Your first prop firm payout feels great until the tax reality hits. Money arrives, no tax is withheld, and suddenly you have to figure out whether this is business income, capital gains, self-employment income, or something else.

That confusion is common. Prop firm taxes don't work like a normal job or a personal brokerage account, and if you handle them the wrong way, the mistakes can get expensive fast. Trading also involves risk of loss, and managing taxes is part of treating trading like a real business. This article is educational only, not financial or tax advice.

Your First Prop Firm Payout and the Tax Questions That Follow

You pass an evaluation, start trading well, and then your first payout lands. The first thought is usually relief. The second is often, “Do I owe tax on this right now?”

For many traders, that first payment is the moment prop trading stops feeling like a side experiment and starts feeling like a business. No payroll department steps in. No one withholds tax for you. The number you see in your payout portal is not the number you should mentally treat as spendable cash.

A lot of traders freeze at the same set of questions:

- Is this taxed like trading gains? Many assume it works like profits in a personal account.

- What if the firm pays in crypto? Traders often think the payment method changes the tax result.

- What if I leave the money in the ecosystem? That can still create a tax issue.

- Do challenge fees count for anything? In many cases, they may matter as business expenses.

If you're trying to optimise your tax as a contractor, that contractor mindset is the right starting point for prop trading too. The most useful shift is to stop thinking like an investor and start thinking like a self-employed person getting paid for performance.

One more practical issue catches people out. Firms often explain profit splits and withdrawal rules clearly, but traders don't always connect those rules to taxes. If you want to understand how payout mechanics usually work before looking at the tax side, review a typical prop firm profit split structure.

Treat your first payout like business revenue, not bonus money.

