Algorithmic trading uses computer programs to automatically execute trades based on a predefined set of rules, removing emotion and enabling high-speed execution. It moved from a specialist approach into mainstream market structure long ago, with estimates putting algorithmic trading at about 70% of U.S. securities-market activity by the end of 2009 and roughly 70% of U.S. equity trading by 2013.

You're probably here because manual trading has started to feel repetitive in the worst way. You scan charts, wait for setups, second-guess entries, miss clean signals, then take the messy one out of frustration.

That's where algorithmic trading starts to make sense.

Not because it's a shortcut, and definitely not because it prints money. It doesn't. What it does is turn a trading idea into a set of explicit rules that a machine can follow without hesitation, boredom, fear, or impulse. If your edge is real, automation can help you apply it consistently. If your edge is weak, automation will expose that faster too.

Introduction Why Traders Turn to Algorithms

Most traders don't fail because they can't spot patterns. They fail because they can't execute the same process the same way every time.

A manual trader says, “I buy pullbacks in an uptrend.” That sounds clear until the market opens and the pullback is deeper than expected, news is noisy, and three instruments are moving at once. Then the rule becomes fuzzy. Fuzzy rules create inconsistent trades.

An algorithm forces clarity. You have to define the setup, the entry, the stop, the exit, and the risk filter in a form a computer can understand. That pressure is useful. It removes a lot of the hidden ambiguity in how people trade.

The practical problem algorithms solve

Algorithmic trading helps with a few common pain points:

- Emotional execution: You don't panic out early or chase late because the system follows rules.

- Missed opportunities: The strategy can monitor markets continuously instead of relying on you to be at the screen.

- Inconsistent decision-making: The same signal gets the same treatment every time.

- Operational fatigue: You stop wasting energy re-evaluating the same setup from scratch.

Practical rule: If you can't explain your strategy in plain English first, you probably can't automate it well.

This isn't a niche corner of trading anymore. The global algorithmic trading market was valued at USD 21.06 billion in 2024 and is projected to reach USD 42.99 billion by 2030 according to Grand View Research's algorithmic trading market report. That matters because it tells you where modern trading infrastructure is headed. Automated execution, data handling, and systematic decision-making are now part of the standard toolkit.

For a newer trader, the important takeaway is simple. You don't need to think like a hedge fund to understand what is algorithmic trading. You need to think like a process designer. The core question isn't “How do I build a bot?” It's “What exact behavior do I want the system to repeat?”

The Core Concepts of Algorithmic Trading

The easiest way to understand what is algorithmic trading is to compare it to a recipe.

Your strategy is the recipe. Market data are the ingredients. The algorithm is the chef that follows instructions exactly as written. If your instructions say “buy when price closes above yesterday's high and volume rises,” the chef doesn't improvise. It follows the recipe.

That sounds simple, but most confusion starts here. People hear “algorithmic trading” and think only about speed, high-frequency trading, and firms fighting over microseconds. That's only part of the picture.

It's broader than “fast trading”

Algorithmic trading is the use of computer code to execute orders automatically when predefined market conditions are met, and it's widely used by institutions to spread large orders or execute trades more efficiently than humans. High-frequency trading is only one subset of the broader category, as described in Wikipedia's overview of algorithmic trading.

That distinction matters.

A retail trader might use an algorithm to trade a breakout system on a five-minute chart. A bank might use an algorithm to break up a large order so it doesn't slam into the market all at once. Both are algorithmic trading. One is trying to capture a directional move. The other is focused on execution quality.

The three pillars

Most working algo systems rest on three simple pillars:

- Defined rules: The system needs precise instructions. “Buy strong setups” is useless to a machine. “Buy when price closes above a moving average and the prior candle low holds” is at least testable.

- Reliable inputs: If your data are bad, your signals are bad. Price, volume, and session timing all need to be handled cleanly.

- Automated action: Once the rules trigger, the system must place, manage, and close orders without confusion.

Here's a plain-language example:

- You trade EUR/USD.

- Your rule says buy when short-term trend aligns with long-term trend.

- The algorithm checks that condition every bar.

- If the setup appears, it places the order.

- If the stop or target is hit, it exits automatically.

That's it. No gut feel. No “maybe I'll wait one more candle.”

Why it became dominant

Algorithmic trading became a mainstream market force in the late 1990s and 2000s as electronic exchanges expanded. One milestone often cited is 1998, when the U.S. SEC authorized electronic exchanges, helping computerized high-frequency trading move into the mainstream. By the end of 2009, algorithmic trading was estimated to account for about 70% of U.S. securities-market activity, and by 2013 analysts put roughly 70% of U.S. equity trading through algorithms according to Quantified Strategies' history of algorithmic trading.

