You're probably looking at algo trading in forex from one of two places. Either you're tired of missing entries, breaking your own rules, and watching manual execution ruin decent ideas, or you've already tested a bot and learned that a good backtest doesn't automatically survive live conditions.

That's the primary gap. Most guides explain indicators and robot setup. Fewer explain what is essential when you want to run automated systems under prop firm rules, with real execution friction, strict risk limits, and no room for sloppy infrastructure. This article is educational only and not financial advice. Trading involves risk of loss.

What Exactly Is Algo Trading in Forex

Algo trading in forex means using software to follow predefined rules for entries, exits, position management, and risk controls. Instead of deciding trade by trade, you turn your logic into instructions a system can execute consistently.

For newer traders, that sounds like “a bot that trades for me.” That's partly true, but it misses the point. The key advantage is not automation for its own sake. Instead, its primary benefit is rule enforcement.

A manual trader can know the setup and still hesitate. A manual trader can also overtrade, move stops, skip signals, or get distracted during London or New York session moves. An algorithm doesn't fix a bad strategy, but it does remove a lot of the inconsistency that comes from fatigue, fear, and impulse.

A 2019 study found that approximately 92% of all trading in the Forex market was performed by algorithms, not humans, according to this forex algo trading overview from Investing.com. That matters because it tells you algo trading isn't some niche side topic. It's part of the market's structure.

What the algo actually does

At the simplest level, a forex algorithm handles four jobs:

- Signal detection. It checks whether market conditions match your rules.

- Order execution. It sends orders without hesitation when conditions are met.

- Trade management. It applies stops, targets, trailing logic, or time-based exits.

- Risk control. It can restrict size, daily activity, or trading during certain conditions.

That's why good automation often starts with simple logic. If your setup can't be explained clearly, it usually can't be automated well either.

Practical rule: If you can't write your trading idea as a strict checklist, you probably can't trust a bot to trade it.

What changes for the trader

Your role shifts. You stop acting mainly as the clicker and start acting more like a system designer, tester, and supervisor.

That means your work becomes:

- refining rules

- checking fills

- reviewing drawdown behavior

- watching for regime change

- deciding when to pause or retire a model

This is also why general reading on strategies for automation in finance can be useful. The same operational logic applies across finance: automation works best when the process is clear, repeatable, and monitored.

A lot of beginners think automation means less work. In practice, it means different work. Less emotional clicking. More design, testing, monitoring, and discipline.