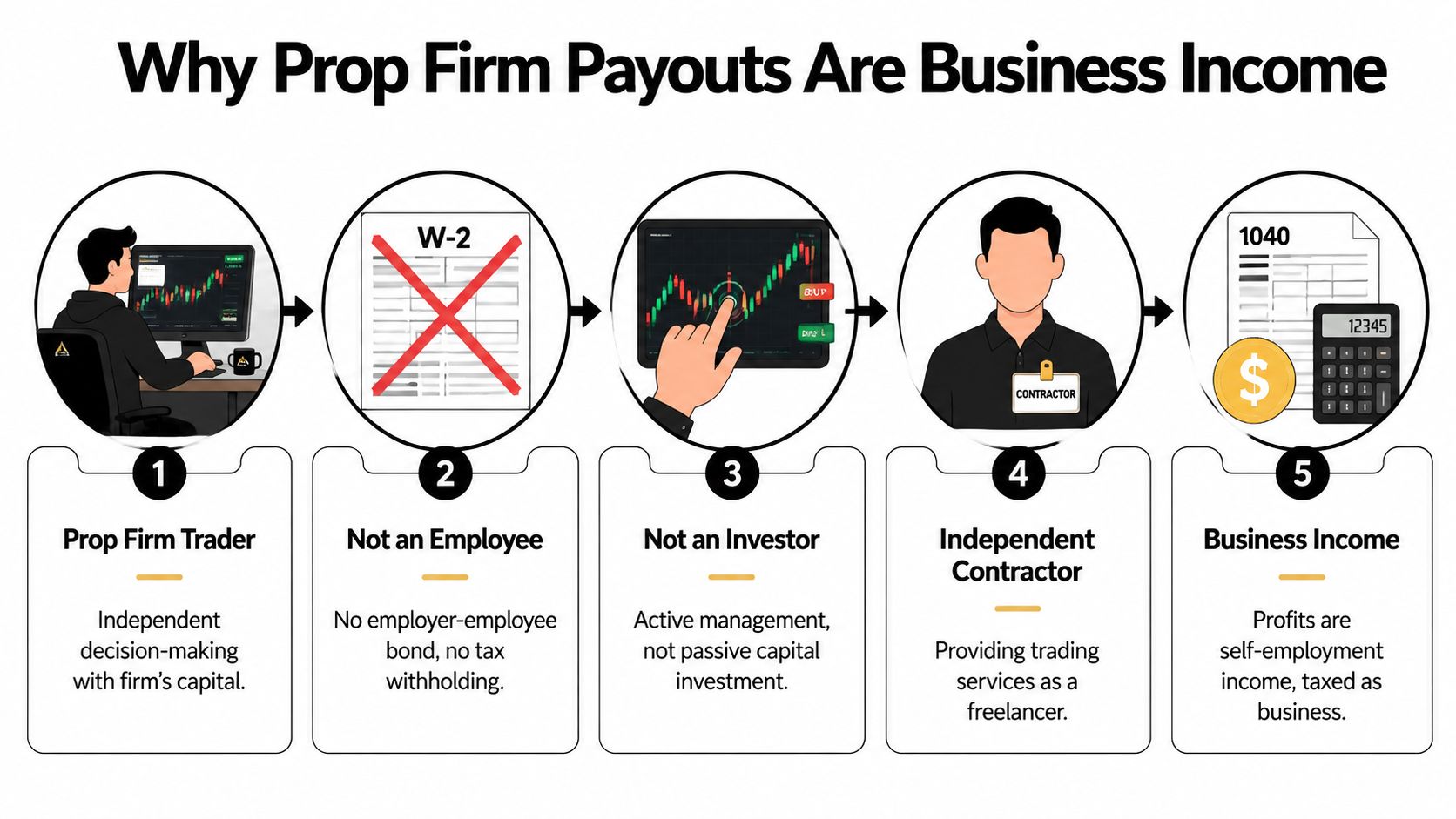

Why Prop Firm Payouts Are Taxed as Business Income

The cleanest way to understand prop firm taxes is this. Think of yourself as a freelance consultant. You aren't investing your own capital in the usual sense, and you aren't an employee on payroll. You're providing trading performance to a firm under a contract and getting paid a share of the result.

That is why prop firm payouts are generally treated as business income or ordinary income, not capital gains.

The three labels traders get wrong

Traders usually misclassify prop income in one of three ways.

Employee income

That doesn't fit because the firm usually isn't hiring you as staff, withholding payroll tax, or treating you like a W-2 employee.Capital gains That also usually doesn't fit because you're not investing your own money and reporting the gain on a personal asset sale. You're performing under a business arrangement.

Business income This is the label that usually matches the actual setup. You're operating independently and receiving a payout for your trading activity.

A broader explanation of how these firms operate can help if you're still sorting out the legal relationship involved in funded trading. This overview of what proprietary trading firms are and how they work is useful background.

Why the IRS cares about control, not just withdrawal

One of the biggest tax traps is constructive receipt. Many traders assume taxes apply only when money reaches their bank. That's not always how it works.

Greentrader Tax warns that many traders think tax is due only on withdrawn payouts, but under IRS constructive receipt rules, credited profits can be taxable when they're available for withdrawal, even if the trader reinvests them or never receives a 1099. The same source notes that “prop traders are likely under-reporting income” for that reason in this discussion of under-reported prop firm income.

That point matters in modern prop trading because firms often let you:

- leave funds sitting in an internal wallet

- request payout later

- scale into a larger account

- receive payment by bank transfer, processor, or crypto

None of those options automatically delays taxation if the money was already credited and available to you.

If the payout is available for you to take, the tax issue may already exist.

A simple way to think about it

Ask one question: Was the money made available to me under my contract?

If the answer is yes, don't assume waiting to withdraw fixes anything. That's where traders get into trouble. They look at the bank statement instead of the payout record.

This is also why keeping records matters so much. Save payout confirmations, dashboard screenshots, invoices, crypto payment records, and any email showing when funds became available. Those records help you report the income correctly and explain timing if a tax professional reviews your file later.