That growth didn't happen because everyone suddenly found easy profits. It happened because markets reward systems that can process information, route orders efficiently, and apply rules without delay.

Algorithmic trading can reduce emotional mistakes. It doesn't remove market risk, strategy risk, or execution risk.

Common Algorithmic Trading Strategies Explained

A lot of beginners get stuck on strategy names. They sound technical, but the core logic is usually simple. The key question is not whether a strategy sounds smart. It's whether you can define it clearly enough to test it.

Trend following

Trend-following systems try to catch sustained directional moves. The logic is straightforward. If a market is moving up, the strategy looks for reasons to stay with the move rather than fade it.

A simple version might buy when price trades above a moving average and exit when it drops back below. It won't catch every turn, and it often gives back part of a move on exit, but that's the trade-off. You're paying for the chance to ride larger trends.

This style often suits traders who want clean rules and can tolerate periods of frustration when markets chop sideways.

Mean reversion

Mean reversion assumes a market that has stretched too far may snap back toward its average. The algorithm looks for overextension, then trades against it.

Example. If an instrument drops sharply away from its recent average, a mean reversion system may buy, expecting the move to relax. These systems can look brilliant in stable conditions and ugly in persistent trends. That's why market regime matters so much.

Momentum

Momentum overlaps with trend following, but the emphasis is different. Momentum strategies look for acceleration. They want assets already moving strongly and try to join that move while it still has force.

A breakout system is a common momentum approach. If price pushes through a recent high with strong participation, the algorithm enters and manages the trade with predefined exits.

If you want a broader library of setups to study, Rize Trade trading strategies is a useful reference for seeing how different trading styles are framed in practice.

Statistical arbitrage

This category sounds intimidating, but the base idea is simple. The system looks for relationships between instruments and tries to profit when those relationships temporarily drift.

That could involve paired instruments that usually move in a related way. When the spread between them gets unusual, the algorithm may bet on re-alignment. This usually requires stronger data handling and more careful testing than beginner strategies.

For retail traders exploring systematic ideas, it helps to review practical examples of algorithmic trading strategy types.

Comparison of Common Algorithmic Trading Strategies

| Strategy Type | Core Logic | Typical Timeframe | Complexity |

|---|---|---|---|

| Trend Following | Trade in the direction of an established move | Intraday to swing | Low to medium |

| Mean Reversion | Trade the return toward an average after extension | Intraday to short swing | Medium |

| Momentum | Buy strength or sell weakness as price accelerates | Short-term to intraday | Medium |

| Statistical Arbitrage | Trade temporary dislocations between related instruments | Usually short-term | High |

How to choose one

Don't pick a strategy because it sounds advanced. Pick one based on what you can support.

Ask yourself:

- What market behavior do I understand best? Trends, reversals, breakouts, or relative pricing?

- What data do I have access to? Basic chart data is enough for many simple systems.

- How much complexity can I manage? More moving parts means more ways to break.

- Can I explain the edge in one paragraph? If not, it's probably too vague.

A simple strategy with clear rules usually teaches you more than a sophisticated strategy you barely understand.

The Technical Infrastructure You Need

Most algo traders don't need institutional hardware. They do need a setup that's stable, testable, and appropriate for their strategy.

That's an important distinction. A daily trend system doesn't need the same infrastructure as a latency-sensitive execution model. Beginners often overspend on technology before they've proven they have a working idea.

