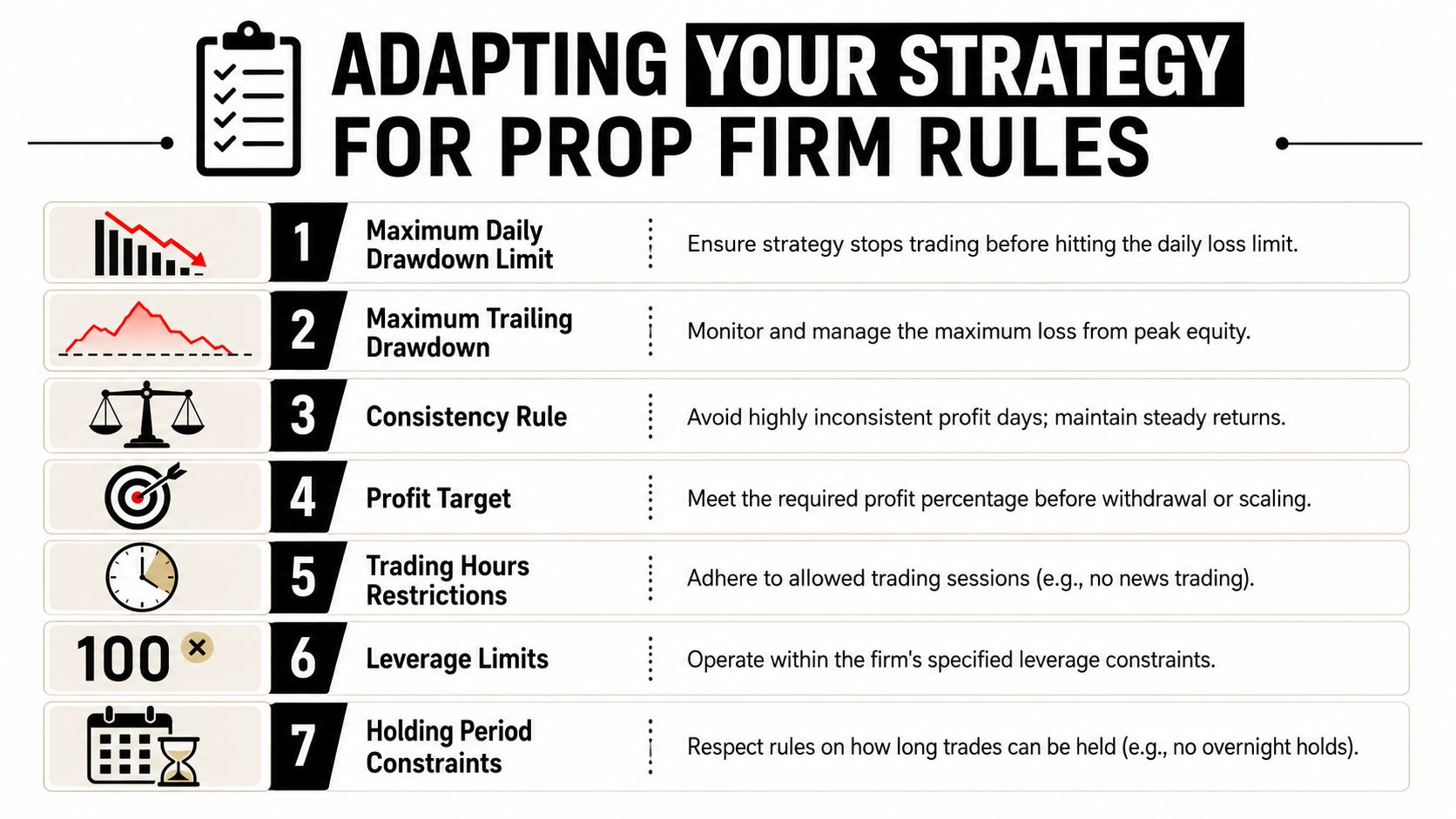

How to Adapt Your Strategy for Prop Firm Rules

A profitable algorithm that breaks the account rules is not a good algorithm. It's just non-compliant code.

That's the gap many traders miss. They build for maximum return, then try to force the strategy into a funded environment later. That usually ends with a breach, not a payout.