Reporting Income and Paying Taxes in the United States

You get your first payout, the money hits your account, and the next question is immediate. Do I wait for a tax form, or do I need to report this now?

For U.S. traders, the answer is usually straightforward. Prop firm income is generally reported as business income. A useful comparison is freelance consulting. The firm is not treating you like an employee with payroll withholding. You are usually the one responsible for tracking income, setting money aside, and paying tax during the year.

The IRS explains in its Instructions for Schedule C that sole proprietors use Schedule C to report income and expenses from a trade or business. For many prop traders, that is the practical starting point. You report the payouts, subtract any deductible business expenses, and calculate net profit.

What forms usually matter

For most U.S. prop traders, the paperwork centers on three items:

- Form 1099-NEC if a firm issues one for nonemployee compensation

- Schedule C on Form 1040 to report your business income and expenses

- Form 1040-ES to make estimated tax payments during the year

Remember: you must report the income even if no form arrives. Traders get in trouble when they assume the reporting duty starts only after a 1099 shows up. The IRS does not use that rule.

What taxes you are usually paying

Two tax systems often apply at the same time:

- Federal income tax, based on your total taxable income and filing status

- Self-employment tax, which applies to net earnings from self-employment

The IRS discusses self-employment tax in its Self-Employed Individuals Tax Center, including the general rule that self-employed people may need to make estimated tax payments and may owe self-employment tax on net earnings.

State tax may also apply. That part depends on where you live and, in some cases, where your business activity is considered to occur.

This catches many traders off guard. At a regular job, withholding happens in the background. With prop firm payouts, you are handling the withholding job yourself.

A practical way to estimate the damage before it happens

Treat each payout as partly yours and partly the IRS's. If you receive $2,500 and spend all $2,500, you can create a cash problem long before tax season arrives.

A safer habit is to move part of every payout into a separate tax savings account as soon as you receive it. The exact percentage depends on your bracket, your state, and your deductions. Many traders use a rough reserve percentage during the year, then true it up with their CPA or tax preparer as income becomes clearer.

If your prop firm pays you through PayPal, Deel, Wise, bank wire, or crypto, the reporting rule does not change just because the payment rail changed. Business income is still business income. Crypto adds a second layer of recordkeeping. You need the fair market value when you received it, and you also need to track any later gain or loss if you keep the coins and they change in value.

Estimated tax payments usually matter

The IRS expects tax to be paid during the year, not only when you file the return. Its Estimated Taxes page explains who generally needs to pay estimated tax and how the system works.

A simple routine helps:

- Track each payout and the date it became available

- Convert any crypto payout to its U.S. dollar value on the receipt date

- Total income and expenses regularly

- Estimate tax before each quarterly deadline

- Pay through IRS Direct Pay, EFTPS, or another approved method

Quarterly payments are where small mistakes turn expensive. Miss the timing, and you may owe penalties even if you pay the full balance with your return later.

Common reporting mistakes

A few errors show up again and again:

- Reporting only what hit your bank account, instead of what was paid or made available to you

- Ignoring foreign or offshore firm payouts, as if a non-U.S. firm changes U.S. taxability

- Failing to document crypto withdrawals, including value on the day received

- Waiting for a 1099 before building your records

- Mixing personal and trading business transactions in one account with no paper trail

Good records solve most of this. Save payout confirmations, invoices, exchange-rate screenshots for crypto receipts, wallet transaction IDs, and account statements. If the IRS ever asks how you calculated income, those records are your map.

How to Legally Reduce Your Prop Firm Tax Bill

If prop trading income is business income, then you need to think like a business owner. That doesn't mean chasing aggressive write-offs. It means claiming ordinary, necessary expenses that are connected to your trading activity and keeping clean records.