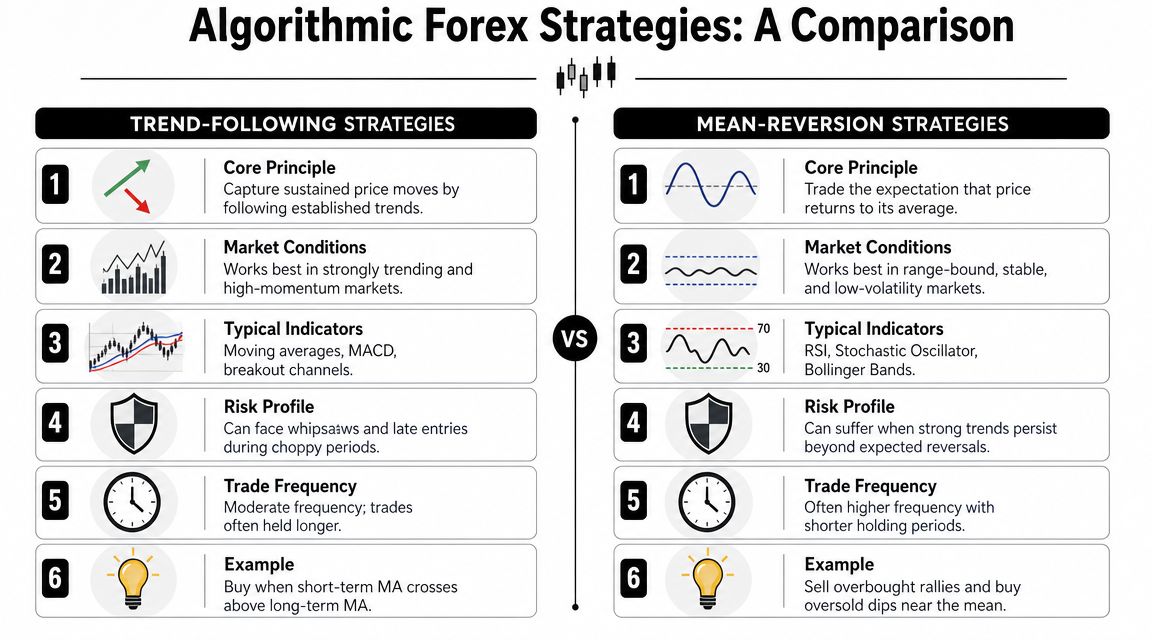

Core Algorithmic Forex Strategies Explained

Two dominant algorithmic approaches in forex are trend-following and mean-reversion. The true skill is not memorizing the labels. It is knowing how each one behaves in live conditions, where fills vary, spreads widen, and prop firm risk limits can force you to cut a system before its long-term edge has time to show.

A clean backtest can make both styles look easy. Live deployment usually exposes the difference. One style absorbs frequent small losses while waiting for expansion. The other collects many small wins but can take sharp damage when price stops respecting a range.

Trend-following systems

Trend-following systems try to participate in directional moves that persist long enough to cover several failed entries and still leave a net gain. In forex, that often means catching momentum after a breakout, a volatility expansion, or a higher-timeframe directional shift.

Common building blocks include:

- Moving-average crossovers for directional bias

- ADX filters to avoid flat conditions

- Donchian breakouts to enter after consolidation resolves

The trade-off is straightforward. These systems are usually uncomfortable to trade because they spend a lot of time being early, slightly wrong, or stopped out before the main move begins. Newer traders often abandon them after a cluster of small losses, even though that rough equity curve is normal for the style.

They also need room to breathe. In a prop firm environment, that matters. If the account has tight daily drawdown rules, a trend model that needs several attempts to catch one clean move can be harder to run than the backtest suggests.

Mean-reversion systems

Mean-reversion systems bet on short-term overextension snapping back toward a recent average. They are common in quieter sessions, inside established ranges, or after fast one-sided moves that look stretched relative to recent volatility.

Typical building blocks include:

- RSI or other oscillator extremes

- support and resistance fades

- short-term volatility contraction

- reversion entries around statistically stretched price moves

These systems often feel better at first because they can produce a smoother run of winners. That comfort is deceptive. A strong trend, a news-driven repricing, or a session handoff can turn a normal pullback entry into repeated losses very quickly.

This is why exit logic matters more than the entry idea. A mean-reversion bot without a hard invalidation rule is not conservative. It is just slow to admit it is wrong.

How to choose between them

Choose based on market behavior, execution quality, and account constraints.

If your broker or prop setup gives stable spreads and your strategy can tolerate a lower hit rate, trend-following can work well because the upside comes from a smaller number of outsized moves. If your model depends on frequent small wins, mean-reversion can work, but only if costs stay controlled and you have strict rules for shutting it down when conditions shift.

A simple comparison helps:

| Strategy type | Works best in | Typical weakness | Trader mistake |

|---|---|---|---|

| Trend-following | Expanding, directional markets | Repeated false starts | Stopping the system after normal losing streaks |

| Mean-reversion | Stable, range-bound markets | Sudden regime shifts | Holding and adding when price is no longer reverting |

In practice, many traders blend filters rather than blend logic. That distinction matters. A solid system might use a higher-timeframe trend filter, then apply a separate entry model only when the market structure fits. What usually fails is mixing incompatible assumptions in one rule set, such as buying breakouts but managing exits as if price will immediately revert.