The prop constraint changes the design brief

Independent research shows that 30–40% of retail algorithmic strategies degrade or fail out-of-sample within 6–12 months, and practical guidance on adapting them to prop-style limits such as a flat 5% daily loss is still underdeveloped.

That matters because a funded account is a rule environment first and a trading environment second. Your algo has to survive both.

Build a master risk layer above the setup logic

Your entry model should not be the final authority. Add a separate risk engine that can override everything.

That master layer should monitor:

- Current daily loss status

- Distance to maximum drawdown

- Open exposure across correlated positions

- Time-based restrictions

- Trade count and loss streak behavior

When thresholds are approached, the master layer should reduce size, block new entries, or flatten the book.

If your strategy can keep trading after it has already proven it's out of control for the day, your automation is incomplete.

What prop-ready code usually includes

Daily stop logic

If the account has a hard daily limit, the algorithm should stop before the platform forces the issue. Don't aim to trade right up to the boundary.

Drawdown-aware sizing

Static size is often too crude. If equity drops, the strategy should automatically reduce exposure. The account needs room to recover.

Exposure clustering controls

Many traders think they have diversification because they opened several symbols. In FX and CFDs, those positions can still express the same underlying bet. The risk engine should cap related exposure.

Session and event filters

Some systems shouldn't trade around major scheduled releases, thin rollover periods, or restricted holding windows. That logic belongs in the code, not in your memory.

A compliance checklist for the live account

Use this before deployment:

- Can the algo disable itself for the rest of the day after hitting its internal loss threshold?

- Can it flatten all open trades if account equity approaches the hard limit?

- Can it block duplicate exposure across highly related instruments?

- Can it adapt position size after drawdown, not just after gains?

- Can it respect trading-hour, news, or holding restrictions automatically?

- Can you audit every action through logs after a bad session?

One practical route is to deploy on an environment that already supports algorithmic and EA-based trading under clear rules. MyFundedCapital supports algorithmic trading on DXtrade and cTrader, with stated parameters including a flat 5% daily loss limit and up to 10% maximum drawdown, which makes it easier to design the risk layer around known constraints rather than vague policy language.

Your Next Steps in Algorithmic Trading

Start smaller than you want to. That's usually the right move.

Take one setup you already trade manually and convert it into explicit rules. Test it on clean historical data. Reject weak samples. Add risk controls before you even think about improving returns. Then run it in paper trading long enough to see how it behaves when the market is live and annoying.

Keep your expectations realistic. Strategies decay. Conditions change. Execution frictions show up late. The traders who last in this space don't chase the fanciest model. They build systems they can monitor, challenge, pause, and rewrite without denial.

Use this roadmap as a working process:

- Pick one strategy type

- Write plain-language rules

- Backtest with realistic assumptions

- Add a master risk layer

- Paper trade on the target platform

- Go live with controlled exposure

This is educational only, not financial advice. Trading involves risk of loss, and no algorithm removes that.

Frequently Asked Questions About Algorithmic Strategies

Can I use a commercial EA instead of building my own?

Yes, but treat it like borrowed code, not a finished business. You still need to understand the entry logic, exit behavior, risk settings, and where it tends to break. If you can't explain what the EA is doing, you can't manage it properly.

Do I need to know programming to build an algorithmic trading strategy?

Not always. Some traders start with visual builders or existing frameworks. Still, even if you don't write every line yourself, you need enough technical understanding to validate rules, inspect logs, and catch execution problems. Otherwise you're operating blind.

What happens if my algorithm breaks prop firm risk rules?

Usually, the account fails the rule set. That's why manual oversight isn't enough. Your algo should enforce internal limits before the account reaches the firm's hard limits. A strategy that depends on you stepping in at the last second isn't automated in any meaningful sense.

How often should I review a live strategy?

Regularly, but not emotionally. Review fills, drawdown behavior, missed signals, and rule adherence. Don't rewrite the system after every rough patch. Review with a process. If performance deterioration becomes persistent, pause the strategy and re-validate it instead of hoping it will snap back.

If you're ready to test your system in a rule-based funded environment, explore MyFundedCapital to compare account types, review risk parameters, and start a challenge that fits your trading style.