A helpful benchmark comes from this article on prop firm tax deductions, which says U.S. prop traders report payouts on Schedule C and face a 15.3% self-employment tax plus income taxes. The same source notes that deducting expenses like DXtrade or cTrader subscriptions, VPS hosting, and challenge fees can reduce taxable net income by 20-40%. It also gives an example where a trader deducting $20,000 in expenses on $100,000 gross income lowers the self-employment tax base to $80,000, saving about $3,000.

Expenses traders often overlook

Some deductions are obvious. Others get missed because traders don't think of themselves as running a business.

Challenge and evaluation fees

These are often the first expense traders forget. If they're part of your trading business activity, they may be relevant deductions.Platform costs

DXtrade and cTrader fees can matter if you're paying for access tied to your trading business.VPS hosting

If you run EAs or need stable execution infrastructure, VPS costs may be part of the business.Data, software, and tools

Charting packages, trade journals, and market research tools may qualify if they directly support the activity.Home office costs

If you use a dedicated workspace for your trading business, this area may be worth reviewing with a tax professional.

A trader exploring legal ways to lower taxable income in another business context can also learn from broader small-business tax habits, such as careful expense tracking and separation of personal and business spending. This guide on minimizing taxable income for property investors isn't about prop trading specifically, but the record-keeping mindset is similar.

Your deduction checklist

Use a simple folder system. One folder per tax year, then subfolders for each expense type.

Keep these records

- Receipts and invoices for challenge fees, software, and subscriptions

- Bank and card statements showing actual payment

- Platform records from DXtrade, cTrader, or related tools

- Crypto transaction records if you paid fees or received payouts that way

- Notes on business purpose when an expense might not be obvious at first glance

If you're trading instruments such as forex or futures under prop firm structures, it's even more important to keep your product costs and trading-business costs separate. A market overview like forex and futures trading differences can help you sort operational categories, but your bookkeeping still needs to show what was paid and why.

The mistake that ruins good deductions

Poor documentation.

A deduction isn't just about whether the expense feels related. You need to show:

- what you paid

- when you paid it

- who you paid

- why it was connected to the business

That standard matters more in prop trading because the activity sits in a category many tax preparers still misunderstand. If your records are messy, they may default to conservative treatment or miss legitimate deductions entirely.

Good records don't just lower tax. They make your return defensible.

Advanced Status and Global Tax Rules

Some traders outgrow the basic “report it on Schedule C” conversation and start asking harder questions. Can a U.S. trader qualify for Trader Tax Status? Does a crypto payout change anything? What if the firm is overseas?

The broad answer is that the business income logic stays surprisingly consistent across borders, even though local forms and compliance rules differ.

Default treatment versus advanced trader treatment

In the U.S., the default setup for many funded traders is business income reported as self-employment income. Some active traders also look into Trader Tax Status, often shortened to TTS.

TTS is a more specialized tax position. The main reason traders care about it is the possibility of electing mark-to-market treatment under Section 475(f), which can help with wash sale issues. But this is not a casual election. It usually depends on substantial, continuous, regular trading activity, and it deserves professional review before filing.

For many funded traders, the practical order is:

| Status path | General idea | Main tax focus |

|---|---|---|

| Default business trader | Report prop firm income as business income | Correct reporting, deductions, estimated taxes |

| Trader Tax Status candidate | More advanced U.S. trader treatment | Eligibility, elections, wash sale implications |

The mistake is chasing advanced status before you've nailed the basics. If your bookkeeping is weak, your payout records are incomplete, or your quarterly taxes are late, TTS isn't the first problem to solve.

Global treatment is more alike than different

According to this global guide to prop firm tax treatment, prop firm income is generally treated as business income, not capital gains. The same source states that in the U.S. it is reported on Schedule C, in Australia the ATO taxes it at marginal rates plus a 2% Medicare Levy, and in the UK it is treated as self-employed income via SA100 with National Insurance contributions. The source also notes that this professional classification rarely allows favorable treatment such as the 60/40 blend for Section 1256 futures contracts.