For a more practical look at algo trading strategy ideas for funded accounts, study how strategy style interacts with platform rules, consistency targets, and drawdown limits. Traders who want to uncover financial insights using AI can also use dashboards to review regime changes, trade clustering, and whether a model is making money from actual edge or from a short-lived market condition.

That is the part generic strategy guides usually skip. In a prop firm setting like MyFundedCapital, the best strategy on paper is not always the best one to deploy. The better choice is often the model whose drawdown profile, trade frequency, and execution demands fit the rules of the account.

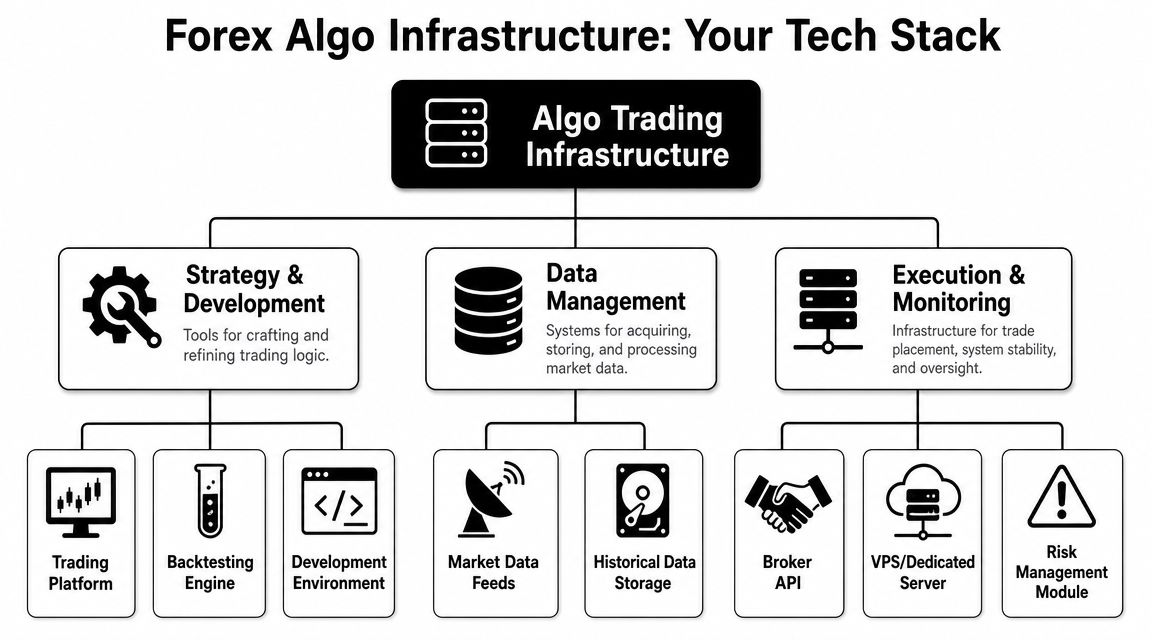

The Essential Infrastructure for Your Forex Algo

A forex algo doesn't live inside a backtest report. It lives in a stack of tools that has to work every day, under load, during volatile sessions, without breaking when you're asleep. Infrastructure is where many decent systems fail unnoticed.

A typical production setup often includes MetaTrader 5 or a Python-based system hosted on a low-latency VPS, because order speed and uptime matter in live deployment, as outlined in this overview of forex algorithmic trading software.

Layer one: strategy and development

The logic resides here.

You need:

- a platform or coding environment

- a backtesting engine

- a way to log decisions and errors

- version control, even if it's basic

Some traders start with MetaTrader because it's familiar. Others use Python to research and generate signals, then connect that logic to an execution layer. The right choice depends less on internet debates and more on your actual workflow.

If you want broader workflow ideas for research and monitoring, tools that uncover financial insights using AI can help structure analysis. They don't replace trading logic, but they can support review, reporting, and pattern detection.

Layer two: data management

Bad data creates fake confidence.