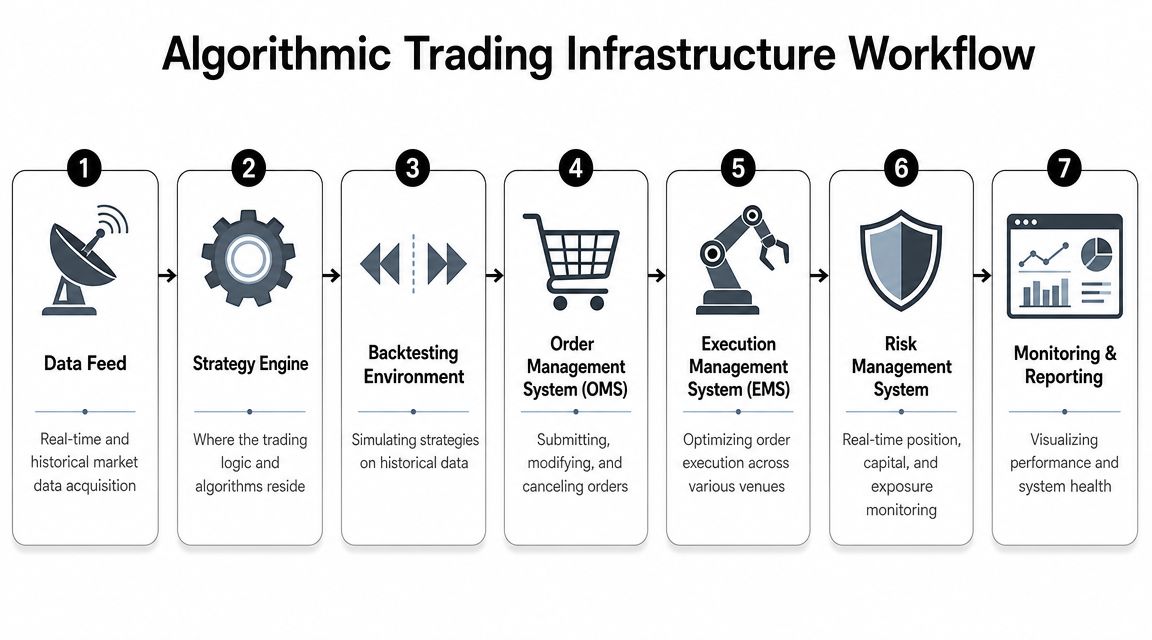

The core pieces

A practical algorithmic trading setup usually includes these parts:

- Market data feed: This provides the prices and other market information your strategy reads.

- Strategy engine: It contains your rules. It decides whether a signal exists.

- Backtesting environment: This lets you run the strategy on historical data before going live.

- Order routing and execution: The system needs a way to place, modify, and cancel orders through your platform or broker connection.

- Risk controls: Position limits, stop logic, daily loss limits, and exposure filters belong here.

- Monitoring: You need a way to catch failures, disconnected sessions, or odd trading behavior.

API, platform, and execution

If you hear people talk about API access, they're talking about a bridge between your code and the trading platform. The strategy generates a decision. The API communicates that decision to the execution layer.

In retail trading, the platform matters because it determines what you can automate, how you test, and how reliably orders are handled. Some traders use coding environments directly. Others use built-in automation tools on platforms designed for systematic trading.

What latency actually means

Latency is just delay. It's the time between a market event and your system's response.

For some strategies, latency matters a lot. For many others, it barely matters at all. If your strategy trades on higher timeframes and enters once every few hours or once per day, shaving tiny fractions of a second off execution probably won't change the outcome. If your system depends on very short-lived price changes, that's a different story.

Why reliability matters more than speed for most traders

Most newer algo traders should focus on uptime, not bragging rights.

A stable VPS can help because it keeps the system running even when your laptop sleeps, your internet drops, or your power flickers. That's not glamorous, but it's practical. If you want a non-trading example of how expensive downtime can become in financial systems, Fivenines analysis of fintech costs gives useful context on why reliability gets so much attention.

Here's the checklist I'd give a new team member:

- Start with your strategy needs: Match infrastructure to timeframe and execution style.

- Keep the first version simple: You can improve architecture after the strategy proves itself.

- Build monitoring early: A system you can't observe is a system you can't trust.

- Assume failure will happen: Internet issues, stale data, and software bugs are normal engineering problems.

How to Build and Backtest Your Trading Algorithm

The majority of the critical work is performed. Not in the idea. In the translation.

A trading idea in your head is vague by default. A trading algorithm has to be explicit. Every condition, every exception, every exit rule needs to be written down and tested.

Step 1 Define the rules in plain English

Before you code anything, write the strategy like instructions for another person.

Bad rule:

- Buy when the market looks strong.

Better rule:

- Buy when price closes above the prior session high and the current trend filter is bullish.

- Risk a fixed amount per trade.

- Exit at a predefined stop, target, or opposite signal.

If you can't make the rule specific, stop there. Coding fuzzy logic only creates polished confusion.

Step 2 Translate the idea into a system

This is the development stage. Many traders use Python for research and prototyping. Others use platform-native tools such as cTrader Automate or other scripting environments tied to execution platforms.

You don't need to become a full-time software engineer. You do need enough structure to answer questions like:

- What exactly counts as a valid signal?

- When does the system ignore a setup?

- How much can it risk on one trade?

- What happens if two signals appear at once?