Here is the high-level comparison.

Prop firm tax treatment in key countries

| Country | Income classification | Key tax form/process | Common rate structure |

|---|---|---|---|

| United States | Business or ordinary income | Schedule C | Income tax plus 15.3% self-employment tax |

| Australia | Business income | ATO self-employed reporting process | Marginal rates plus 2% Medicare Levy |

| United Kingdom | Self-employed income | SA100 | Income tax plus National Insurance contributions |

Overseas firms and crypto payouts

Two modern prop trading realities create confusion.

First, many firms operate internationally and may not issue a local tax form to every trader. That doesn't remove your reporting obligation. If you received the income, you still need records that show the amount, date, and method of payment.

Second, crypto payouts don't change the character of the income. If you receive your prop split in crypto, the tax authority usually still looks first at why you were paid, not just how you were paid. The payout is still business income. After that, a separate tax issue may arise later if the crypto changes value between receipt and sale.

Frequently Asked Questions About Prop Firm Taxes

Are failed challenge fees deductible

They may be, if they're part of your trading business activity and you can support the expense with good records. The key is treating the activity consistently as a business and keeping receipts, payment records, and account history. If you have a mix of personal trading, education spending, and prop evaluations, keep those categories separate so your records stay clear.

What if my prop firm is overseas and doesn't send a tax form

You still need to report the income. A missing form doesn't make the payout non-taxable.

Use your own records:

- Payout dashboard history

- Bank statements

- Crypto wallet records

- Email confirmations

- Invoices or payment summaries

If the firm pays in multiple methods during the year, keep one master spreadsheet showing each credited payout and each actual receipt.

Do I owe tax only when I withdraw the money

Not always. As covered earlier, constructive receipt is the issue. If the money was credited and available for you to withdraw, there may already be a tax event even if you left it with the firm or rolled it into a larger account.

This is one of the most common prop firm taxes mistakes because traders focus on cash movement rather than control over the payout.

The payout date in your dashboard may matter more than the date money hits your personal account.

Does getting paid in crypto make it capital gains instead of business income

No. The payment method doesn't usually change the underlying nature of the payout. If the payment is compensation from your funded trading activity, it is still generally business income first.

Then a second layer can appear later. If you hold the crypto after receiving it and its value changes before you sell or convert it, that later change may create a separate tax consequence. That's why it's important to record the value at receipt and keep the wallet transaction history.

Key Takeaways and Your Next Steps

Your first payout is usually the moment funded trading stops feeling like a game and starts looking like a business. The professional response is simple: set up a tax process before the second payout arrives. Treat each payment like client revenue, whether it lands by bank transfer, Deel, Wise, or crypto. Record the amount and date it was credited, save the proof, separate business expenses such as challenge fees and trading tools, and reserve part of each payout for taxes so estimated payments do not become a surprise.

Professional traders distinguish themselves from amateurs by more than just strategy. The distinction lies in how they manage the results of a profitable month. While an amateur treats a payout as spendable cash, a professional immediately identifies three categories: operating capital, taxes, and personal income. This habit is especially vital with prop firms because the details often become complex. One firm may pay through a contractor platform, another may use crypto, and a third may credit a payout before it is withdrawn. If your records are weak, small mistakes can turn into expensive ones.

Start with a repeatable system this week. Open a separate account for tax savings. Build one spreadsheet that tracks credited payouts, actual receipts, payment method, fees, and related deductions. If you receive crypto, log the value when you receive it and keep the wallet history. If your situation includes an LLC, Trader Tax Status questions, foreign residency, or cross-border payouts, get advice from a tax professional who works with traders and self-employed income, not just general tax returns.

Trading has risk, and taxes are part of the cost structure. This article is educational only and not financial or tax advice.

If you're ready to approach funded trading like a professional, explore MyFundedCapital to compare funding programs, review account types, and choose the challenge path that fits your trading style.