Your system depends on:

- historical data quality for testing

- live feed consistency for signal generation

- timestamp accuracy for execution review

If your backtest uses one data feed and your live environment behaves differently, your model can drift fast. Session opens, spread behavior, and candle formation can all change results.

A useful rule is simple: the shorter your timeframe, the less forgiving bad data becomes.

Layer three: execution and monitoring

This is the part traders ignore until it hurts them.

You need:

- a stable connection to the broker or platform

- a VPS or dedicated remote machine for uptime

- kill-switch logic

- alerts for order failures, disconnects, or abnormal behavior

If your internet drops, your laptop sleeps, or your platform freezes, the market won't pause for you. A home setup is fine for testing and supervision. It's weak for serious unattended execution.

Your edge doesn't come only from the signal. It comes from the signal reaching the market the way your research assumed it would.

For traders evaluating platform compatibility, NinjaTrader platform information can be helpful as part of the broader platform comparison process, even if your forex automation stack ends up centered on a different execution environment.

Backtesting and Validation Without The Hype

Backtesting is useful. It's also where traders lie to themselves without meaning to.

The wrong mindset is “prove this strategy will make money.” The better mindset is “try to disprove this strategy before live markets do it for me.” That change alone improves decision-making.

What backtesting is good for

A solid backtest can help you answer practical questions:

- Does the logic even hold up?

- How ugly is the drawdown behavior?

- Does performance depend on one narrow market phase?

- Do small rule changes destroy the result?

That last point matters a lot. Fragile systems often look great only at one exact setting. Resilient systems usually survive small changes in parameters without falling apart.

The overfitting trap

Overfitting happens when you tune a model too closely to the past. You keep adjusting entries, exits, filters, and time windows until the equity curve looks clean. The problem is that you didn't find a durable edge. You found a way to describe old noise very precisely.

That's why a beautiful report can be a warning sign.

Use a stricter process:

- Build simple rules first.

- Test on one sample.

- Hold back a separate out-of-sample period.

- Check whether the behavior still makes sense.

- Forward test before risking anything meaningful.

Why walk-forward thinking matters

Walk-forward analysis is one of the more practical ways to think about validation. Instead of optimizing once on all history, you repeatedly test how a strategy would have adapted over time. That gets you closer to live reality.

You don't need a fancy quant lab to benefit from the idea. The principle is what matters: research on one period, validate on another, then see whether the process still behaves sensibly as markets change.

A backtest should make you more skeptical, not more excited.

If your strategy only works with perfect fills, exact indicator settings, and no messy periods, it's probably not ready. In prop-style trading, that kind of fragility tends to show up fast.

Algo Trading with a Prop Firm MyFundedCapital

Running algo trading in forex inside a prop environment changes the design problem. You're no longer asking only, “Does this system have edge?” You're also asking, “Can this system survive firm rules, platform constraints, and evaluation pressure?”

That second question matters more than many traders realize.

What prop-ready design looks like

A prop-ready system usually has these characteristics:

- Controlled downside so one bad sequence doesn't break account rules

- Stable position sizing instead of aggressive recovery logic

- Clear shutdown conditions for bad market states

- Auditability so you know why the bot traded

- Platform fit so execution matches the environment you employ

Many off-the-shelf EAs often fail. They may be built for a personal account with wide tolerance for drawdown, loose execution oversight, or martingale-style recovery. That structure often clashes with funded account rules.

The risk rule problem

Per the publisher brief, MyFundedCapital uses a 5% daily loss limit and up to 10% maximum drawdown. Those numbers directly affect algo design.

A system that “usually recovers” is not good enough here. If it has clustered losses, position-size escalation, or no hard volatility filter, it can violate limits before the long-term edge has any chance to show up.