Some traders use assistants and workflow tools during ideation. If you're researching tools that can support strategy design or automation workflows, the Tradeos AI tool is one example worth reviewing.

Step 3 Backtest on historical data

An essential workflow in algorithmic trading is strategy development followed by backtesting on historical data. Performance should be evaluated with metrics such as total return, maximum drawdown, and Sharpe ratio, because those measures help reveal whether the strategy's edge survives costs and market changes, as explained in TrendSpider's guide to algorithmic trading basics.

That sentence contains the heart of the process.

A backtest is not there to flatter you. It's there to challenge the idea.

Look for questions like these:

- Did the strategy make money in one short stretch only?

- How ugly were the losing periods?

- Was drawdown tolerable relative to the return?

- Did performance depend on a very narrow parameter choice?

If changing one setting slightly destroys the results, that's a warning sign.

Step 4 Forward test before treating it as real

After backtesting, run the algorithm in a demo or simulated environment. That's often called forward testing. The goal is to see how the system behaves with live incoming data, real spreads, timing friction, and operational quirks.

This stage catches problems that backtests miss:

- Execution mismatches: Orders fill differently than expected.

- Coding bugs: A condition triggers repeatedly when it shouldn't.

- Session issues: The strategy behaves differently around rollover or market open.

- Risk leaks: Position sizing or stop handling doesn't behave as planned.

For traders who are still learning this phase, this backtesting guide gives a useful overview of how historical testing fits into the broader validation process.

Backtests tell you whether an idea deserved a closer look. They do not prove the future.

A simple build checklist

- Write the setup clearly

- Code the exact rules

- Backtest on clean historical data

- Review return, drawdown, and risk-adjusted behavior

- Forward test in a safe environment

- Change one variable at a time

- Document every version

That last one matters more than people think. If you can't track what changed between versions, you won't know whether improvement came from the strategy or from accidental curve-fitting.

Using Algorithmic Trading with MyFundedCapital

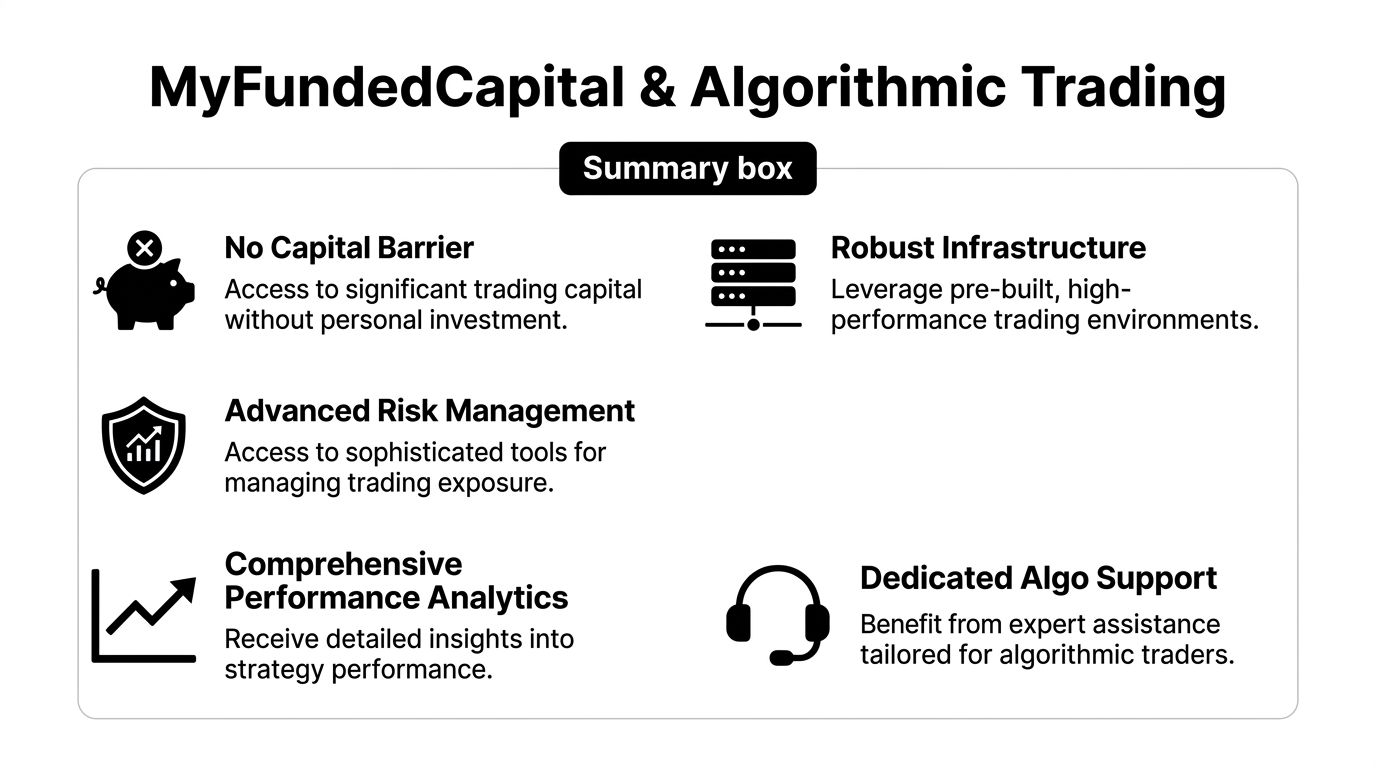

For many retail traders, the biggest bottleneck isn't ideas. It's capital, platform access, and a clear operating framework.

That's where a prop-style environment can become useful. Instead of trying to scale a small personal account while also debugging a strategy, some traders prefer to prove their process inside a funded program built around risk rules and platform structure.

Why that matters for system traders

Algorithmic traders usually care about a few things more than marketing language:

- Platform compatibility: If you build automated systems, you need platforms that support that workflow.

- Clear risk rules: The algorithm has to know its boundaries.

- Enough room to test discipline: You need a framework that rewards consistency, not random oversized bets.

MyFundedCapital supports manual, algorithmic, and copy trading across 350+ instruments on DXtrade and cTrader, with MT5 coming soon, according to the firm's published overview on its website. For an algo trader, that matters because platform support shapes how easily you can deploy and monitor a rule-based system.

Risk rules are part of the design brief

A lot of traders treat prop firm rules like an obstacle. A better way to think about them is as engineering constraints.

MyFundedCapital publishes a flat 5% daily loss limit and up to 10% maximum drawdown in its program overview. Those limits are useful because they force discipline into the system design. If your strategy can't operate cleanly inside explicit loss boundaries, that's not a prop-firm problem. That's a strategy design problem.

This is one reason systematic traders often prefer transparent constraints. They can code them in. They can test around them. They can see quickly whether the strategy's risk profile fits the environment.

If you're specifically exploring firm support for automation, MyFundedCapital automated trading programs outlines how the company approaches algorithmic and system-based participation.

Where it fits in the workflow

A funded environment makes the most sense after you've already done the hard part:

- You've defined the strategy

- You've tested it historically

- You've forward-tested execution

- You understand the drawdown behavior

- You know the system's operational requirements

At that point, the question becomes practical. Where do you want to run a proven process? For a trader who doesn't want to commit large personal capital upfront, a prop structure can be a reasonable next step.

Trading still involves risk of loss. Funding doesn't change that. It just changes the capital framework around the same core requirement, which is disciplined execution.

Frequently Asked Questions About Algorithmic Trading

Do I need to know how to code?

Not always, but some coding knowledge helps a lot. If you build your own system, coding gives you control and transparency. If you use a pre-built bot or EA, you can get started faster, but you also inherit someone else's logic, assumptions, and possible flaws.

For most serious traders, the better long-term path is understanding enough code or platform logic to inspect how the system behaves.

Is algorithmic trading legal for retail traders?

In many markets, retail traders can legally use automated trading tools through supported brokers and platforms. The details depend on where you live, what market you trade, and what platform rules apply. The key point is simple. Legal access doesn't remove the need for responsible risk management, good testing, and compliance with platform terms.

What are the biggest risks besides losing trades?

The main risks aren't only market-related.

- Coding errors: A small logic bug can produce completely different trades than intended.

- Overfitting: The strategy looks great on historical data because it was tuned too closely to the past.

- Execution issues: Slippage, rejected orders, or data problems can change outcomes.

- Technology failure: Your script, VPS, or platform can fail at the worst time.

Should I buy a ready-made bot or build my own?

If you buy one, treat it like buying a black-box business. You need to know what it does, when it struggles, and how risk is managed. If the seller can't explain the logic clearly, that's a bad sign.

Building your own usually takes longer, but it teaches you the one skill that matters most in algorithmic trading. Knowing why the system is taking each trade.

If you're ready to move from theory to execution, explore MyFundedCapital to compare funding programs, review account types, and see whether its platform and risk framework fit your algorithmic trading process. Trading involves risk of loss, and this article is educational only, not financial advice.