A useful review checklist looks like this:

| Area | What to check |

|---|---|

| Position sizing | Is size fixed or rule-based, or does it escalate after losses? |

| Daily risk | Can the system stop itself after a bad run? |

| Open exposure | Can correlated pairs create hidden concentration? |

| Session behavior | Does the bot behave differently around opens or news periods? |

| Logging | Can you review every action after the fact? |

Platform and rule fit

The practical side matters. A strategy built for one ecosystem may need changes before it runs cleanly on another.

For traders considering funded deployment, automated trading programs are worth reviewing because they frame what's allowed, how automation is handled, and what operational limits matter. In this kind of setup, supported environments such as DXtrade and cTrader matter because platform support affects how you route orders, monitor execution, and structure supervision.

The optional features in a prop environment also influence design. If weekend holding is allowed through an add-on, swing logic becomes more practical. If news trading permissions vary, event-sensitive strategies need explicit safeguards. These are not side details. They change how your algo should behave.

A practical build standard

If I were reviewing a forex bot for prop use, I'd want to see:

- a narrow and understandable strategy idea

- hard risk caps built into the logic

- no dependency on revenge sizing or averaging deeper into trouble

- evidence that live execution assumptions were considered

- a clear answer to this question: when should this bot stop trading?

That last part is often missing. Good algos don't just know when to enter. They know when conditions no longer justify participation.

Managing Execution Risk and Slippage

Execution is where a promising strategy gets exposed. You can have clean signals, decent logic, and sensible risk controls, then still underperform because your orders don't hit the market the way your tests assumed.

Recent FX commentary notes that algo trading now accounts for around 75% of spot FX volume, and that the focus has shifted toward execution quality, as discussed in this BNP Paribas market commentary on FX algorithmic trading. That's the practical reality. In a heavily automated market, weak execution is a direct disadvantage.

What slippage and latency actually mean

Latency is the delay between your system deciding to trade and the order reaching the venue.

Slippage is the difference between the price you expected and the price you got filled at.

Those two problems don't hit every strategy equally. A slower swing system may tolerate some execution noise. A short-term breakout bot can lose its edge quickly if entries arrive late or exits slip repeatedly.

What usually works better

A few habits help:

- Measure actual fills against intended prices

- Separate backtest assumptions from live reality

- Use order types deliberately instead of blindly favoring market orders

- Avoid pretending every session has the same liquidity conditions

- Track behavior around news and session transitions

There's always a trade-off. Market orders improve certainty of execution but can worsen price. Limit orders control price better but increase the chance of not getting filled. Neither is universally superior.

If you don't track slippage by setup, session, and market condition, you don't know your real strategy performance.

For prop traders, this is even more important. Tight risk rules don't leave much room for hidden execution drag. A strategy can remain “correct” in theory and still fail operationally because the live environment keeps shaving away the margin that made it viable.

Frequently Asked Questions and Final Takeaways

Can I just buy a commercial EA and use it?

You can, but that doesn't make it a good decision. If you don't understand the entry logic, risk model, and failure mode, you're outsourcing trust without any real control. Black-box systems are hardest to fix when performance changes.

What's the best programming language for a beginner?

The best one is usually the one that matches your platform and lets you test ideas clearly. Some traders start with platform-native tools. Others prefer Python for research because it's flexible and easier to extend.

Is forex arbitrage still viable for retail traders?

Mostly not in the pure form people imagine. As explained in this algorithmic trading guide from Axiory, pure arbitrage opportunities in modern FX are rare and extremely short-lived due to institutional speed advantages. For most traders, automation is more useful for disciplined execution and risk control than for chasing textbook arbitrage.

What matters most in algo trading in forex?

Three things:

- A validated idea that survives more than one market condition

- Reliable infrastructure so live execution matches your assumptions closely enough

- Strict risk management so normal losing periods don't become account-ending events

That's the honest version of this business. You don't need a magical bot. You need a strategy with a clear edge, a stack that can run properly, and rules strong enough to survive your own bad habits.

If you want to apply that approach inside a funded environment, review the account options and funding paths at MyFundedCapital. Compare the challenge models, check platform support, and make sure your system fits the risk rules before you deploy.